Answered step by step

Verified Expert Solution

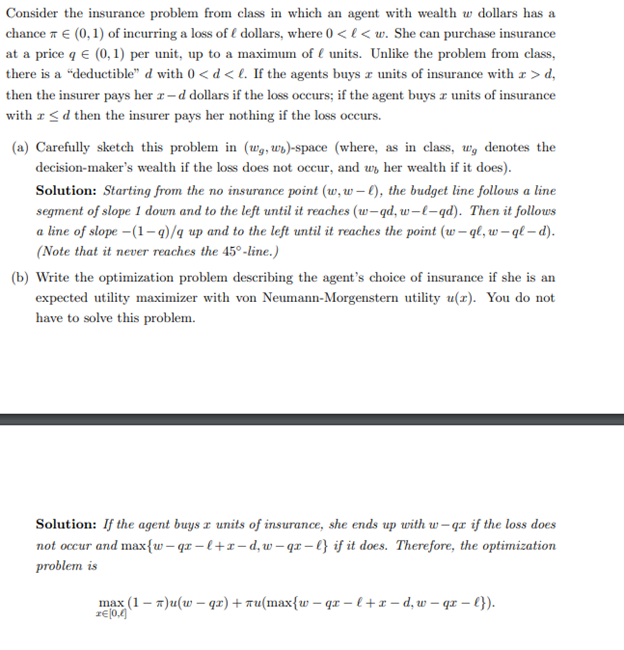

Question

1 Approved Answer

please only do: if you can teach explain steps Consider the insurance problem from class in which an agent with wealth w dollars has a

please only do: if you can teach explain steps

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Are You Ready For An ISMS Audit Based On 27001

Authors: BSI British

1st Edition

0580829138, 978-0580829130