Answered step by step

Verified Expert Solution

Question

1 Approved Answer

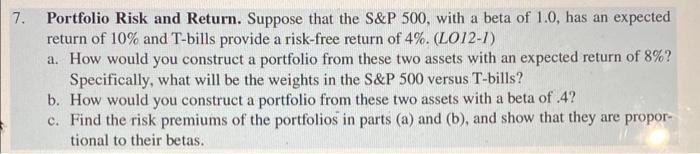

Please include equations Portfolio Risk and Return. Suppose that the S&P 500, with a beta of 1.0 , has an expected return of 10% and

Please include equations

Portfolio Risk and Return. Suppose that the S\&P 500, with a beta of 1.0 , has an expected return of 10% and T-bills provide a risk-free return of 4%. (LO12-I) a. How would you construct a portfolio from these two assets with an expected return of 8% ? Specifically, what will be the weights in the S\&P 500 versus T-bills? b. How would you construct a portfolio from these two assets with a beta of .4? c. Find the risk premiums of the portfolios in parts (a) and (b), and show that they are proportional to their betas Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance A Contemporary Application Of Theory To Policy

Authors: David N Hyman

10th Edition

053875446X, 978-0538754460