please prepare journal entries

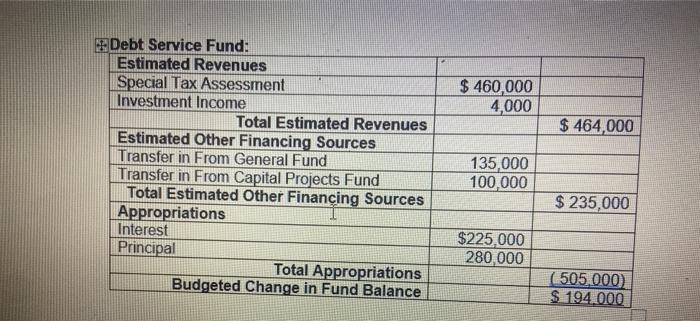

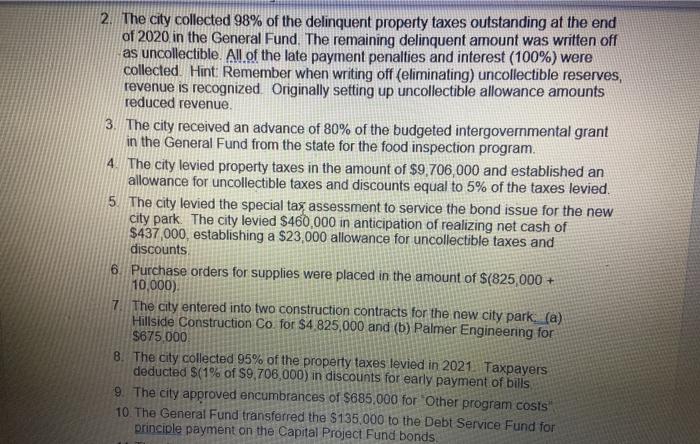

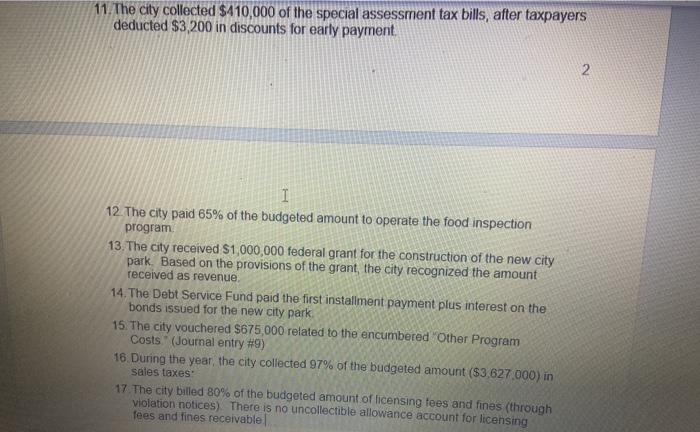

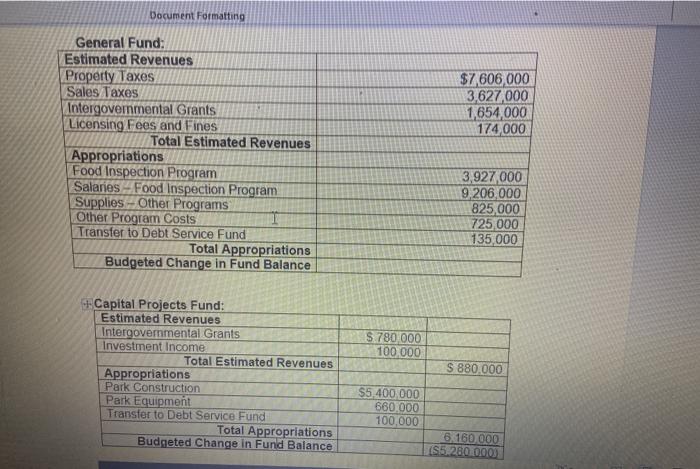

Document Formatting $7 606,000 3,627,000 1,654,000 174,000 General Fund: Estimated Revenues Property Taxes Sales Taxes Intergovemmental Grants Licensing Fees and Fines Total Estimated Revenues Appropriations Food Inspection Program Salaries-Food Inspection Program Supplies - Other Programs Other Program Costs Transfer to Debt Service Fund Total Appropriations Budgeted Change in Fund Balance 3,927,000 9,206,000 825,000 725 000 135,000 $ 780,000 100.000 Capital Projects Fund: Estimated Revenues Intergovernmental Grants Investment Income Total Estimated Revenues Appropriations Park Construction Park Equipment Transfer to Debt Service Fund Total Appropriations Budgeted Change in Fund Balance $ 880,000 $5.400.000 660.000 100.000 6.160 000 185.280.000 $ 460,000 4,000 $ 464,000 Debt Service Fund: Estimated Revenues Special Tax Assessment Investment Income Total Estimated Revenues Estimated Other Financing Sources Transfer in From General Fund Transfer in From Capital Projects Fund Total Estimated Other Financing Sources Appropriations Interest Principal Total Appropriations Budgeted Change in Fund Balance 135,000 100,000 $ 235,000 $225,000 280,000 ( 505.000) $ 194.000 2. The city collected 98% of the delinquent property taxes outstanding at the end of 2020 in the General Fund. The remaining delinquent amount was written off as uncollectible. All of the late payment penalties and interest (100%) were collected. Hint: Remember when writing off (eliminating) uncollectible reserves, revenue is recognized Originally setting up uncollectible allowance amounts reduced revenue. 3. The city received an advance of 80% of the budgeted intergovernmental grant in the General Fund from the state for the food inspection program. 4. The city levied property taxes in the amount of $9,706,000 and established an allowance for uncollectible taxes and discounts equal to 5% of the taxes levied. 5. The city levied the special tas assessment to service the bond issue for the new city park. The city levied $460,000 in anticipation of realizing net cash of $437,000, establishing a $23,000 allowance for uncollectible taxes and discounts 6. Purchase orders for supplies were placed in the amount of $(825,000 + 10.000) 7 The city entered into two construction contracts for the new city park. (a) Hillside Construction Co for $4 825,000 and (b) Palmer Engineering for $675 000 8. The city collected 95% of the property taxes levied in 2021. Taxpayers deducted $(1% of S9,706,000) in discounts for early payment of bills 9. The city approved encumbrances of $685,000 for Other program costs 10. The General Fund transferred the $135,000 to the Debt Service Fund for principle payment on the Capital Project Fund bonds. 11. The city collected $410,000 of the special assessment tax bills, after taxpayers deducted $3,200 in discounts for early payment 2. I 12. The city paid 65% of the budgeted amount to operate the food inspection program 13. The city received $1,000,000 federal grant for the construction of the new city park. Based on the provisions of the grant, the city recognized the amount received as revenue. 14. The Debt Service Fund paid the first installment payment plus interest on the bonds issued for the new city park 15. The city vouchered $675,000 related to the encumbered Other Program Costs." (Journal entry #9) 16. During the year, the city collected 97% of the budgeted amount ($3,627.000) in sales taxes 17 The city billed 80% of the budgeted amount of licensing tees and fines (through violation notices). There is no uncollectible allowance account for licensing fees and fines receivable Document Formatting $7 606,000 3,627,000 1,654,000 174,000 General Fund: Estimated Revenues Property Taxes Sales Taxes Intergovemmental Grants Licensing Fees and Fines Total Estimated Revenues Appropriations Food Inspection Program Salaries-Food Inspection Program Supplies - Other Programs Other Program Costs Transfer to Debt Service Fund Total Appropriations Budgeted Change in Fund Balance 3,927,000 9,206,000 825,000 725 000 135,000 $ 780,000 100.000 Capital Projects Fund: Estimated Revenues Intergovernmental Grants Investment Income Total Estimated Revenues Appropriations Park Construction Park Equipment Transfer to Debt Service Fund Total Appropriations Budgeted Change in Fund Balance $ 880,000 $5.400.000 660.000 100.000 6.160 000 185.280.000 $ 460,000 4,000 $ 464,000 Debt Service Fund: Estimated Revenues Special Tax Assessment Investment Income Total Estimated Revenues Estimated Other Financing Sources Transfer in From General Fund Transfer in From Capital Projects Fund Total Estimated Other Financing Sources Appropriations Interest Principal Total Appropriations Budgeted Change in Fund Balance 135,000 100,000 $ 235,000 $225,000 280,000 ( 505.000) $ 194.000 2. The city collected 98% of the delinquent property taxes outstanding at the end of 2020 in the General Fund. The remaining delinquent amount was written off as uncollectible. All of the late payment penalties and interest (100%) were collected. Hint: Remember when writing off (eliminating) uncollectible reserves, revenue is recognized Originally setting up uncollectible allowance amounts reduced revenue. 3. The city received an advance of 80% of the budgeted intergovernmental grant in the General Fund from the state for the food inspection program. 4. The city levied property taxes in the amount of $9,706,000 and established an allowance for uncollectible taxes and discounts equal to 5% of the taxes levied. 5. The city levied the special tas assessment to service the bond issue for the new city park. The city levied $460,000 in anticipation of realizing net cash of $437,000, establishing a $23,000 allowance for uncollectible taxes and discounts 6. Purchase orders for supplies were placed in the amount of $(825,000 + 10.000) 7 The city entered into two construction contracts for the new city park. (a) Hillside Construction Co for $4 825,000 and (b) Palmer Engineering for $675 000 8. The city collected 95% of the property taxes levied in 2021. Taxpayers deducted $(1% of S9,706,000) in discounts for early payment of bills 9. The city approved encumbrances of $685,000 for Other program costs 10. The General Fund transferred the $135,000 to the Debt Service Fund for principle payment on the Capital Project Fund bonds. 11. The city collected $410,000 of the special assessment tax bills, after taxpayers deducted $3,200 in discounts for early payment 2. I 12. The city paid 65% of the budgeted amount to operate the food inspection program 13. The city received $1,000,000 federal grant for the construction of the new city park. Based on the provisions of the grant, the city recognized the amount received as revenue. 14. The Debt Service Fund paid the first installment payment plus interest on the bonds issued for the new city park 15. The city vouchered $675,000 related to the encumbered Other Program Costs." (Journal entry #9) 16. During the year, the city collected 97% of the budgeted amount ($3,627.000) in sales taxes 17 The city billed 80% of the budgeted amount of licensing tees and fines (through violation notices). There is no uncollectible allowance account for licensing fees and fines receivable