Please look at the notes attached.

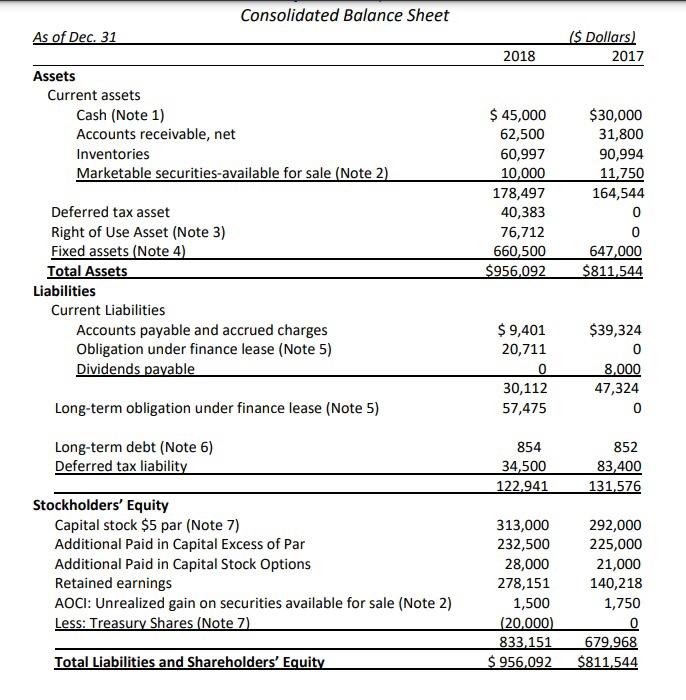

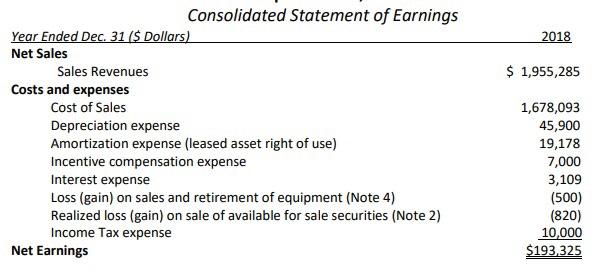

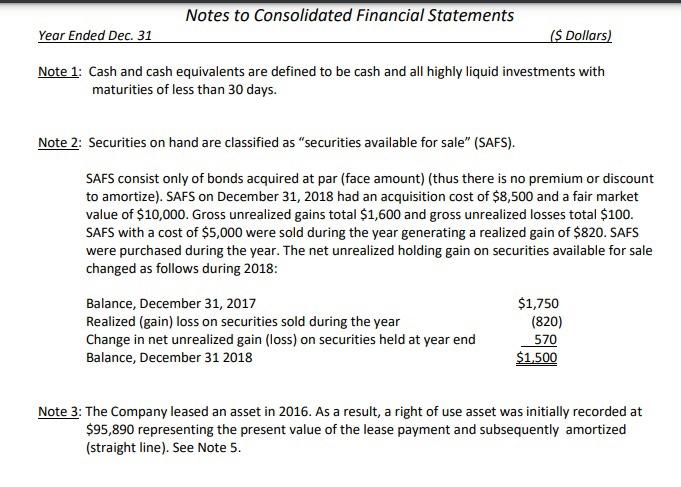

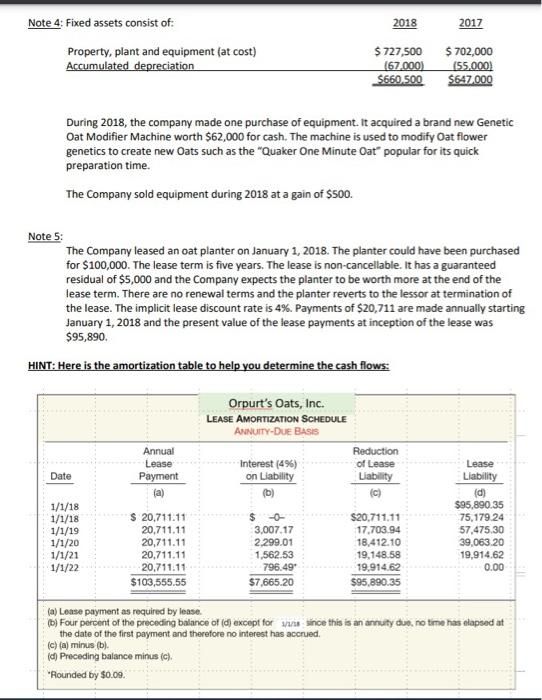

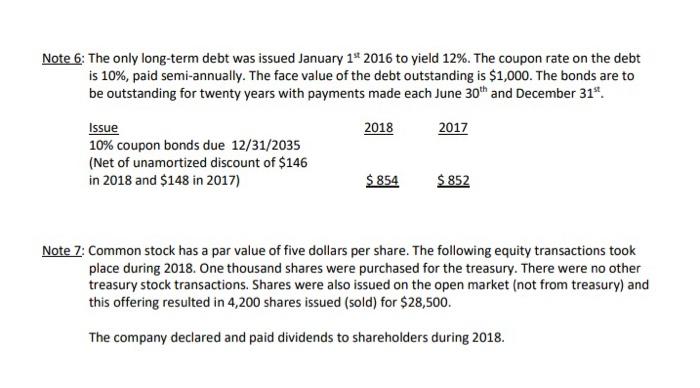

Prepare an indirect method statement of cash flows for 2018. A T-account wor provided to assist you but you will only be rewarded for answering the questi provided on the blank Statement of Cash Flows. Consolidated Balance Sheet Consolidated Statement of Earnings Year Ended Dec. 31 (\$ Dollars) 2018 Net Sales Sales Revenues $1,955,285 Costs and expenses Cost of Sales Depreciation expense Amortization expense (leased asset right of use) Incentive compensation expense 1,678,093 Interestexpense3,109 Loss (gain) on sales and retirement of equipment (Note 4) Realized loss (gain) on sale of available for sale securities (Note 2) (820) Income Tax expense Net Earnings Note 1: Cash and cash equivalents are defined to be cash and all highly liquid investments with maturities of less than 30 days. Note 2: Securities on hand are classified as "securities available for sale" (SAFS). SAFS consist only of bonds acquired at par (face amount) (thus there is no premium or discount to amortize). SAFS on December 31,2018 had an acquisition cost of $8,500 and a fair market value of $10,000. Gross unrealized gains total $1,600 and gross unrealized losses total $100. SAFS with a cost of $5,000 were sold during the year generating a realized gain of $820. SAFS were purchased during the year. The net unrealized holding gain on securities available for sale changed as follows during 2018: Note 3: The Company leased an asset in 2016. As a result, a right of use asset was initially recorded at $95,890 representing the present value of the lease payment and subsequently amortized (straight line). See Note 5. During 2018, the company made one purchase of equipment. It acquired a brand new Genetic Oat Modifier Machine worth $62,000 for cash. The machine is used to modify Oat flower genetics to create new Oats such as the "Quaker One Minute Oat" popular for its quick preparation time. The Company sold equipment during 2018 at a gain of $500. Note 5: The Company leased an oat planter on January 1, 2018. The planter could have been purchased for $100,000. The lease term is five years. The lease is non-cancellable. It has a guaranteed residual of $5,000 and the Company expects the planter to be worth more at the end of the lease term. There are no renewal terms and the planter reverts to the lessor at termination of the lease. The implicit lease discount rate is 4%. Payments of $20,711 are made annually starting January 1, 2018 and the present value of the lease payments at inception of the lease was $95,890. HINT: Here is the amortization table to help you determine the cash flows: (a) Lease payment as required by lease. (b) Four percent of the preceding balance of (d) except for i/has since this is an annuly du0, no time has nlapsed at the date of the first payment and therefore no interest has accrued. (c) (a) minus (b). (d) Preceding balance minus (c). "Flounded by $0.09. Note 6: The only long-term debt was issued January 1tt2016 to yield 12%. The coupon rate on the debt is 10%, paid semi-annually. The face value of the debt outstanding is $1,000. The bonds are to be outstanding for twenty years with payments made each June 30th and December 31st. Note 7: Common stock has a par value of five dollars per share. The following equity transactions took place during 2018. One thousand shares were purchased for the treasury. There were no other treasury stock transactions. Shares were also issued on the open market (not from treasury) and this offering resulted in 4,200 shares issued (sold) for $28,500. The company declared and paid dividends to shareholders during 2018. Prepare an indirect method statement of cash flows for 2018. A T-account wor provided to assist you but you will only be rewarded for answering the questi provided on the blank Statement of Cash Flows. Consolidated Balance Sheet Consolidated Statement of Earnings Year Ended Dec. 31 (\$ Dollars) 2018 Net Sales Sales Revenues $1,955,285 Costs and expenses Cost of Sales Depreciation expense Amortization expense (leased asset right of use) Incentive compensation expense 1,678,093 Interestexpense3,109 Loss (gain) on sales and retirement of equipment (Note 4) Realized loss (gain) on sale of available for sale securities (Note 2) (820) Income Tax expense Net Earnings Note 1: Cash and cash equivalents are defined to be cash and all highly liquid investments with maturities of less than 30 days. Note 2: Securities on hand are classified as "securities available for sale" (SAFS). SAFS consist only of bonds acquired at par (face amount) (thus there is no premium or discount to amortize). SAFS on December 31,2018 had an acquisition cost of $8,500 and a fair market value of $10,000. Gross unrealized gains total $1,600 and gross unrealized losses total $100. SAFS with a cost of $5,000 were sold during the year generating a realized gain of $820. SAFS were purchased during the year. The net unrealized holding gain on securities available for sale changed as follows during 2018: Note 3: The Company leased an asset in 2016. As a result, a right of use asset was initially recorded at $95,890 representing the present value of the lease payment and subsequently amortized (straight line). See Note 5. During 2018, the company made one purchase of equipment. It acquired a brand new Genetic Oat Modifier Machine worth $62,000 for cash. The machine is used to modify Oat flower genetics to create new Oats such as the "Quaker One Minute Oat" popular for its quick preparation time. The Company sold equipment during 2018 at a gain of $500. Note 5: The Company leased an oat planter on January 1, 2018. The planter could have been purchased for $100,000. The lease term is five years. The lease is non-cancellable. It has a guaranteed residual of $5,000 and the Company expects the planter to be worth more at the end of the lease term. There are no renewal terms and the planter reverts to the lessor at termination of the lease. The implicit lease discount rate is 4%. Payments of $20,711 are made annually starting January 1, 2018 and the present value of the lease payments at inception of the lease was $95,890. HINT: Here is the amortization table to help you determine the cash flows: (a) Lease payment as required by lease. (b) Four percent of the preceding balance of (d) except for i/has since this is an annuly du0, no time has nlapsed at the date of the first payment and therefore no interest has accrued. (c) (a) minus (b). (d) Preceding balance minus (c). "Flounded by $0.09. Note 6: The only long-term debt was issued January 1tt2016 to yield 12%. The coupon rate on the debt is 10%, paid semi-annually. The face value of the debt outstanding is $1,000. The bonds are to be outstanding for twenty years with payments made each June 30th and December 31st. Note 7: Common stock has a par value of five dollars per share. The following equity transactions took place during 2018. One thousand shares were purchased for the treasury. There were no other treasury stock transactions. Shares were also issued on the open market (not from treasury) and this offering resulted in 4,200 shares issued (sold) for $28,500. The company declared and paid dividends to shareholders during 2018