Answered step by step

Verified Expert Solution

Question

1 Approved Answer

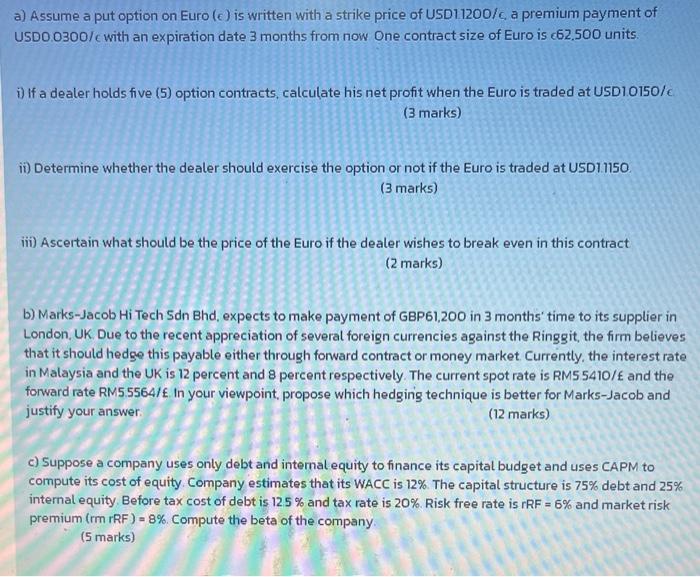

please helpppp a) Assume a put option on Euro (e) is written with a strike price of USD11200/c, a premium payment of USDO 0300/c with

please helpppp

a) Assume a put option on Euro (e) is written with a strike price of USD11200/c, a premium payment of USDO 0300/c with an expiration date 3 months from now One contract size of Euro is 62,500 units. i) If a dealer holds five (5) option contracts, calculate his net profit when the Euro is traded at USD10150/c (3 marks) ii) Determine whether the dealer should exercise the option or not if the Euro is traded at USD1.1150. (3 marks) iii) Ascertain what should be the price of the Euro if the dealer wishes to break even in this contract (2 marks) b) Marks-Jacob Hi Tech Sdn Bhd, expects to make payment of GBP61,200 in 3 months' time to its supplier in London, UK. Due to the recent appreciation of several foreign currencies against the Ringgit, the firm believes that it should hedge this payable either through forward contract or money market Currently, the interest rate in Malaysia and the UK is 12 percent and 8 percent respectively. The current spot rate is RM5.5410/ and the forward rate RM5.5564/. In your viewpoint, propose which hedging technique is better for Marks-Jacob and justify your answer. (12 marks) c) Suppose a company uses only debt and internal equity to finance its capital budget and uses CAPM to compute its cost of equity. Company estimates that its WACC is 12%. The capital structure is 75% debt and 25% internal equity Before tax cost of debt is 12.5 % and tax rate is 20%. Risk free rate is rRF = 6% and market risk premium (rm rRF) - 8%. Compute the beta of the company Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Option Trader Handbook

Authors: George Jabbour

2nd Edition

0470481617, 978-0470481615