Please i need a solution urgently i am in exam

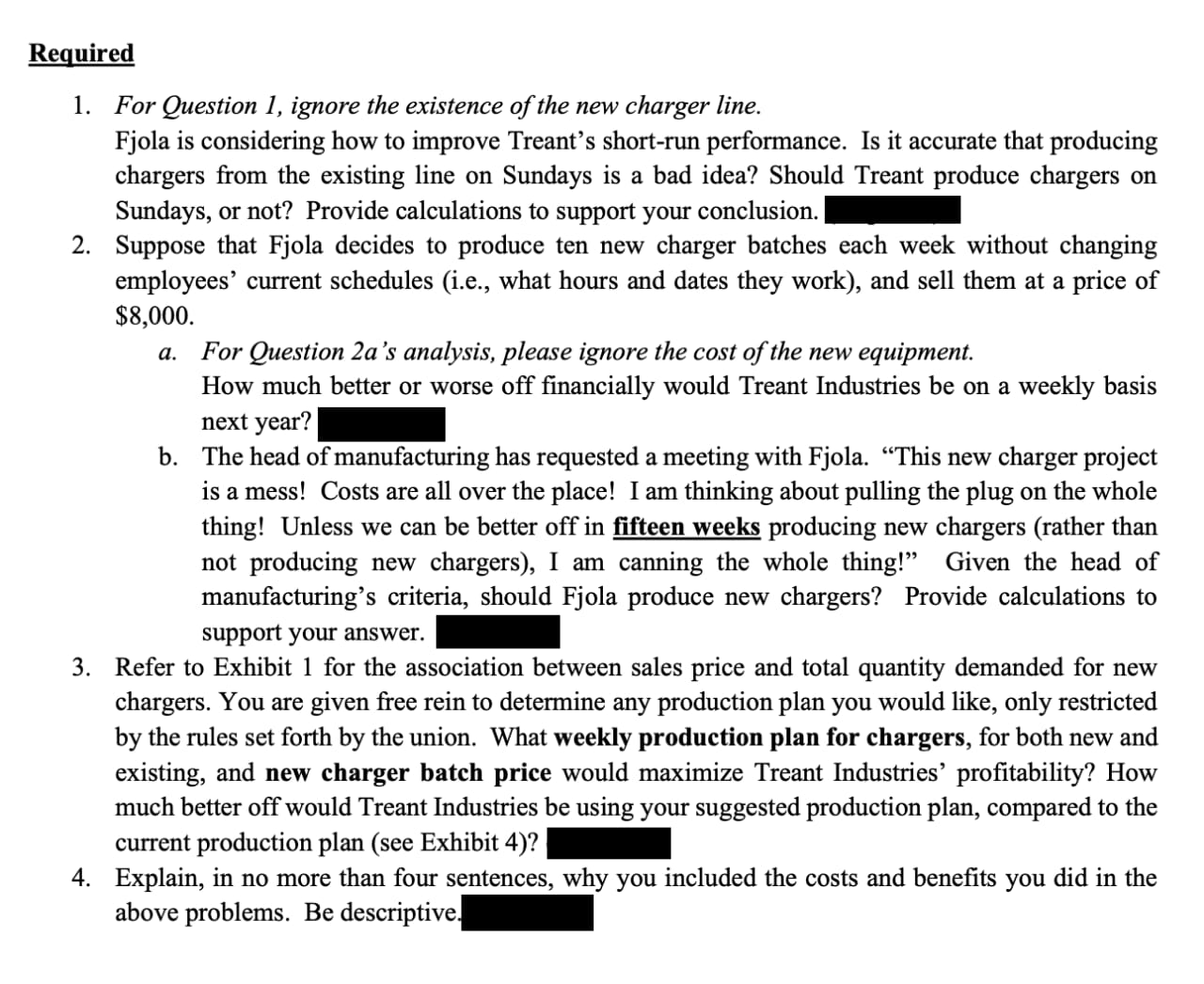

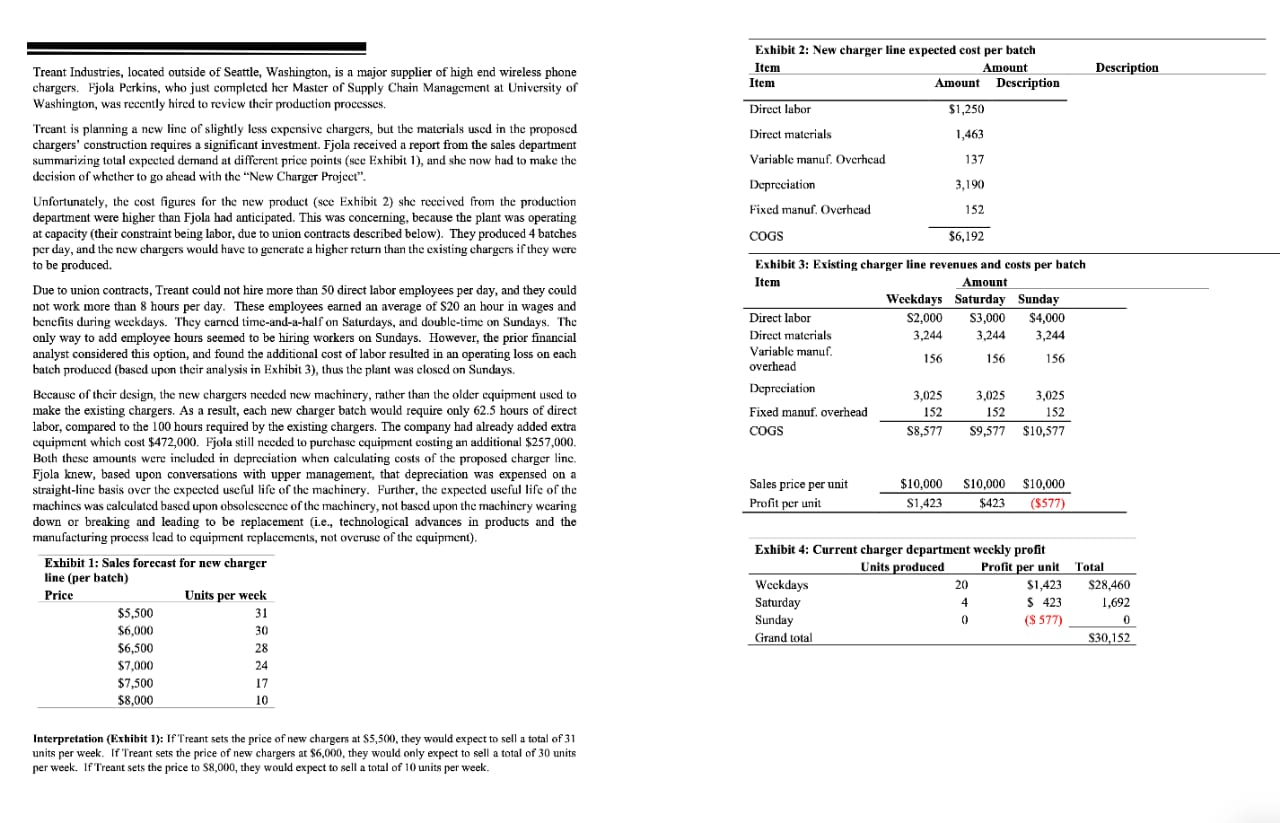

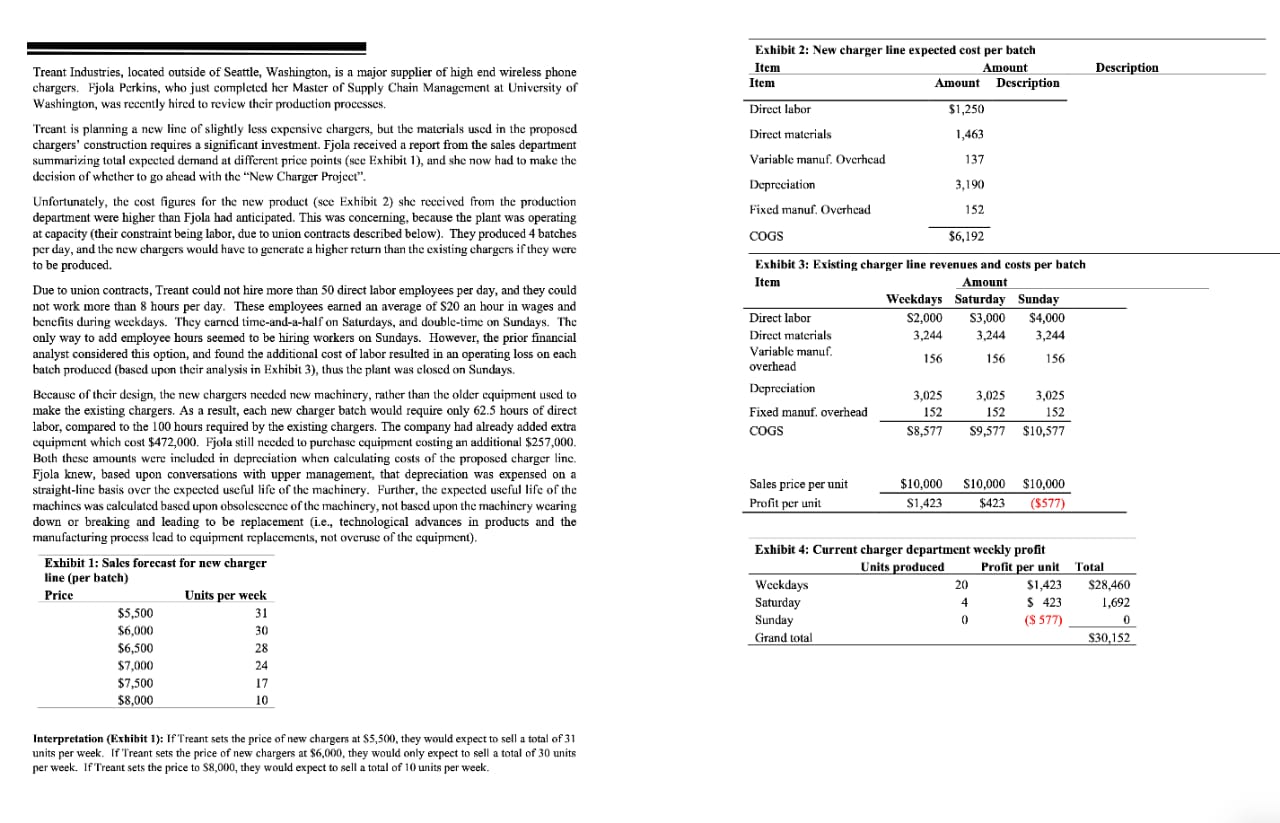

quuired 1. For Question I, ignore the existence ofthe new charger line. Fjola is considering how to improve Treant's short-run performance. Is it accurate that producing chargers from the existing line on Sundays is a bad idea? Should Treant produce chargers on Sundays, or not? Provide calculations to support your conclusion. _ 2. Suppose that Fjola decides to produce ten new charger batches each week without changing employees' current schedules (i.e., what hours and dates they work), and sell them at a price of $8,000. a. For Question 20 's anabm's, please ignore the cost of the new equipment. How much better or worse o' nancially would Treant Industries be on a weekly basis next year? _ b. The head of manufacturing has requested a meeting with Fjola. \"This new charger project is a mess! Costs are all over the place! I am thinking about pulling the plug on the whole thing! Unless we can be better off in fteen geeks producing new chargers (rather than not producing new chargers), I am canning the whole thing!\" Given the head of manufacturing's criteria, should Fjola produce new chargers? Provide calculations to support your answer. _ 3. Refer to Exhibit 1 for the association between sales price and total quantity demanded for new chargers. You are given free rein to determine any production plan you would like, only restricted by the rules set forth by the union. What weekly production plan for chargers, for both new and existing, and new charger batch price would maximize Treant Industries' protability? How much better off would Treant Industries be using your suggested production plan, compared to the current production plan (see Exhibit 4)? _ 4. Explain, in no more than four sentences, why you included the costs and benets you did in the above problems. Be descriptive- Exhibit 2: New charger line expected cost per batch Treant Industries, located outside of Seattle, Washington, is a major supplier of high end wireless phone Item Amount Description chargers. Fjola Perkins, who just completed her Master of Supply Chain Management at University of Item Amount Description Washington, was recently hired to review their production processes, Direct labor $1,250 I'reant is planning a new line of slightly less expensive chargers, but the materials used in the proposed chargers' construction requires a significant investment. Fjola received a report from the sales department Direct materials 1,463 summarizing total expected demand at different price points (see Exhibit 1), and she now had to make the Variable manuf. Overhead 137 decision of whether to go ahead with the "New Charger Project". Depreciation 3,190 Unfortunately, the cost figures for the new product (see Exhibit 2) she received from the production department were higher than Fjola had anticipated. This was concerning, because the plant was operating Fixed manuf. Overhead 152 at capacity (their constraint being labor, due to union contracts described below). They produced 4 batches COGS $6,192 per day, and the new chargers would have to generate a higher return than the existing chargers if they were to be produced. Exhibit 3: Existing charger line revenues and costs per batch Due to union contracts, Treant could not hire more than 50 direct labor employees per day, and they could Item Amount not work more than 8 hours per day. These employees earned an average of $20 an hour in wages and Weekdays Saturday Sunday benefits during weekdays. They carned time-and-a-half on Saturdays, and double-time on Sundays. The Direct labor $2,000 $3,000 $4,000 only way to add employee hours seemed to be hiring workers on Sundays. However, the prior financial Direct materials 3.244 3.244 3.244 analyst considered this option, and found the additional cost of labor resulted in an operating loss on each Variable manuf. batch produced (based upon their analysis in Exhibit 3), thus the plant was closed on Sundays. overhead 156 156 156 Because of their design, the new chargers needed new machinery, rather than the older equipment used to Depreciation 3.025 3.025 3.025 make the existing chargers. As a result, each new charger batch would require only 62.5 hours of direct Fixed manuf. overhead 152 152 152 labor, compared to the 100 hours required by the existing chargers. The company had already added extra equipment which cost $472,000. Fjola still needed to purchase equipment costing an additional $257,000. COGS $8,577 $9,577 $10,577 Both these amounts were included in depreciation when calculating costs of the proposed charger line. Fjola knew, based upon conversations with upper management, that depreciation was expensed on a straight-line basis over the expected useful life of the machinery. Further, the expected useful life of the Sales price per unit $10,000 $10,000 $10,000 machines was calculated based upon obsolescence of the machinery, not based upon the machinery wearing Profit per unit $1,423 $423 ($577 down or breaking and leading to be replacement (ie., technological advances in products and the manufacturing process lead to equipment replacements, not overuse of the equipment). Exhibit 4: Current charger department weekly profit Exhibit 1: Sales forecast for new charger line (per batch) Units produced Profit per unit Total Price Units per week Weekdays 20 $1,423 $28.460 $5,500 $ 423 1,692 31 Saturday $6,000 30 Sunday ($ 577) $6,500 28 Grand total $30.152 $7,000 24 $7,500 17 $8,000 10 Interpretation (Exhibit 1): IfTreant sets the price of new chargers at $5,500, they would expect to sell a total of 31 units per week. If Treant sets the price of new chargers at $6,000, they would only expect to sell a total of 30 units per week. If Treant sets the price to $8,000, they would expect to sell a total of 10 units per week