Question: please I need this, step by step with formulas, avoid using excel. CASE 33 Security Software, Inc. communication in a highly secure and efficient process.

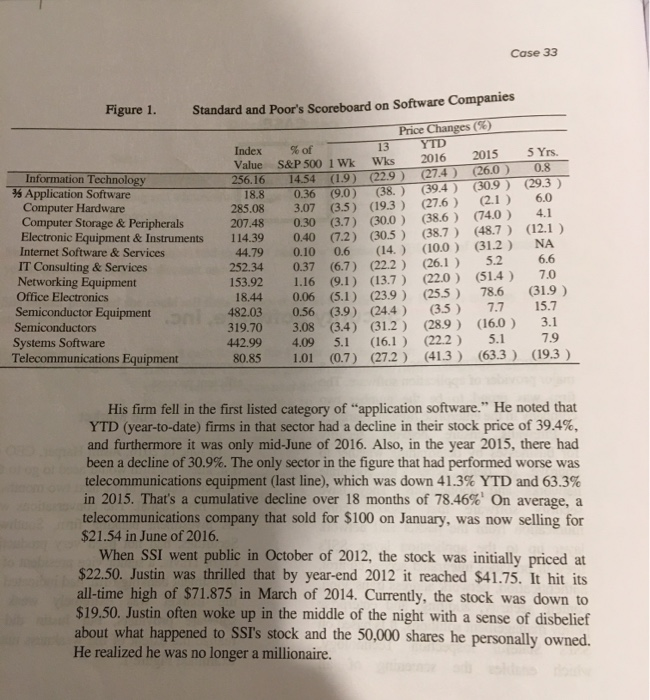

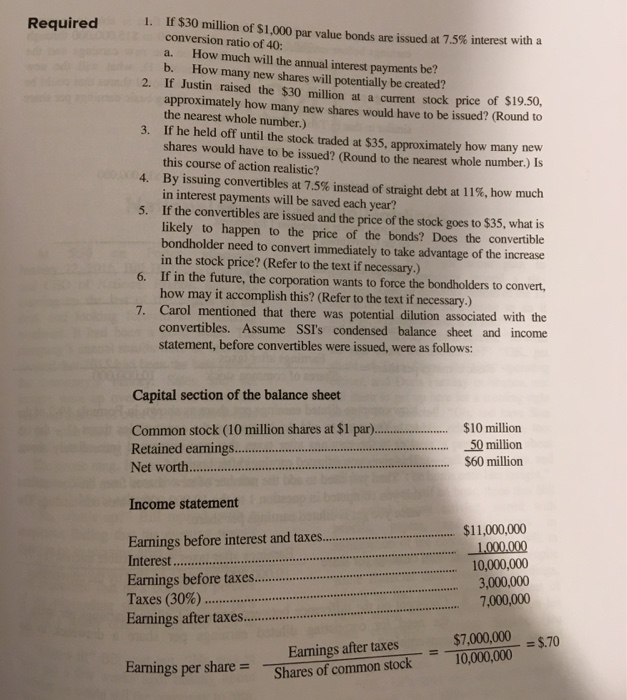

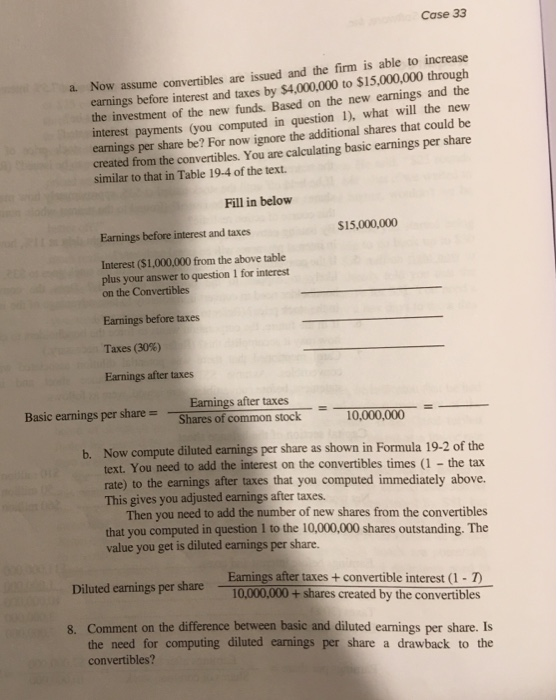

CASE 33 Security Software, Inc. communication in a highly secure and efficient process. The Market Security Software, Inc. (SSI) was a major provider of application software. The firm was proud to be the number two company in the enterprise firewall market. Firewalls ensure network Security for businesses by determining whether to approve or deny access to corporate networks and applications. They have security software that inspects com- munication from the packet and network layer up to the application layer. SSI's firewall provides integrated access control, authentication, network address translation, content security, auditing, and enterprise policy management solutions. It is based on SSI's Stateful Inspection Technology, which enables the screening of all In June of 2016, Justin Harper, CEO of SSI, knew the firm would need to go to the financial markets in the next two months to raise new capital. The conversations with his investment banking firm, Southwest Securities, had not been very productive. Carol Travis, a senior vice president of the investment banking firm, had indicated that the market was extremely weak for software providers, but Justin did not realize the extent of the weakness until he examined Figure 1. Case 33 Figure 1. Standard and Poor's Scoreboard on Software Companies Price Changes (56) Index % of 13 YTD Value S&P 500 1 Wk Wks 2016 2015 Information Technology 256.16 14.54 (1.9) (22.9 ) (27.4) (26.0) Application Software 18.8 0.36 (9.0) (38.) (39.4) (30.9 ) Computer Hardware 285.08 3.07 (3.5) (19.3) (27.6) (2.1) Computer Storage & Peripherals 207.48 0.30 (3.7) (30.0) (38.6) (74.0) Electronic Equipment & Instruments 114.39 0.40 (7.2) (30.5) (38.7) Internet Software & Services (48.7) 44.79 0.10 0.6 (14.) (10.0) (31.2) IT Consulting & Services 252.34 0.37 (6.7) Networking Equipment (22.2) (26.1 ) 5.2 153.92 1.16 (9.1) (13.7 ) (22.0) (51.4) Office Electronics 18.44 0.06 (5.1) (23.9 ) (255) 78.6 Semiconductor Equipment 482.03 0.56 (3.9) (24.4) (3.5) 7.7 Semiconductors 3.08 (3.4) (31.2) (28.9 ) (16.0) Systems Software 442.99 4 .09 5.1 (16.1 ) (22.2) 5.1 Telecommunications Equipment 80.85 1.01 (0.7) (27.2) (41.3) (63.3) 5 Yrs. 0.8 (29.3 ) 6.0 4.1 (12.1 ) NA 6.6 7.0 (31.9) 15.7 3.1 7.9 (19.3 ) His firm fell in the first listed category of application software." He noted that YTD (year-to-date) firms in that sector had a decline in their stock price of 39.4%, and furthermore it was only mid-June of 2016. Also, in the year 2015, there had been a decline of 30.9%. The only sector in the figure that had performed worse was telecommunications equipment (last line), which was down 41.3% YTD and 63.3% in 2015. That's a cumulative decline over 18 months of 78.46%' On average, a telecommunications company that sold for $100 on January, was now selling for $21.54 in June of 2016. When SSI went public in October of 2012, the stock was initially priced at $22.50. Justin was thrilled that by year-end 2012 it reached $41.75. It hit its all-time high of $71.875 in March of 2014. Currently, the stock was down to $19.50. Justin often woke up in the middle of the night with a sense of disbelief about what happened to SSI's stock and the 50,000 shares he personally owned. He realized he was no longer a millionaire. SSI's Need for Capital The firm needed to program of resear position of leadership in the em peeded to raise $30 million in the financial markets to continue with its of research and development. R&D was absolutely essential to maintain a of leadership in the software related firewall industry. Justin indicated that Grm would not be willing to sell additional shares to the public for $19.50 when initial public offering had been at $22.50 and as recently as March of 2014. the had sold at $71.875. Although there had been ups and downs in quarterly pings due to a weak economy, the company was still as fundamentally sound as the day it went public. When Justin approached his investment banker Carol Travis with the idea of euing debt instead of stock, she balked. She explained that similar firms in his industry had bonds that were rated B to Ba by Moody's and BB by Standard and Poor's. This meant they were classified as junk bonds. To be politically correct, most investment bankers call them 'high yield bonds, but everybody knew what that really meant. Not only did high yield bonds carry high interest rates (2-4% over high quality bonds), but currently there was a very limited market for them, particularly when they were being issued by firms in the computer software industry. In response to Carol's very lukewarm response to the idea of a bond issue, Justin asked, "Isn't there someway SSI could sweeten up the deal so that bonds might be acceptable for investors." Carol's Response Carol responded, now you are thinking more realistically." While there was no market right now for a debt issue of SSI, if the debt had an option to convert to common stock (while still paying interest), then investors would be interested. Justin quickly snapped back that he was not interested in adding new shares at the current low price of $19.50. She encouraged Justin to calm down by saying, "One of the advantages of convertible bonds is that they do not have to be convertible at the current market Value of common stock. There can be a premium built in the price of the common stock into which the bonds are convertible." Carol went on to suggest a 1,000 par Value bond might be convertible into 40 shares of common stock. in was not familiar with the lingo associated with convertibles and asked for er explanation. Carol explained that a conversion ratio of 40 on a $1,000 par meant that the shares were effectively being priced at $25 per share par value/40 conversion ratio). Assuming the bonds had a ten-year life, if the bondholders converted in the future, they would be effectively buying a fuller explanation. Carole value bond meant that the shal ($1,000 par value/40 con and when the bondholders the stock at $25 per share. Case 33 If the stock, which was currently priced at $19.50, never got up to a market value of $25 over the life of the bond, conversion would not take place. However, if the stock went to over $25. perhaps to $30 or $40. bondholders might have some desire to convert that is, trade in an initially priced $1,000 par value bond for 40 shares per bond at an effective cost of $25 per share). Justin liked the concept of potentially getting $25 per share for SSI's currently priced stock of $19.50, but he was not fully sold on the idea. He said, "$25 sounds good based on the terrible hit we have taken in the market, but what if we waited to issue common stock until the stock got back up to $30 or higher, wouldn't we be better off?" Now it was Carol's turn to snap back. "Justin, it's about time you started being more realistic. You have no assurance that SSI stock is going to go back up to $30 or higher or even $25 for that matter. Besides, you need $30 million right now to remain competitive in the firewall software market. I've already told you that the straight debt market (nonconvertible) is not a viable alternative for SSI. You need a sweetener to attract investors." Justin replied, "Let me have a few days to think this over." A Second Meeting When Justin and Carol got back together five days later, he indicated that he had discussed the matter with his chief financial officer and various members of the board of directors and they were amenable to a convertible issue. Carol further fueled his interest by saying, "convertibles normally can be issued at a lower rate than straight bonds." She went on to say that although straight bonds likely could not be issued at this point in time, comparable firms to SSI with straight debt already outstanding were paying 11 percent. If similar rated debt (B or Ba) were issued by SSI, but sweetened by the convertibility feature, the rate would probably only be 7.5%." Justin certainly liked this factor and asked if there were any other factors he needed to consider. Carol was quick to answer, "Yes, convertible bonds are potentially dilutive to earnings per share and that is something you will definitely need to consider-but first let's go over some basics." Pequired . $ 30 million of $1.000 par value bonds are issued at 7.5% interest with a conversion ratio of 40: a. How much will the annual interest payments be? b. How many new shares will potentially be created? 2. If Justin raised the $30 million at a current stock price of $19.50, approximately how many new shares would have to be issued? (Round to the nearest whole number.) 3. If he held off until the stock traded at $35, approximately how many new shares would have to be issued? (Round to the nearest whole number.) Is this course of action realistic? 4. By issuing convertibles at 7.5% instead of straight debt at 11%, how much in interest payments will be saved each year? 5. If the convertibles are issued and the price of the stock goes to $35, what is likely to happen to the price of the bonds? Does the convertible bondholder need to convert immediately to take advantage of the increase in the stock price? (Refer to the text if necessary.) 6. If in the future, the corporation wants to force the bondholders to convert, how may it accomplish this? (Refer to the text if necessary.) 7. Carol mentioned that there was potential dilution associated with the convertibles. Assume SSI's condensed balance sheet and income statement, before convertibles were issued, were as follows: Capital section of the balance sheet Common stock (10 million shares at $1 par)..... Retained earnings............ Net worth.. $10 million 50 million $60 million Income statement Earnings before interest and taxes..... Interest ......................... Earnings before taxes..... ........ Taxes (30%) ......... Earnings after taxes............ $11,000,000 1.000.000 10,000,000 3,000,000 7,000,000 $7,000,000 = $.70 Earnings after taxes Shares of common stock 10,000,000 Earnings per share Shares of common stock Case 33 a Now assume convertibles are issued and the firm is able to increase earnings before interest and taxes by $4,000,000 to $15,000,000 through the investment of the new funds. Based on the new earnings and the interest payments (you computed in question 1), what will the new earnings per share be? For now ignore the additional shares that could be created from the convertibles. You are calculating basic earnings per share similar to that in Table 19-4 of the text. Fill in below $15,000,000 Earnings before interest and taxes Interest ($1,000,000 from the above table plus your answer to question 1 for interest on the Convertibles Earnings before taxes Taxes (30%) Earnings after taxes Earnings after taxes Shares of common stock Basic earnings per share = 10,000,000 b. Now compute diluted earnings per share as shown in Formula 19-2 of the text. You need to add the interest on the convertibles times (1 - the tax rate) to the earnings after taxes that you computed immediately above. This gives you adjusted earnings after taxes. Then you need to add the number of new shares from the convertibles that you computed in question 1 to the 10,000,000 shares outstanding. The value you get is diluted earnings per share. Diluted earnings per share Earnings after taxes + convertible interest (1 - 1) - 10,000,000+ shares created by the convertibles 8. Comment on the difference between basic and diluted earnings per share. Is the need for computing diluted earnings per share a drawback to the convertibles

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts