Question

Please I need solution for this issue with all the details .please you can write the answer typing and not write by hand,so that I

Please I need solution for this issue with all the details .please you can write the answer typing and not write by hand,so that I can read and understand your answer clearly.I need step by step solution to the following this question asap.

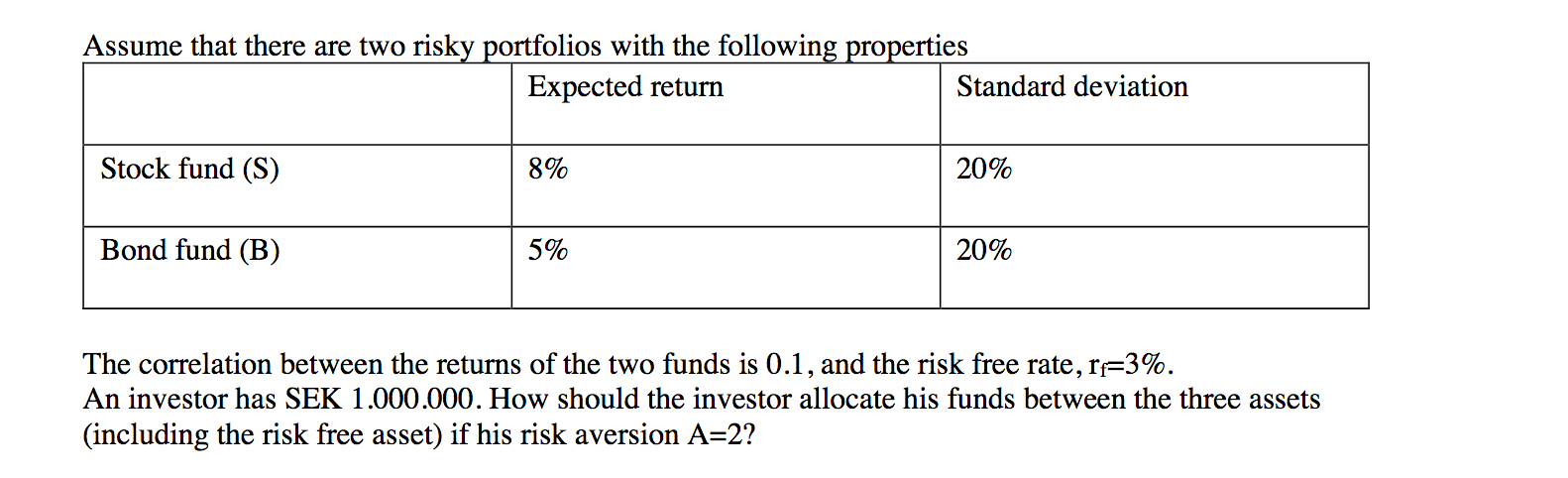

Assume that there are two risky portfolios with the following properties Expected return Standard deviation Stock fund (S) 8% 20% Bond fund (B) 5% 20% The correlation between the returns of the two funds is 0.1, and the risk free rate, rf=3%. An investor has SEK 1.000.000. How should the investor allocate his funds between the three assets (including the risk free asset) if his risk aversion A=2

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management Fundamentals

Authors: R. Charles Moyer, James R. McGuigan, Ramesh P. Rao

1st Edition

0324015771, 9780324015775