please need urgent answer for this question

i really appreciate it

brother this is the total question thanks

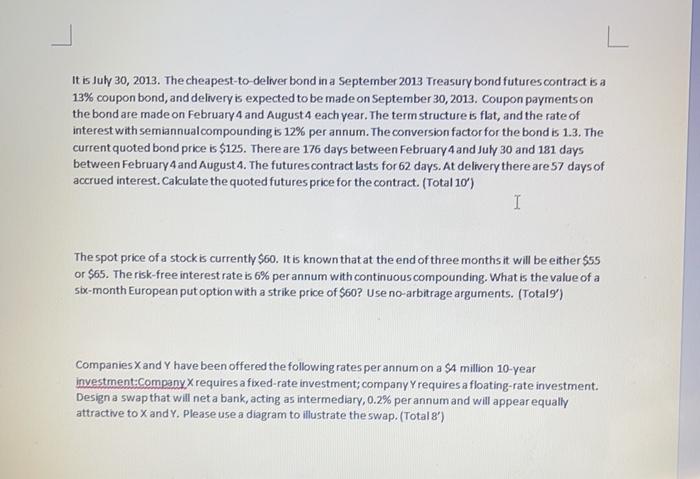

Companies X and Y have been offered the following rates per annum on a $1 million 10-year investment:Company X requires a fixed-rate investment; company Yrequires a floating-rate investment. Design a swap that will net a bank, acting as intermediary, 0.2% per annum and will appear equally attractive to X and Y. Please use a diagram to illustrate the swap. (Total 8') L. It is July 30, 2013. The cheapest-to-deliver bond in a September 2013 Treasury bond futures contract is a 13% coupon bond, and delivery is expected to be made on September 30, 2013. Coupon payments on the bond are made on February 4 and August 4 each year. The term structure is flat, and the rate of interest with semiannualcompounding is 12% per annum. The conversion factor for the bond is 1.3. The current quoted bond price is $125. There are 176 days between February 4 and July 30 and 181 days between February 4 and August 4. The futures contract lasts for 62 days. At delivery there are 57 days of accrued interest. Calculate the quoted futures price for the contract. (Total 10') I The spot price of a stock is currently $60. It is known that at the end of three months it will be either $55 or $65. The risk-free interest rate is 6% per annum with continuous compounding. What is the value of a Sbx-month European put option with a strike price of $60? Use no-arbitrage arguments. (Total) Companies X and Y have been offered the following rates per annum on a SA million 10-year Investment:Compeny X requires a fixed-rate investment; company Y requires a floating-rate investment. Design a swap that will net a bank, acting as intermediary, 0.2% per annum and will appear equally attractive to Xandy. Please use a diagram to illustrate the swap. (Total 8') Companies X and Y have been offered the following rates per annum on a $1 million 10-year investment:Company X requires a fixed-rate investment; company Yrequires a floating-rate investment. Design a swap that will net a bank, acting as intermediary, 0.2% per annum and will appear equally attractive to X and Y. Please use a diagram to illustrate the swap. (Total 8') L. It is July 30, 2013. The cheapest-to-deliver bond in a September 2013 Treasury bond futures contract is a 13% coupon bond, and delivery is expected to be made on September 30, 2013. Coupon payments on the bond are made on February 4 and August 4 each year. The term structure is flat, and the rate of interest with semiannualcompounding is 12% per annum. The conversion factor for the bond is 1.3. The current quoted bond price is $125. There are 176 days between February 4 and July 30 and 181 days between February 4 and August 4. The futures contract lasts for 62 days. At delivery there are 57 days of accrued interest. Calculate the quoted futures price for the contract. (Total 10') I The spot price of a stock is currently $60. It is known that at the end of three months it will be either $55 or $65. The risk-free interest rate is 6% per annum with continuous compounding. What is the value of a Sbx-month European put option with a strike price of $60? Use no-arbitrage arguments. (Total) Companies X and Y have been offered the following rates per annum on a SA million 10-year Investment:Compeny X requires a fixed-rate investment; company Y requires a floating-rate investment. Design a swap that will net a bank, acting as intermediary, 0.2% per annum and will appear equally attractive to Xandy. Please use a diagram to illustrate the swap. (Total 8')