Answered step by step

Verified Expert Solution

Question

1 Approved Answer

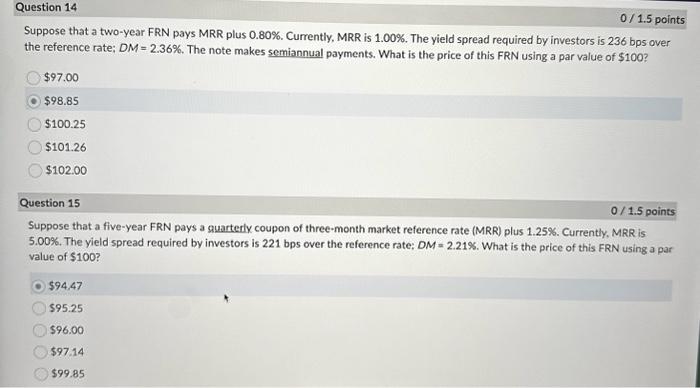

please help! thank you! the current answers are wrong. Suppose that a two-year FRN pays MRR plus 0.80%. Currently, MRR is 1.00%. The yield spread

please help! thank you! the current answers are wrong.

Suppose that a two-year FRN pays MRR plus 0.80%. Currently, MRR is 1.00%. The yield spread required by investors is 236 bps over the reference rate; DM=2.36%. The note makes semiannual payments. What is the price of this FRN using a par value of $100 ? $97.00 $98.85 $100.25 $101.26 $102.00 Question 15 0/1.5 points Suppose that a five-year FRN pays a quarterly coupon of three-month market reference rate (MRR) plus 1.25\%. Currently, MRR is 5.00%. The yield spread required by investors is 221 bps over the reference rate; DM=2.21%. What is the price of this FRN using a par value of $100 ? $94,47 $95.25 $96.00 $97.14 $99.85 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New Retirementality Planning Your Life And Living Your Dreams At Any Age You Want

Authors: Mitch Anthony

4th Edition

1118705122, 978-1118705124