please make the statement of cash flows for this. Quick response =thumbs up

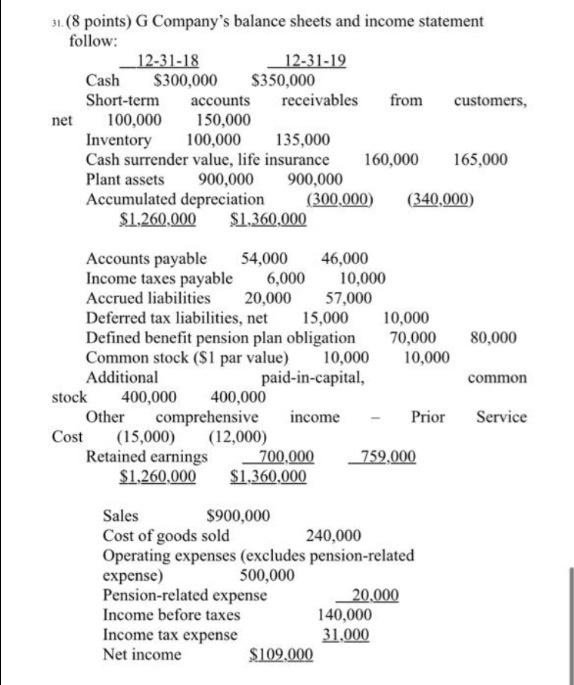

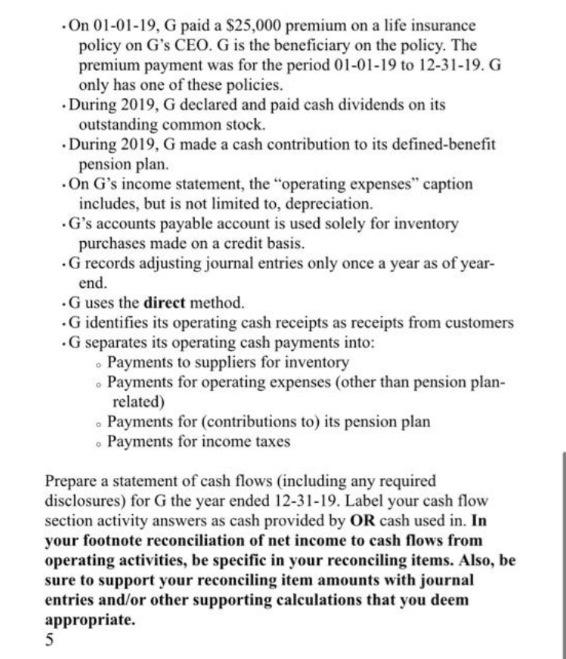

On 01-01-19, G paid a $25,000 premium on a life insurance policy on G's CEO. G is the beneficiary on the policy. The premium payment was for the period 01-01-19 to 12-31-19. G only has one of these policies. During 2019, G declared and paid cash dividends on its outstanding common stock. . During 2019, G made a cash contribution to its defined-benefit pension plan. On G's income statement, the operating expenses" caption includes, but is not limited to, depreciation. G's accounts payable account is used solely for inventory purchases made on a credit basis. G records adjusting journal entries only once a year as of year- end. G uses the direct method. G identifies its operating cash receipts as receipts from customers G separates its operating cash payments into: Payments to suppliers for inventory Payments for operating expenses (other than pension plan- related) . Payments for contributions to) its pension plan . Payments for income taxes Prepare a statement of cash flows (including any required disclosures) for G the year ended 12-31-19. Label your cash flow section activity answers as cash provided by OR cash used in. In your footnote reconciliation of net income to cash flows from operating activities, be specific in your reconciling items. Also, be sure to support your reconciling item amounts with journal entries and/or other supporting calculations that you deem appropriate. 5 31.(8 points) G Company's balance sheets and income statement follow: 12-31-18 12-31-19 Cash $300,000 $350,000 Short-term accounts receivables from customers, net 100,000 150,000 Inventory 100,000 135,000 Cash surrender value, life insurance 160,000 165,000 Plant assets 900,000 900,000 Accumulated depreciation (300.000) (340,000) $1,260,000 $1.360,000 Accounts payable 54,000 46,000 Income taxes payable 6,000 10,000 Accrued liabilities 20,000 57,000 Deferred tax liabilities, net 15,000 10,000 Defined benefit pension plan obligation 70,000 80,000 Common stock ($1 par value) 10,000 10,000 Additional paid-in-capital, common stock 400,000 400,000 Other comprehensive income Prior Service Cost (15,000) (12,000) Retained earnings 700,000 759,000 $1,260,000 $1.360,000 Sales $900,000 Cost of goods sold 240,000 Operating expenses (excludes pension-related expense) 500,000 Pension-related expense 20.000 Income before taxes 140,000 Income tax expense 31.000 Net income $109,000 On 01-01-19, G paid a $25,000 premium on a life insurance policy on G's CEO. G is the beneficiary on the policy. The premium payment was for the period 01-01-19 to 12-31-19. G only has one of these policies. During 2019, G declared and paid cash dividends on its outstanding common stock. . During 2019, G made a cash contribution to its defined-benefit pension plan. On G's income statement, the operating expenses" caption includes, but is not limited to, depreciation. G's accounts payable account is used solely for inventory purchases made on a credit basis. G records adjusting journal entries only once a year as of year- end. G uses the direct method. G identifies its operating cash receipts as receipts from customers G separates its operating cash payments into: Payments to suppliers for inventory Payments for operating expenses (other than pension plan- related) . Payments for contributions to) its pension plan . Payments for income taxes Prepare a statement of cash flows (including any required disclosures) for G the year ended 12-31-19. Label your cash flow section activity answers as cash provided by OR cash used in. In your footnote reconciliation of net income to cash flows from operating activities, be specific in your reconciling items. Also, be sure to support your reconciling item amounts with journal entries and/or other supporting calculations that you deem appropriate. 5 31.(8 points) G Company's balance sheets and income statement follow: 12-31-18 12-31-19 Cash $300,000 $350,000 Short-term accounts receivables from customers, net 100,000 150,000 Inventory 100,000 135,000 Cash surrender value, life insurance 160,000 165,000 Plant assets 900,000 900,000 Accumulated depreciation (300.000) (340,000) $1,260,000 $1.360,000 Accounts payable 54,000 46,000 Income taxes payable 6,000 10,000 Accrued liabilities 20,000 57,000 Deferred tax liabilities, net 15,000 10,000 Defined benefit pension plan obligation 70,000 80,000 Common stock ($1 par value) 10,000 10,000 Additional paid-in-capital, common stock 400,000 400,000 Other comprehensive income Prior Service Cost (15,000) (12,000) Retained earnings 700,000 759,000 $1,260,000 $1.360,000 Sales $900,000 Cost of goods sold 240,000 Operating expenses (excludes pension-related expense) 500,000 Pension-related expense 20.000 Income before taxes 140,000 Income tax expense 31.000 Net income $109,000