Please prepare a statement of cash flows for December 31,2021

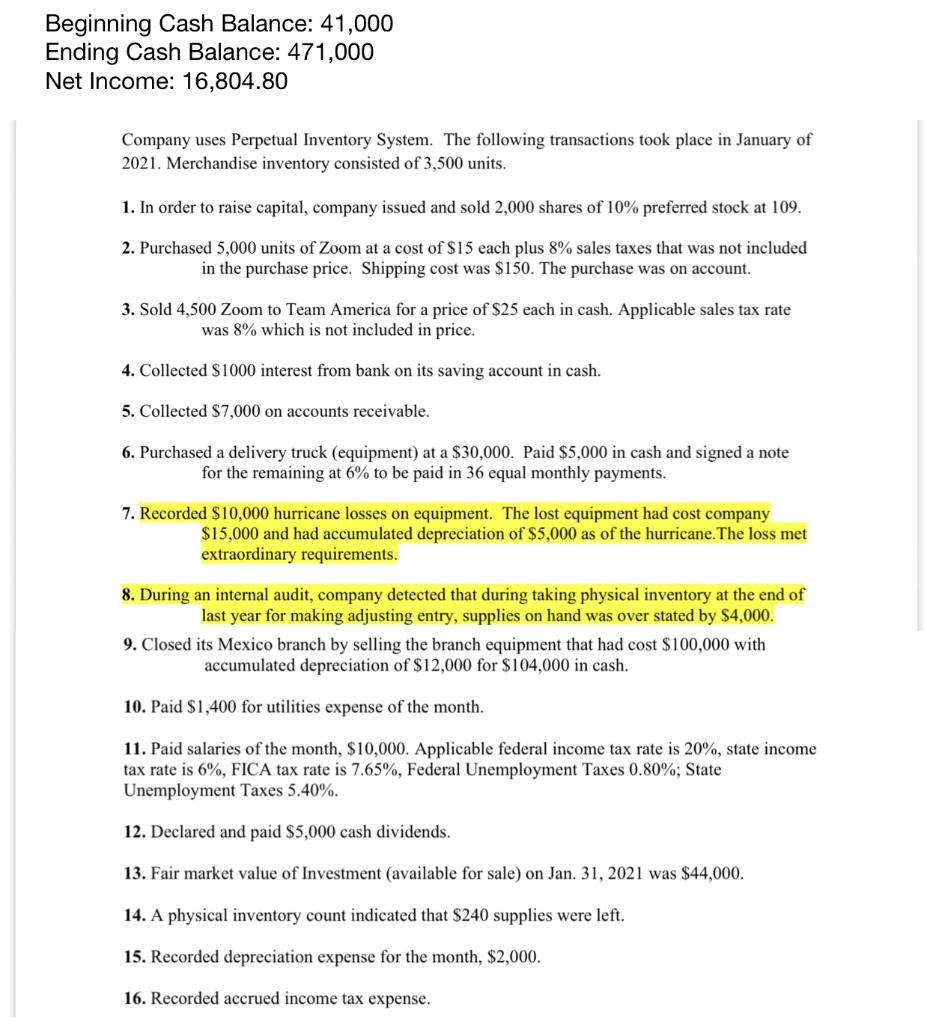

Beginning Cash Balance: 41,000 Ending Cash Balance: 471,000 Net Income: 16,804.80 Company uses Perpetual Inventory System. The following transactions took place in January of 2021. Merchandise inventory consisted of 3,500 units. 1. In order to raise capital, company issued and sold 2,000 shares of 10% preferred stock at 109. 2. Purchased 5,000 units of Zoom at a cost of $15 each plus 8% sales taxes that was not included in the purchase price. Shipping cost was $150. The purchase was on account. 3. Sold 4,500 Zoom to Team America for a price of $25 each in cash. Applicable sales tax rate was 8% which is not included in price. 4. Collected $1000 interest from bank on its saving account in cash. 5. Collected $7,000 on accounts receivable. 6. Purchased a delivery truck (equipment) at a $30,000. Paid $5,000 in cash and signed a note for the remaining at 6% to be paid in 36 equal monthly payments. 7. Recorded $10,000 hurricane losses on equipment. The lost equipment had cost company $15,000 and had accumulated depreciation of $5,000 as of the hurricane.The loss met extraordinary requirements. 8. During an internal audit, company detected that during taking physical inventory at the end of last year for making adjusting entry, supplies on hand was over stated by $4,000. 9. Closed its Mexico branch by selling the branch equipment that had cost $100,000 with accumulated depreciation of $12,000 for $104,000 in cash. 10. Paid $1,400 for utilities expense of the month. 11. Paid salaries of the month, $10,000. Applicable federal income tax rate is 20%, state income tax rate is 6%, FICA tax rate is 7.65%, Federal Unemployment Taxes 0.80%; State Unemployment Taxes 5.40%. 12. Declared and paid $5,000 cash dividends. 13. Fair market value of Investment (available for sale) Jan. 31, 2021 was $44,000. 14. A physical inventory count indicated that $240 supplies were left. 15. Recorded depreciation expense for the month, $2,000. 16. Recorded accrued income tax expense. Beginning Cash Balance: 41,000 Ending Cash Balance: 471,000 Net Income: 16,804.80 Company uses Perpetual Inventory System. The following transactions took place in January of 2021. Merchandise inventory consisted of 3,500 units. 1. In order to raise capital, company issued and sold 2,000 shares of 10% preferred stock at 109. 2. Purchased 5,000 units of Zoom at a cost of $15 each plus 8% sales taxes that was not included in the purchase price. Shipping cost was $150. The purchase was on account. 3. Sold 4,500 Zoom to Team America for a price of $25 each in cash. Applicable sales tax rate was 8% which is not included in price. 4. Collected $1000 interest from bank on its saving account in cash. 5. Collected $7,000 on accounts receivable. 6. Purchased a delivery truck (equipment) at a $30,000. Paid $5,000 in cash and signed a note for the remaining at 6% to be paid in 36 equal monthly payments. 7. Recorded $10,000 hurricane losses on equipment. The lost equipment had cost company $15,000 and had accumulated depreciation of $5,000 as of the hurricane.The loss met extraordinary requirements. 8. During an internal audit, company detected that during taking physical inventory at the end of last year for making adjusting entry, supplies on hand was over stated by $4,000. 9. Closed its Mexico branch by selling the branch equipment that had cost $100,000 with accumulated depreciation of $12,000 for $104,000 in cash. 10. Paid $1,400 for utilities expense of the month. 11. Paid salaries of the month, $10,000. Applicable federal income tax rate is 20%, state income tax rate is 6%, FICA tax rate is 7.65%, Federal Unemployment Taxes 0.80%; State Unemployment Taxes 5.40%. 12. Declared and paid $5,000 cash dividends. 13. Fair market value of Investment (available for sale) Jan. 31, 2021 was $44,000. 14. A physical inventory count indicated that $240 supplies were left. 15. Recorded depreciation expense for the month, $2,000. 16. Recorded accrued income tax expense