Please help parts A - E

Please help parts A - E

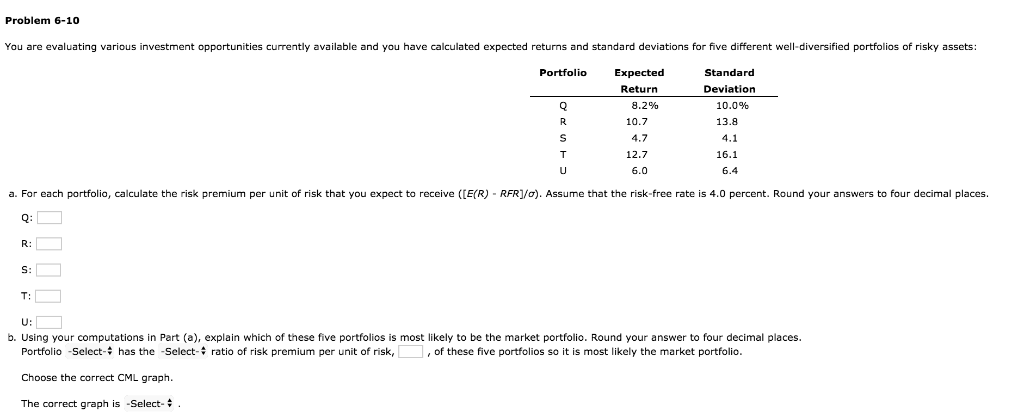

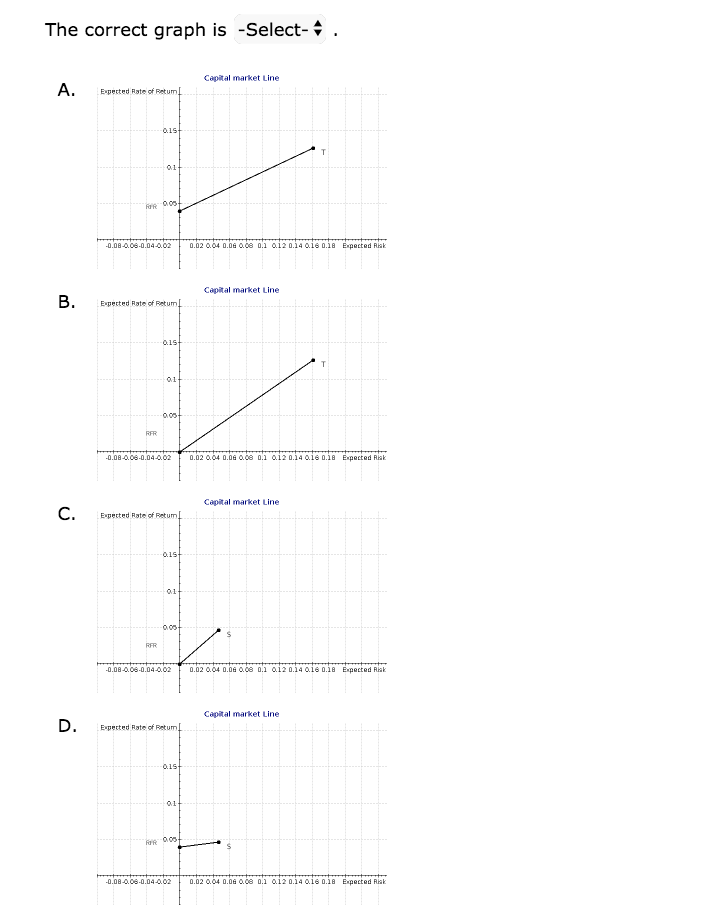

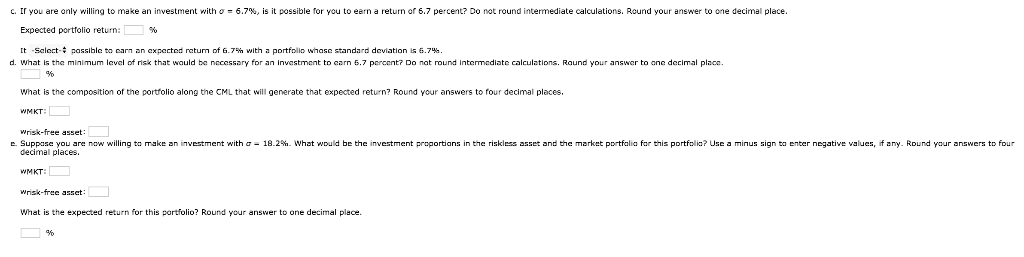

Problem 6-10 You are evaluating various investment opportunities currently available and you have calculated expected returns and standard deviations for five different well-diversified portfolios of risky assets Portfolio Expected Return Standard Deviation 10.0% 13.8 8.2% 10.7 4.7 12.7 6.0 16.1 a. For each portfolio, calculate the risk premium per unit of risk that you expect to receive ([E(R)-RFR)/o). Assume that the risk-free rate is 4.0 percent. Round your answers to four decimal places. T: U: b. Using your computations in Part (a), explain which of these five portfolios is most likely to be the market portfolio. Round your answer to four decimal places , of these five portfolios so it is most likely the market portfolio Portfolio -Select-4 has the -Select- Choose the correct CML graph The correct graph is -Select- ratio of risk premium per unit of risk, The correct graph is -Select-4 Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum FR 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 0. 12 0.14 01 0.18 Expected Rak c. tr you are only willing to make an investment with o-6.7%, is it possible for you to earn a return or 6.7 percent? Do not round intermediate calculations. Round your answer to one decimal place. Expected portfolio return: It -Select-, passible to earn an expected rtum of 6.7%, with a portfolis whase standard deviation is 6.7%. d. What is the minimum lavel of risk that wauld ba necossary for an investment to earn 6.7 percent? Do nat round intermediate calculations. Raund your answer to ane decimal placo. answers What is the composition of the portfolio along the CML that will generate that expected return? Round your answers to four decimal places, WMKT Wrisk-free asset decimal places WMKT Wrisk-free asset What is the expected return for this portfolio? Round your answer to one decimal place. e. Suppase you are now willing to make an investment with 18.2% what would be the investment proportans in tne riskless asset and the market portfalia ar this Portfoia? Use a minus sign to enter negative values if any. Round your answers to our Problem 6-10 You are evaluating various investment opportunities currently available and you have calculated expected returns and standard deviations for five different well-diversified portfolios of risky assets Portfolio Expected Return Standard Deviation 10.0% 13.8 8.2% 10.7 4.7 12.7 6.0 16.1 a. For each portfolio, calculate the risk premium per unit of risk that you expect to receive ([E(R)-RFR)/o). Assume that the risk-free rate is 4.0 percent. Round your answers to four decimal places. T: U: b. Using your computations in Part (a), explain which of these five portfolios is most likely to be the market portfolio. Round your answer to four decimal places , of these five portfolios so it is most likely the market portfolio Portfolio -Select-4 has the -Select- Choose the correct CML graph The correct graph is -Select- ratio of risk premium per unit of risk, The correct graph is -Select-4 Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum FR 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 8 0. 12 0.14 01 0.18 Expected Rak Capital market Line Expected Rate of Retum 0.08-008-0.04-0020.02 004 0.0 0. 12 0.14 01 0.18 Expected Rak c. tr you are only willing to make an investment with o-6.7%, is it possible for you to earn a return or 6.7 percent? Do not round intermediate calculations. Round your answer to one decimal place. Expected portfolio return: It -Select-, passible to earn an expected rtum of 6.7%, with a portfolis whase standard deviation is 6.7%. d. What is the minimum lavel of risk that wauld ba necossary for an investment to earn 6.7 percent? Do nat round intermediate calculations. Raund your answer to ane decimal placo. answers What is the composition of the portfolio along the CML that will generate that expected return? Round your answers to four decimal places, WMKT Wrisk-free asset decimal places WMKT Wrisk-free asset What is the expected return for this portfolio? Round your answer to one decimal place. e. Suppase you are now willing to make an investment with 18.2% what would be the investment proportans in tne riskless asset and the market portfalia ar this Portfoia? Use a minus sign to enter negative values if any. Round your answers to our