Answered step by step

Verified Expert Solution

Question

1 Approved Answer

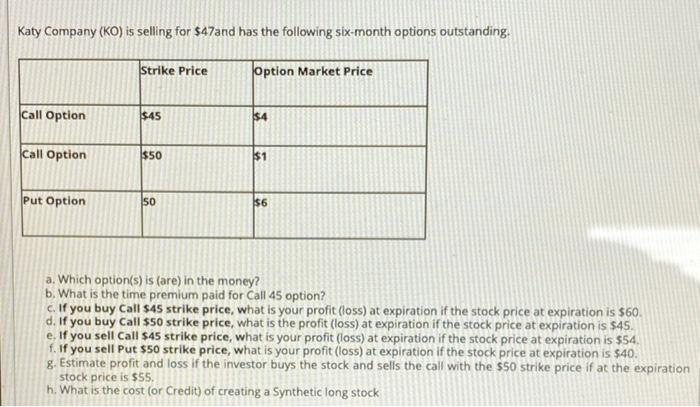

Please help! Thank you! Katy Company (KO) is selling for $47and has the following six-month options outstanding Strike Price Option Market Price Call Option $45

Please help! Thank you!

Katy Company (KO) is selling for $47and has the following six-month options outstanding Strike Price Option Market Price Call Option $45 Call Option $50 Put Option 50 $6 a. Which option(s) is (are) in the money? b. What is the time premium paid for Call 45 option? c. If you buy Call 845 strike price, what is your profit (loss) at expiration if the stock price at expiration is 560 d. If you buy Call 50 strike price, what is the profit (loss) at expiration if the stock price at expiration is $45. e. If you sell Call $45 strike price, what is your profit (loss) at expiration if the stock price at expiration is $54 f. If you sell Put $50 strike price, what is your profit (loss) at expiration if the stock price at expiration is $40. g. Estimate profit and loss if the investor buys the stock and sells the call with the $50 strike price if at the expiration stock price is $55. h. What is the cost (or Credit) of creating a Synthetic long stock Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Housing An Introduction

Authors: Cathy Davis

1st Edition

1447306481, 978-1447306481