Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please help me with this question. Im struggling a lot with financial. Table 1 Cash Flow in One Year Security Market Price Today Weak Economy

Please help me with this question. Im struggling a lot with financial.

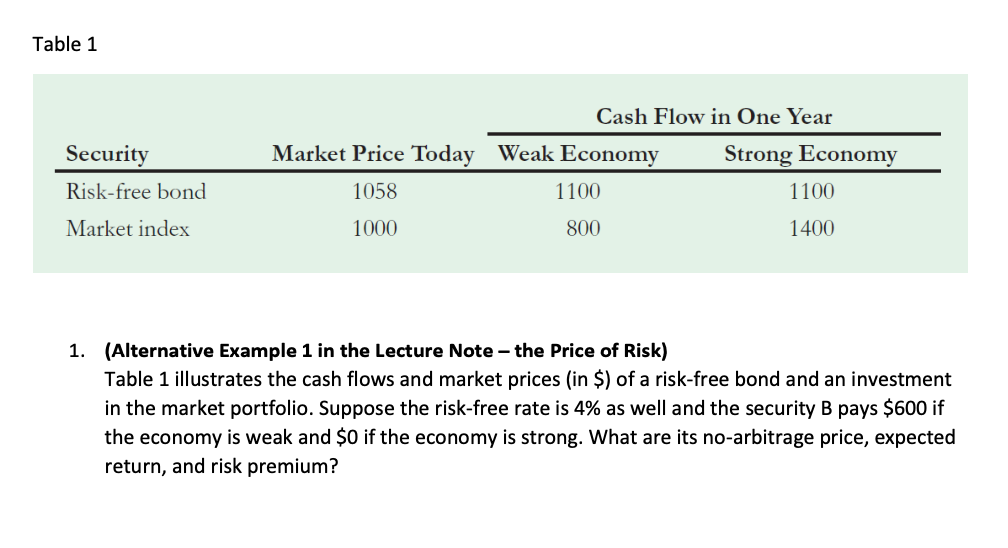

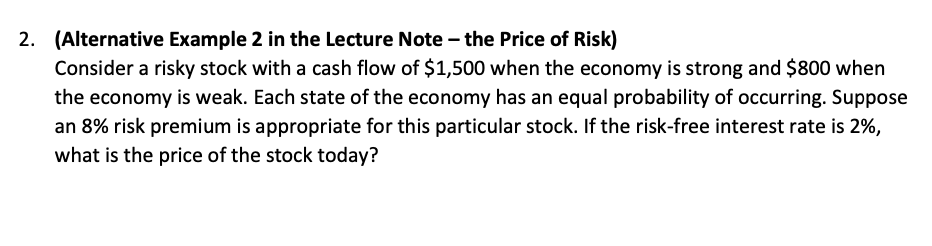

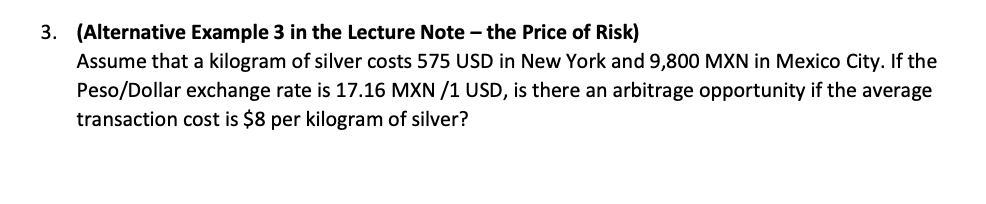

Table 1 Cash Flow in One Year Security Market Price Today Weak Economy Strong Economy Risk-free bond 1058 1100 1100 Market index 1000 800 1400 1. (Alternative Example 1 in the Lecture Note - the Price of Risk) Table 1 illustrates the cash flows and market prices (in $) of a risk-free bond and an investment in the market portfolio. Suppose the risk-free rate is 4% as well and the security B pays $600 if the economy is weak and $0 if the economy is strong. What are its no-arbitrage price, expected return, and risk premium? 2. (Alternative Example 2 in the Lecture Note - the Price of Risk) Consider a risky stock with a cash flow of $1,500 when the economy is strong and $800 when the economy is weak. Each state of the economy has an equal probability of occurring. Suppose an 8% risk premium is appropriate for this particular stock. If the risk-free interest rate is 2%, what is the price of the stock today? 3. (Alternative Example 3 in the Lecture Note - the Price of Risk) Assume that a kilogram of silver costs 575 USD in New York and 9,800 MXN in Mexico City. If the Peso/Dollar exchange rate is 17.16 MXN /1 USD, is there an arbitrage opportunity if the average transaction cost is $8 per kilogram of silver? Table 1 Cash Flow in One Year Security Market Price Today Weak Economy Strong Economy Risk-free bond 1058 1100 1100 Market index 1000 800 1400 1. (Alternative Example 1 in the Lecture Note - the Price of Risk) Table 1 illustrates the cash flows and market prices (in $) of a risk-free bond and an investment in the market portfolio. Suppose the risk-free rate is 4% as well and the security B pays $600 if the economy is weak and $0 if the economy is strong. What are its no-arbitrage price, expected return, and risk premium? 2. (Alternative Example 2 in the Lecture Note - the Price of Risk) Consider a risky stock with a cash flow of $1,500 when the economy is strong and $800 when the economy is weak. Each state of the economy has an equal probability of occurring. Suppose an 8% risk premium is appropriate for this particular stock. If the risk-free interest rate is 2%, what is the price of the stock today? 3. (Alternative Example 3 in the Lecture Note - the Price of Risk) Assume that a kilogram of silver costs 575 USD in New York and 9,800 MXN in Mexico City. If the Peso/Dollar exchange rate is 17.16 MXN /1 USD, is there an arbitrage opportunity if the average transaction cost is $8 per kilogram of silverStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

8th Edition

0132164949, 9780132164948