Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please highlight/bold final answers. Please display all formulas. Please explain work. Thank you :) FINANCE PROBLEM Binomial Option Method Challenge Problem Show all work. All

Please highlight/bold final answers.

Please display all formulas.

Please explain work.

Thank you :)

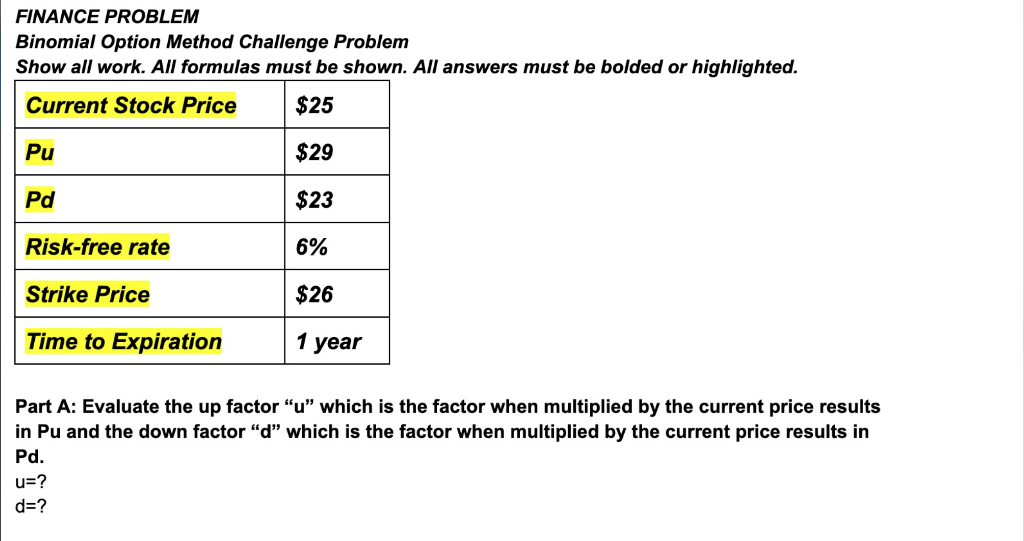

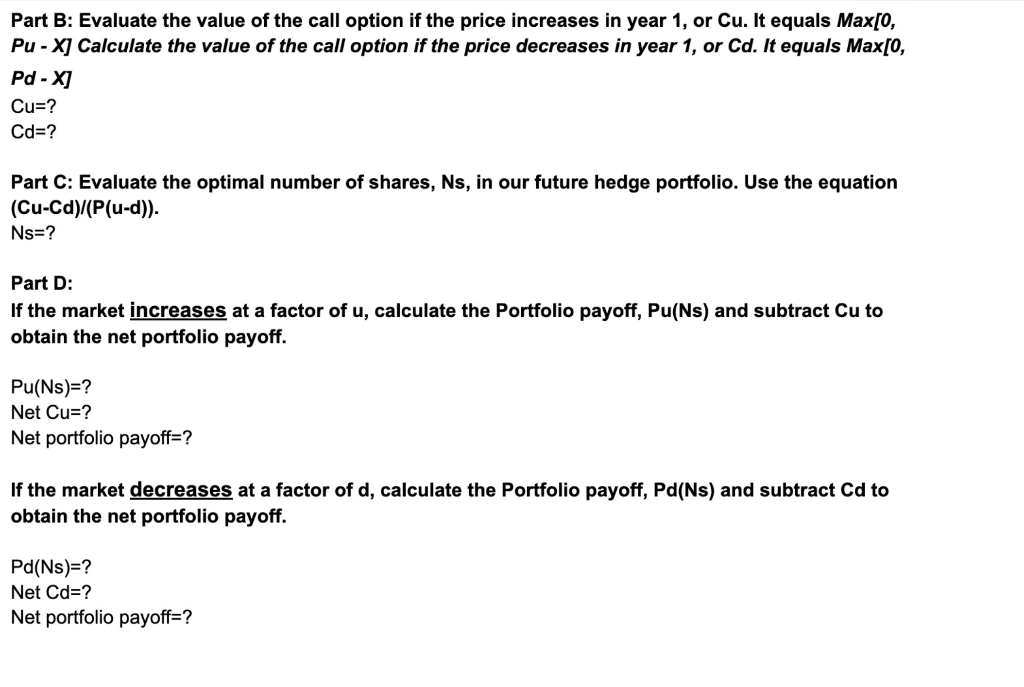

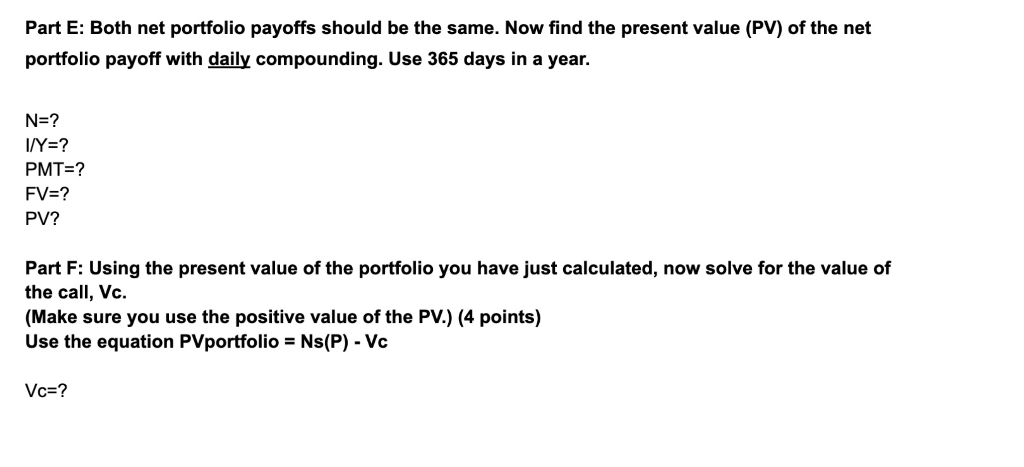

FINANCE PROBLEM Binomial Option Method Challenge Problem Show all work. All formulas must be shown. All answers must be bolded or highlighted. Current Stock Price $25 Pu $29 Pd $23 Risk-free rate 6% Strike Price $26 Time to Expiration 1 year Part A: Evaluate the up factor u which is the factor when multiplied by the current price results in Pu and the down factor d which is the factor when multiplied by the current price results in Pd. u=? d=? Part B: Evaluate the value of the call option if the price increases in year 1, or Cu. It equals Max[0, Pu - X] Calculate the value of the call option if the price decreases in year 1, or Cd. It equals Max[0, Pd - X] Cu=? Cd=? Part C: Evaluate the optimal number of shares, Ns, in our future hedge portfolio. Use the equation (Cu-Cd)/(P(u-d)) Ns=? Part D: If the market increases at a factor of u, calculate the Portfolio payoff, Pu(Ns) and subtract Cu to obtain the net portfolio payoff. Pu(Ns)? Net Cu=? Net portfolio payoff=? If the market decreases at a factor of d, calculate the Portfolio payoff, Pd(Ns) and subtract Cd to obtain the net portfolio payoff. Pd(NS)=? Net Cd=? Net portfolio payoff=? Part E: Both net portfolio payoffs should be the same. Now find the present value (PV) of the net portfolio payoff with daily compounding. Use 365 days in a year. N=? I/Y=? PMT=? FV=? PV? Part F: Using the present value of the portfolio you have just calculated, now solve for the value of the call, Vc. (Make sure you use the positive value of the PV.) (4 points) Use the equation PVportfolio = Ns(P) - Vc Vc=? FINANCE PROBLEM Binomial Option Method Challenge Problem Show all work. All formulas must be shown. All answers must be bolded or highlighted. Current Stock Price $25 Pu $29 Pd $23 Risk-free rate 6% Strike Price $26 Time to Expiration 1 year Part A: Evaluate the up factor u which is the factor when multiplied by the current price results in Pu and the down factor d which is the factor when multiplied by the current price results in Pd. u=? d=? Part B: Evaluate the value of the call option if the price increases in year 1, or Cu. It equals Max[0, Pu - X] Calculate the value of the call option if the price decreases in year 1, or Cd. It equals Max[0, Pd - X] Cu=? Cd=? Part C: Evaluate the optimal number of shares, Ns, in our future hedge portfolio. Use the equation (Cu-Cd)/(P(u-d)) Ns=? Part D: If the market increases at a factor of u, calculate the Portfolio payoff, Pu(Ns) and subtract Cu to obtain the net portfolio payoff. Pu(Ns)? Net Cu=? Net portfolio payoff=? If the market decreases at a factor of d, calculate the Portfolio payoff, Pd(Ns) and subtract Cd to obtain the net portfolio payoff. Pd(NS)=? Net Cd=? Net portfolio payoff=? Part E: Both net portfolio payoffs should be the same. Now find the present value (PV) of the net portfolio payoff with daily compounding. Use 365 days in a year. N=? I/Y=? PMT=? FV=? PV? Part F: Using the present value of the portfolio you have just calculated, now solve for the value of the call, Vc. (Make sure you use the positive value of the PV.) (4 points) Use the equation PVportfolio = Ns(P) - Vc Vc=Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Basic Finance An Introduction to Financial Institutions Investments and Management

Authors: Herbert B. Mayo

10th edition

1111820635, 978-1111820633