Answered step by step

Verified Expert Solution

Question

1 Approved Answer

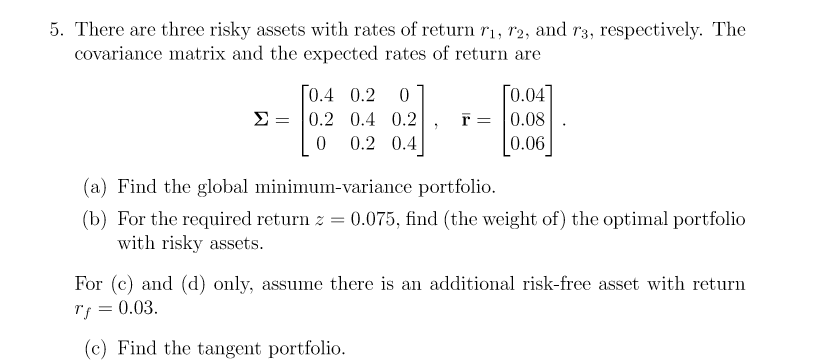

Please make sure your answer is correct! Please do not copy other wrong answers There are three risky assets with rates of return r1,r2, and

Please make sure your answer is correct! Please do not copy other wrong answers

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Infographic Guide To Personal Finance

Authors: Michele Cagan CPA, Elisabeth Lariviere

1st Edition

1507204663, 978-1507204665