Question

please please type the answer instead of posting an image What impact does the repurchase plan have on M&Ms weighted-average cost of capital? Complete the

please please type the answer instead of posting an image

What impact does the repurchase plan have on M&Ms weighted-average cost of capital? Complete the table below (No Corporate Taxes). What are the debt and equity claims worth under the alternative scenarios? You may note that the present value of a perpetual cash flow stream is equal to the expected payment divided by the associated required return. Which proposal is best for investors, discuss your results in your explanation? What do you recommend that Miller do?

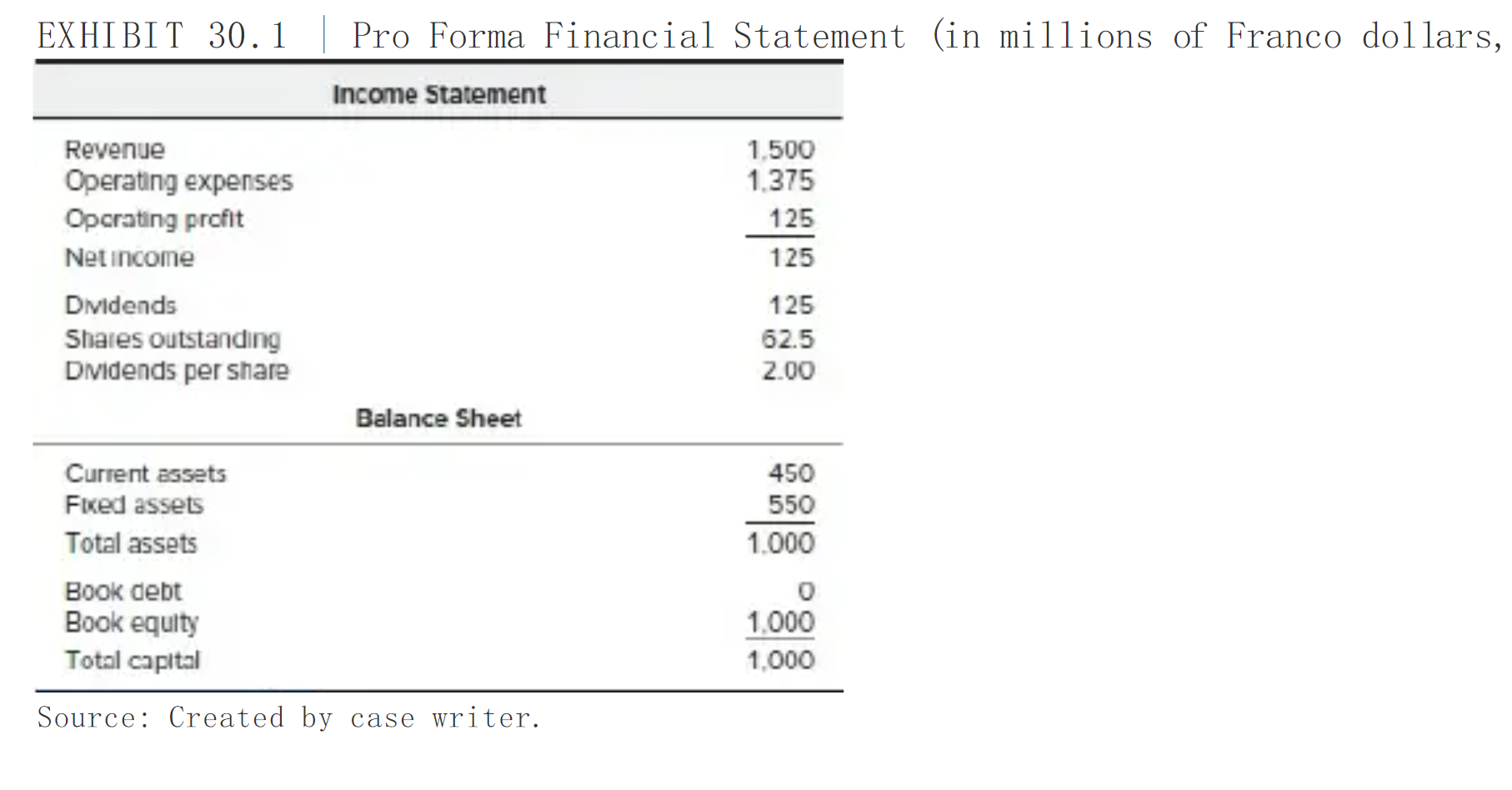

| Income Statement | Debt = 0 | Debt = 500 | |||||

| Revenue | 1500 | 1500 | |||||

| Operating expenses | 1375 | 1375 | |||||

| Operating profit | 125 | 125 | |||||

| Interest payments | 0 | ||||||

| Taxes | 0 | 0 | |||||

| Net profit | 125 | ||||||

| Dividends | 125 | ||||||

| Shares outstanding | 62.5 | ||||||

| Dividends per share | 2.00 | ||||||

| Cost of Capital | |||||||

| Cost of debt | 4.00% | 4.00% | |||||

| Beta | 0.800 | Levered Beta | |||||

| Cost of equity | CAPM | ||||||

| WACC | = D / V * Kd (1 - t) + (1 - D/V) * Ke | ||||||

| Cash flows | |||||||

| Debt holders | = Interest payments | ||||||

| Equity holders | = Dividend payments | ||||||

| Free cash flow | = Op profit | ||||||

| Value | |||||||

| Debt | = Int payments / Kd | ||||||

| Equity | = Div payments / Ke | ||||||

| Total | = Sum or FCF / WACC | ||||||

| Share price 1 | = Equity / Shares outstanding | ||||||

| Share price 2 | = DPS / Ke | ||||||

| Value of Firm | = Value of unlevered + Tax shield | ||||||

| D/E | = D / (V - D) | ||||||

| D/V | = D / V | ||||||

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Security Audit And Review Toolkit The Modern Toolkit For Security And Risk Professionals To Grow Their Business And For The Business Owners.

Authors: L Burke Files, Gamal Newry, Ibrahim Yeku

1st Edition

1674831315, 978-1674831312