Answered step by step

Verified Expert Solution

Question

1 Approved Answer

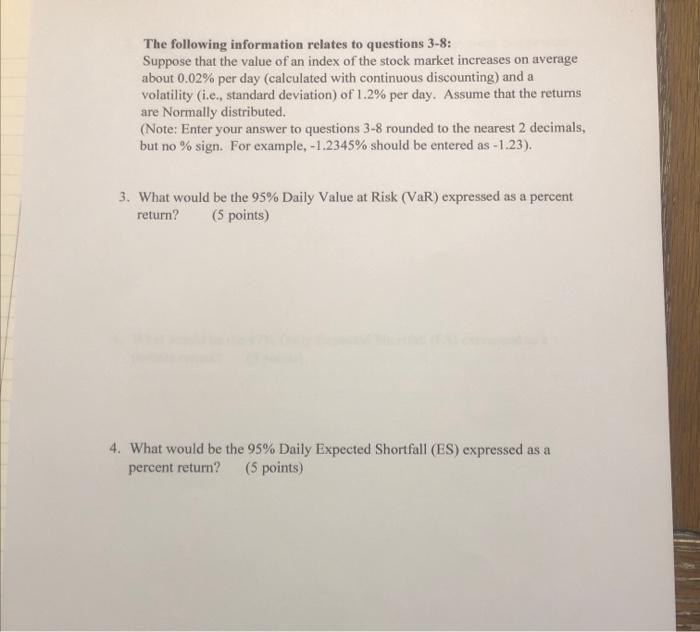

please help! risk management! show work please! The following information relates to questions 3-8: Suppose that the value of an index of the stock market

please help! risk management!

The following information relates to questions 3-8: Suppose that the value of an index of the stock market increases on average about 0.02% per day (calculated with continuous discounting) and a volatility (i.c., standard deviation) of 1.2% per day. Assume that the returns are Normally distributed. (Note: Enter your answer to questions 3-8 rounded to the nearest 2 decimals, but no % sign. For example, -1.2345% should be entered as -1.23). 3. What would be the 95% Daily Value at Risk (VaR) expressed as a percent return? (5 points) 4. What would be the 95% Daily Expected Shortfall (ES) expressed as a percent return? (5 points) show work please!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Family Inc Using Business Principles To Maximize Your Familys Wealth

Authors: Douglas P. McCormick

1st Edition

1119577411, 978-1119577416