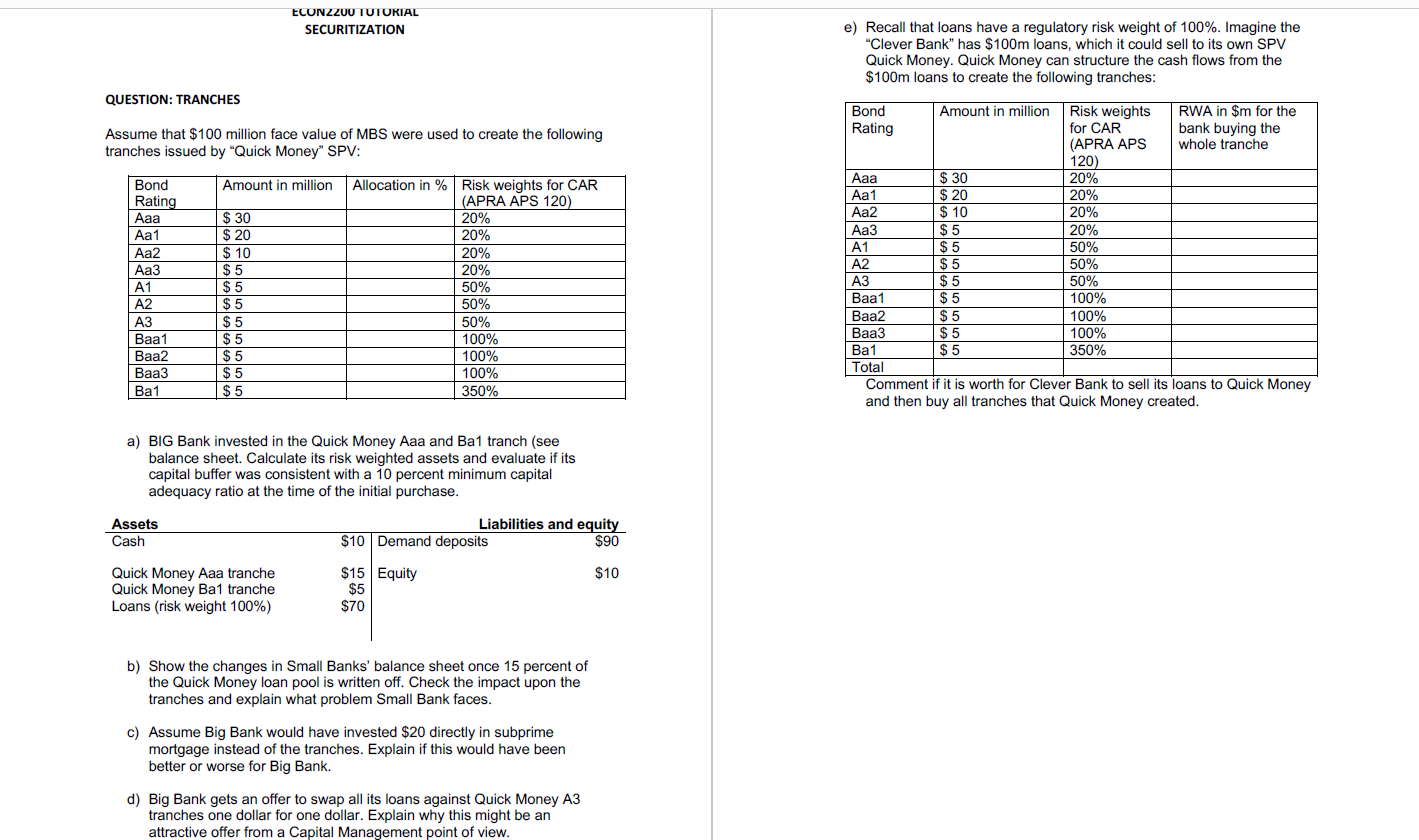

Question

--PLEASE, PLEASE HELP ANYONE? NEED THE ASSISTANCE OF A KIND NEW YEAR 2020 ANGEL? :) THANK YOU SO MUCH!! WISHING YOU AN AMAZING NEW YEAR!!

--PLEASE, PLEASE HELP ANYONE? NEED THE ASSISTANCE OF A KIND NEW YEAR 2020 ANGEL? :) THANK YOU SO MUCH!! WISHING YOU AN AMAZING NEW YEAR!! THANK YOUUU!! :) :)

**IMPORTANT NOTE: I have uploaded the necessary Securitization Tutorial 10 PDF required for this Question as an image file for your use. NO NEED TO ANSWER THE QUESTIONS IN THIS 'SECURITIZATION PDF'! (They are only for reference in the filling out of the blanks below) Please help, only need help filling in the BLANKS BELOW, THANK YOUU!!

QUESTION 20. This is another exam type question. The risk inherent in tranches is different to normal assets. During the GFC it costs many investors a lot of money and during past exams some students lost a lot of marks. Please make sure that you really understand the underlying mechanics. Please do NOT RELY on memorization and shallow knowledge! Understanding will enable you to get 90% - 100% with ease.

To enable automatic feedback/marking the answers to the attached questions should be provided by filling in the blanks. However, for your own practice, I recommend taking notes on paper / pdf, including detailed calculations, balance sheets and short explanations.

Tutorial 10 Securitization.pdf

a. The risk weighted assets of BIG Bank are $___________ (no rounding!). Therefore its capital ratio is___________ (more/less) than 10%.

b. If 15 percent of Subprime Quick Money loan pool is written off, the value of BIG Bank AAA tranche holding will be $___________ and its Ba1 tranche holding will be valued at $___________. Big Bank's Equity will change to $__________. Is this still 10% of its RWA?

c. If Big Bank would have invested $20 directly into MBS (the same type of loans as Quick Money) and 15% of the underlying loans would have defaulted, the loss for Big Bank would have been exactly $___________. This would have been___________ (better / worse) than the investment in the tranches.

d. Continue with your balance sheet from b) after the losses. If Big Bank would swap all its loans against Quick Money A3 tranches, its RWA would change to $___________ (no rounding!). Check if Big Bank is now achieving its minimum CAR of 10% again.

e. If Clever Bank keeps all its loans on its balance sheet, its RWA would be exactly $___________m. However, if it does the deal with Quick Money its RWA would be $___________m. This is an___________ (advantage/disadvantage) for a capital management point of view. Did the actual riskiness of the assets change?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New Microfinance Handbook A Financial Market System Perspective

Authors: Joanna Ledgerwood, Julie Earne, Candace Nelson

1st Edition

0821389270, 978-0821389270