Answered step by step

Verified Expert Solution

Question

1 Approved Answer

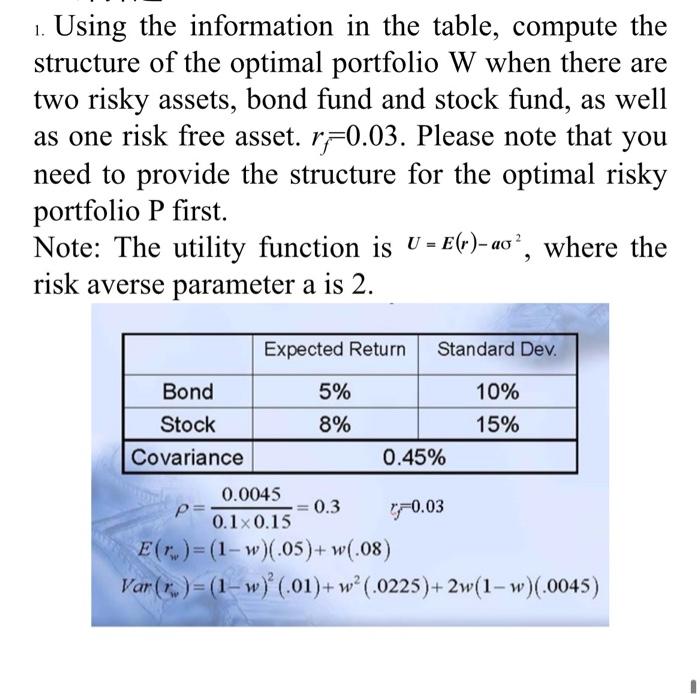

please make sure the answer is correct and attach with formulars that are correct. thanks 1. Using the information in the table, compute the structure

please make sure the answer is correct and attach with formulars that are correct. thanks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Michael Saylor On Bitcoin The Very First Interviews

Authors: Coinan The Barbarian ,Satoshi Nakamoto

1st Edition

979-8423442019