Answered step by step

Verified Expert Solution

Question

1 Approved Answer

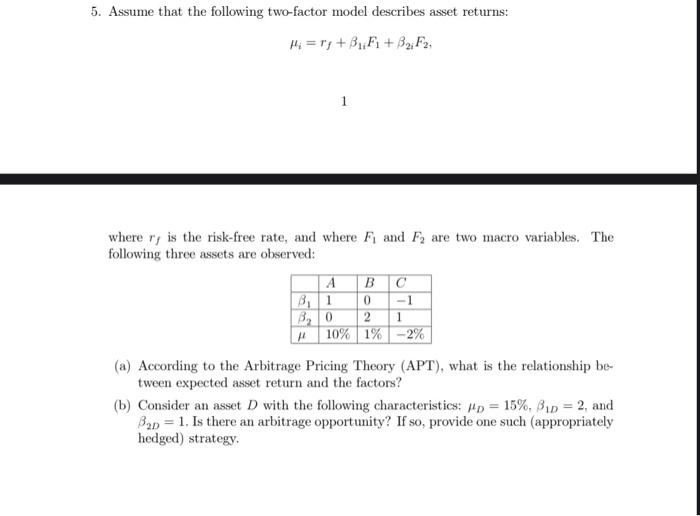

please help, with steps 5. Assume that the following two-factor model describes asset returns: i=rf+1iF1+2iF2, 1 where rf is the risk-free rate, and where F1

please help, with steps

5. Assume that the following two-factor model describes asset returns: i=rf+1iF1+2iF2, 1 where rf is the risk-free rate, and where F1 and F2 are two macro variables. The following three assets are observed: (a) According to the Arbitrage Pricing Theory (APT), what is the relationship between expected asset return and the factors? (b) Consider an asset D with the following characteristics: D=15%,1D=2, and 2D=1. Is there an arbitrage opportunity? If so, provide one such (appropriately hedged) strategy. 5. Assume that the following two-factor model describes asset returns: i=rf+1iF1+2iF2, 1 where rf is the risk-free rate, and where F1 and F2 are two macro variables. The following three assets are observed: (a) According to the Arbitrage Pricing Theory (APT), what is the relationship between expected asset return and the factors? (b) Consider an asset D with the following characteristics: D=15%,1D=2, and 2D=1. Is there an arbitrage opportunity? If so, provide one such (appropriately hedged) strategy Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of The Political Economy Of Financial Crises

Authors: Martin H. Wolfson, Gerald A. Epstein

1st Edition

0199757232, 978-0199757237