Answered step by step

Verified Expert Solution

Question

1 Approved Answer

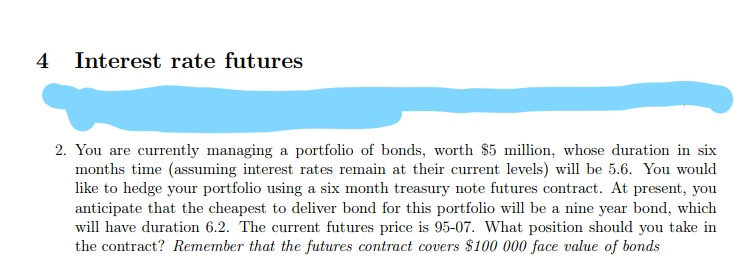

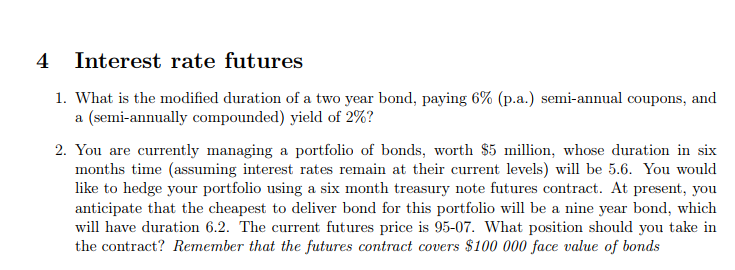

(Please only answer the question no.2 as in the first image, The current futures price, 95.07) 4 Interest rate futures 2. You are currently managing

(Please only answer the question no.2 as in the first image, The current futures price, 95.07)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Life Money An Honest Guide To Taking Control Of Your Finances

Authors: Clare Seal

1st Edition

1472272293, 978-1472272294