Answered step by step

Verified Expert Solution

Question

1 Approved Answer

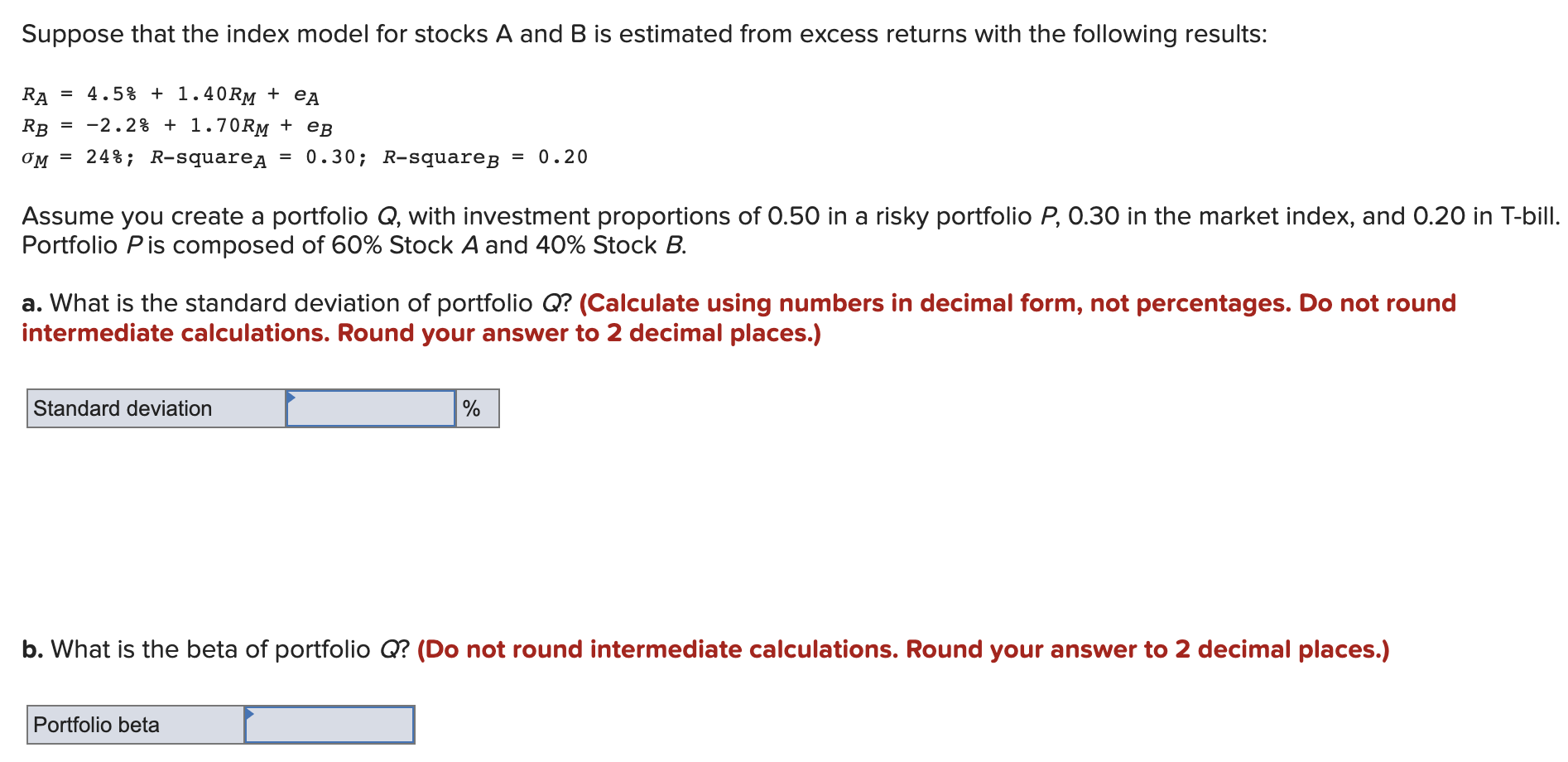

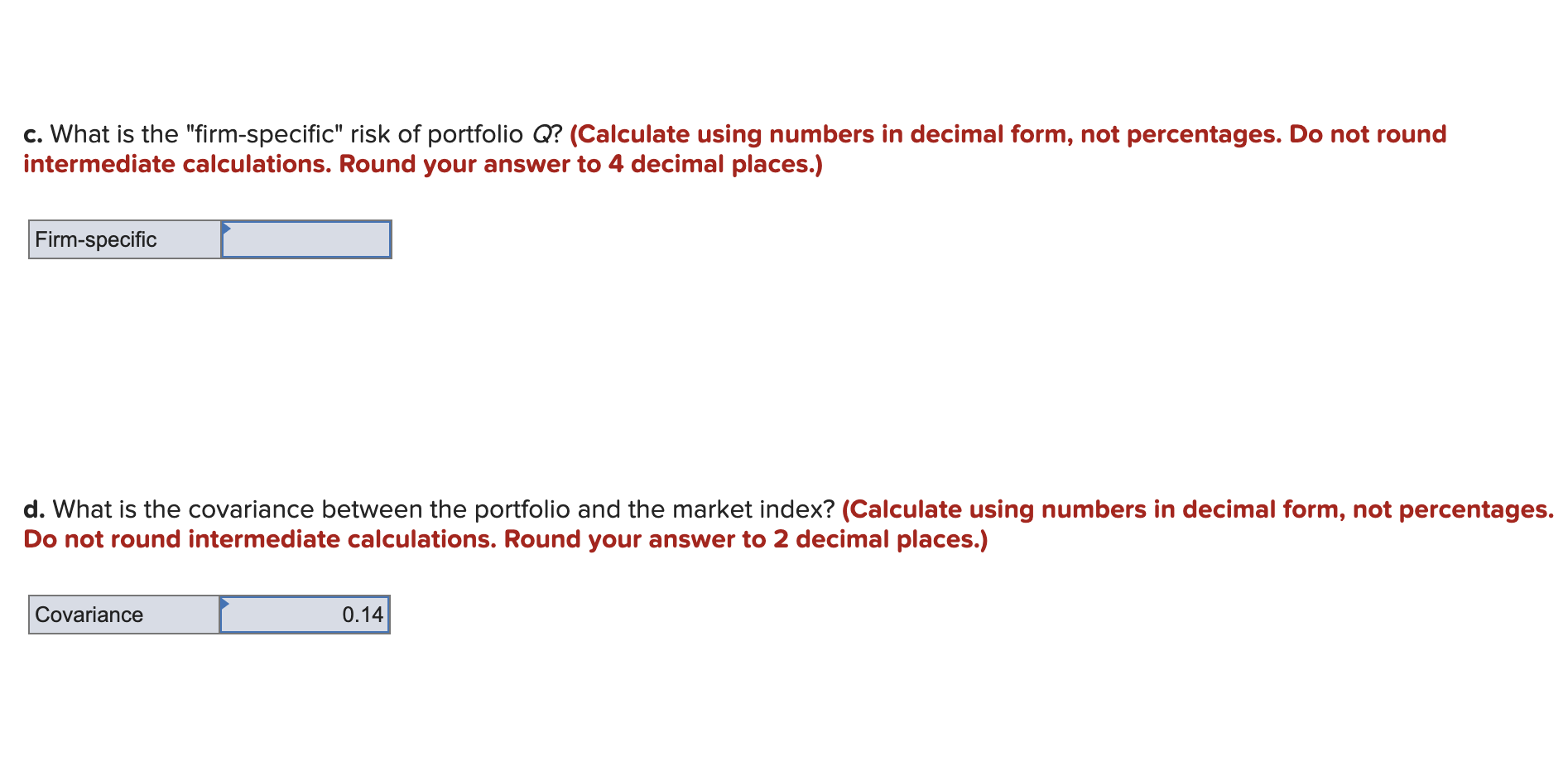

please help RA=4.5%+1.40RM+eARB=2.2%+1.70RM+eBM=24%;RsquareA=0.30;R-squareB=0.20 Assume you create a portfolio Q, with investment proportions of 0.50 in a risky portfolio P,0.30 in the market index, and 0.20

please help

please help

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Family Inc Using Business Principles To Maximize Your Familys Wealth

Authors: Douglas P. McCormick

1st Edition

1119577411, 978-1119577416