Answered step by step

Verified Expert Solution

Question

1 Approved Answer

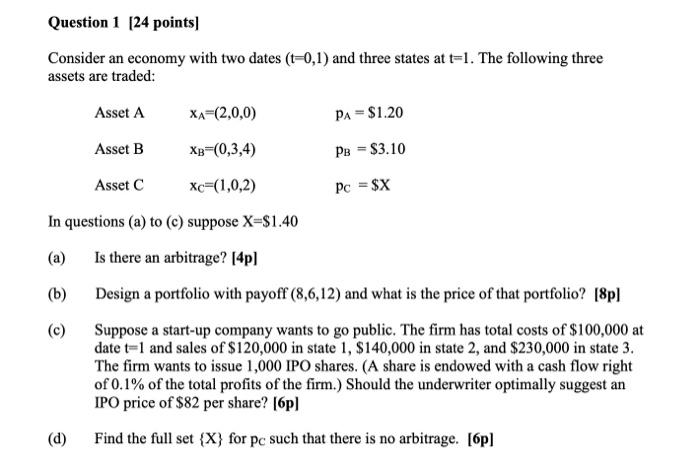

Please help with all the parts. Thanks! Question 1 (24 points) Consider an economy with two dates (t=0,1) and three states at t=1. The following

Please help with all the parts. Thanks!

Question 1 (24 points) Consider an economy with two dates (t=0,1) and three states at t=1. The following three assets are traded: Asset A XA (2,0,0) PA = $1.20 Asset B XB-(0,3,4) PB = $3.10 Asset C Xc=(1,0,2) Pc = $x In questions (a) to (c) suppose X=$1.40 (a) Is there an arbitrage? [4p) (6) Design a portfolio with payoff (8,6,12) and what is the price of that portfolio? [8pl (c) Suppose a start-up company wants to go public. The firm has total costs of $100,000 at date t-1 and sales of $120,000 in state 1, $140,000 in state 2, and $230,000 in state 3. The firm wants to issue 1,000 IPO shares. (A share is endowed with a cash flow right of 0.1% of the total profits of the firm.) Should the underwriter optimally suggest an IPO price of $82 per share? (6p) (d) Find the full set {X} for pc such that there is no arbitrage. [6] Question 1 (24 points) Consider an economy with two dates (t=0,1) and three states at t=1. The following three assets are traded: Asset A XA (2,0,0) PA = $1.20 Asset B XB-(0,3,4) PB = $3.10 Asset C Xc=(1,0,2) Pc = $x In questions (a) to (c) suppose X=$1.40 (a) Is there an arbitrage? [4p) (6) Design a portfolio with payoff (8,6,12) and what is the price of that portfolio? [8pl (c) Suppose a start-up company wants to go public. The firm has total costs of $100,000 at date t-1 and sales of $120,000 in state 1, $140,000 in state 2, and $230,000 in state 3. The firm wants to issue 1,000 IPO shares. (A share is endowed with a cash flow right of 0.1% of the total profits of the firm.) Should the underwriter optimally suggest an IPO price of $82 per share? (6p) (d) Find the full set {X} for pc such that there is no arbitrage. [6] Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational financial management

Authors: Alan c. Shapiro

10th edition

9781118801161, 1118572386, 1118801164, 978-1118572382