Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please only answer ii, D and E 1. United Airlines has just signed a contract to purchase some A320 planes from Airbus for 200,000,000 euros.

Please only answer ii, D and E

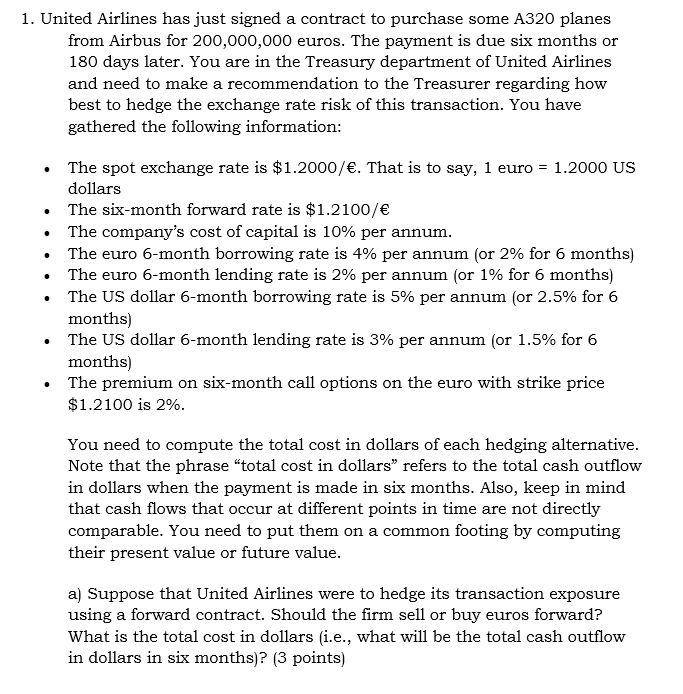

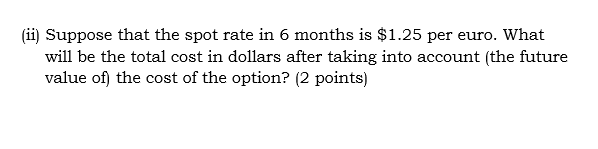

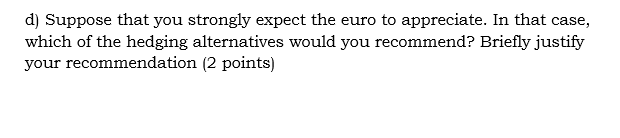

1. United Airlines has just signed a contract to purchase some A320 planes from Airbus for 200,000,000 euros. The payment is due six months or 180 days later. You are in the Treasury department of United Airlines and need to make a recommendation to the Treasurer regarding how best to hedge the exchange rate risk of this transaction. You have gathered the following information: The spot exchange rate is $1.2000/. That is to say, 1 euro = 1.2000 US dollars The six-month forward rate is $1.2100/ The company's cost of capital is 10% per annum. The euro 6-month borrowing rate is 4% per annum (or 2% for 6 months) The euro 6-month lending rate is 2% per annum (or 1% for 6 months) The US dollar 6-month borrowing rate is 5% per annum (or 2.5% for 6 months) The US dollar 6-month lending rate is 3% per annum (or 1.5% for 6 months) The premium on six-month call options on the euro with strike price $1.2100 is 2%. You need to compute the total cost in dollars of each hedging alternative. Note that the phrase "total cost in dollars" refers to the total cash outflow in dollars when the payment is made in six months. Also, keep in mind that cash flows that occur at different points in time are not directly comparable. You need to put them on a common footing by computing their present value or future value. a) Suppose that United Airlines were to hedge its transaction exposure using a forward contract. Should the firm sell or buy euros forward? What is the total cost in dollars (i.e., what will be the total cash outflow in dollars in six months)? (3 points) (ii) Suppose that the spot rate in 6 months is $1.25 per euro. What will be the total cost in dollars after taking into account (the future value of) the cost of the option? (2 points) d) Suppose that you strongly expect the euro to appreciate. In that case, which of the hedging alternatives would you recommend? Briefly justify your recommendation (2 points) e) Suppose that you expect the euro to depreciate. How much does the euro need to depreciate in order to make the call option a better alternative than the forward contract? In other words, how low does the euro have to go in value to make the call option a better alternative than the forward contract? Explain your calculations. (3 points)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started