Please provide a summary and reaction to the article. The summary should be 250 words and reaction should be approximately 150 words and should describe the major points of the article, and the reaction should demonstrate your interpretation of the article and how you can apply that knowledge.

Article is - Organization of responsibility accounting of city electric transport enterprises activity | Nykyforak | Eastern-European Journal of Enterprise Technologies (uran.ua)

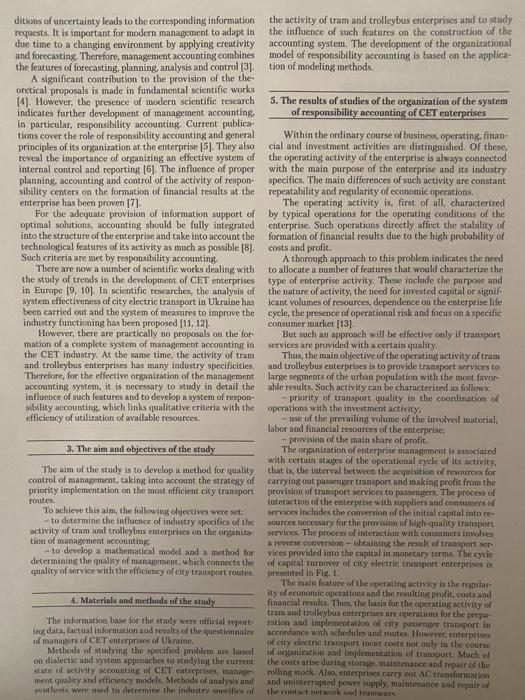

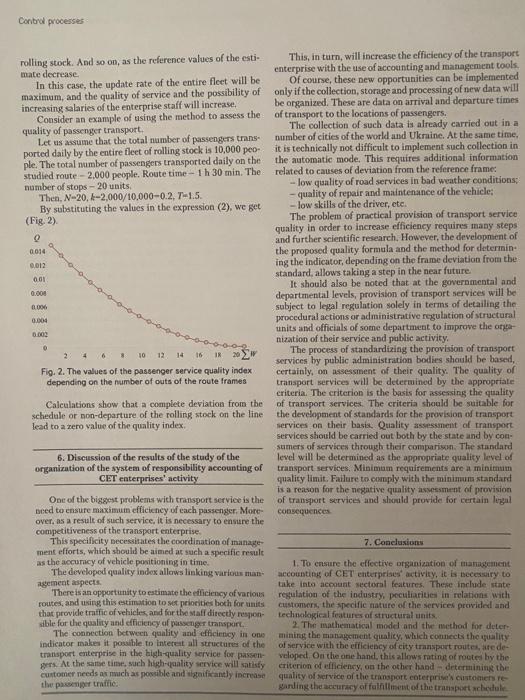

D- .7. 1, DOI: 10.15587720-061.2018. 12617 - . - . - . - : - , , - , - - , - . - - , - : , , - , ORGANIZATION OF RESPONSIBILITY ACCOUNTING OF CITY ELECTRIC TRANSPORT ENTERPRISES' ACTIVITY 1. Nykyforak PhD Department of Accounting. Analysis and Audit Yuriy Fedkovych Chernivtsi National University Kotsyubynsky str., 2, Chernivtsi, Ukraine, 58012 E-mail: i.nykyforak@chnu.edu.ua N. Du hanets PhD, Associate Professor Department of Accounting and Taxation State Agrarian and Engineering University of Podilya Shevchenko str., 13, Kamianets-Podilsky, Khmelnitsky region, Ukraine, 32300 E-mail: ptashka77774@gmail.com Ye. Kobrusleva PhD, Associate Professor Department of Administrative and Criminal Law Dniprovsky National University Gagarin ave., 72, Dnipro, Ukraine, 490 10 E-mail: kobruseva22@gmail.com - 1. Introduction information on service quality violations is generated under the condition of organization of responsibility accounting In such circumstances, information about resources consumed and results achieved by separate units of the enterprise is generated. Reasonable grounds for motivating employees to achieve specific goals are also provided. However, the profit and cost center accounting in different industries is carried out deperuling on the production technology and organizational structure of the enterprise. The organization of responsibility accounting creates the opportunities of proper information support for making optimal management decisions The important role of the land city electric transport (CET) is confirmed by the experience of the functioning of advanced transport systems around the world. The need for its development in cities is justified by scientists and experts in the field of organization of city transport systems. The infrastructure nature of transport services lies in the acces wibility, cost-effectiveness and environmental friendliness At present, enterprises of city clectric transport in Ukraine are inprofitable, so the industry is declining Low ever, latest scientific studies indicate the need for the de- velopment of electric transport, which will allow achieving significant environmental and social efects[i]. The CET sector Deeds radical reform. It is necessary to increase the efficiency of the management system by direct- ing efforts to overcome the unprofitability of tram and trol leybus enterprises. This is primarily related to improving the quality of service. Therefore, optimization of the formation of financial results of activity are the priorities of manage meat of tram and trolleybus enterprises Effective management in modern conditions involves the use of qualitatively new information generated in the man werment acting witem. The macrurate and timely 2. Literature review and problem statement The scientific problem of improving the system onuna ment accounting of the enterprise activity is under reviewly many researchers. The main trend of management accounting in the statement about changing the current role of co- tints towards active participation in decision-making on management of economic activity of the enterprise 12 At the moment, management accounting acquires clear steel frature. The wine community of business in com ditions of uncertainty leads to the corresponding information the activity of tram and trolleybus enterprises and to study requests. It is important for modern management to adapt in the influence of such features on the construction of the due time to a changing environment by applying creativity accounting system. The development of the organizational and forecasting Therefore, management accounting combines model of responsibility accounting is based on the applica- the features of forecasting planning, analysis and control (3) tion of modeling methods. A significant contribution to the prowision of the the oretical proposals is made in fundamental scientific works 14). However, the presence of modern scientific research 5. The results of studies of the organization of the system indicates further development of management accounting, of responsibility accounting of CET enterprises in particular, responsibility accounting, Current publica tions cover the role of responsibility accounting and general Within the ordinary course of business, operating, finan principles of its organization at the enterprise (5). They also cial and investment activities are distinguished. Of these, reveal the importance of organizing an effective system of the operating activity of the enterprise is always connected internal control and reporting (6). The influence of proper with the main purpose of the enterprise and its industry planning, accounting and control of the activity of respon- specifics. The main differences of such activity are constant sibility centers on the formation of financial results at the repeatability and regularity of economic operations, enterprise has been proven 171. The operating activity is, first of all, characterized For the adequate provision of information support of by typical operations for the operating conditions of the optimal solutions, accounting should be fully integrated enterprise. Such operations directly affect the stability of into the structure of the enterprise and take into account the formation of financial results due to the high probability of technological features of its activity as much as possible [8]. costs and profit. Such criteria are met by responsibility accounting A thorough approach to this problem indicates the need There are now a number of scientific works dealing with to allocate a number of features that would characterize the the study of trends in the development of CET enterprises type of enterprise activity. These include the purpose and in Europe [9, 10). In scientific researches, the analysis of the nature of activity, the need for invested capital or signif system effectiveness of city electric transport in Ukraine has Icant volumes of resources, dependence on the enterprise life been carried out and the system of measures to improve the cycle, the presence of operational risk and focus on a specific industry functioning has been proposed (11, 12). consumer market [13] However, there are practically no proposals on the for But such an approach will be effective only if transport mation of a complete system of management accounting in services are provided with a certain quality the CET industry. At the same time, the activity of tram Thus, the main objective of the operating activity of tram and trolleybus enterprises has many industry specificities. and trolleybus enterprises is to provide transport services to Therefore, for the effective organization of the management large segments of the urban population with the most favor accounting system, it is necessary to study in detail the able results. Such activity can be characterized as follows influence of such features and to develop a system of respon- priority of transport quality in the coordination of sibility accounting, which links qualitative criteria with the operations with the investment activity efficiency of utilization of available resources. - use of the prevailing volume of the involved material, labor and financial resources of the enterprise provision of the main share of profit. 3. The aim and objectives of the study The organization of enterprise management is associated with certain stages of the operational cycle of its activity, The aim of the study is to develop a method for quality that is the interval between the acquisition of resources for control of management, taking into account the strategy of carrying out passenger transport and making profit from the priority implementation on the most efficient city transport provision of transport services to passengers. The process of routes Interaction of the enterprise with suppliers and consumers of To achieve this aim, the following objectives were set: services includes the conversion of the initial capital into re- - to determine the influence of industry specifics of the sources necessary for the provision of high-quality transport activity of tram and trolleybus enterprises on the organiza services. The process of interaction with consumers involves tion of management accounting a reverse conversion - obtaining the result of transport ser - to develop a mathematical model and a method for vices provided into the capital in monetary terms. The cycle determining the quality of management, which connects the of capital turnover of city electric transport enterprises is quality of service with the efficiency of city transport routes presented in Fig. 1 The main feature of the uperating activity is the regular ity of economie operations and the resulting profit, costs and 4. Materials and methods of the study financial results. Thus, the basis for the operating activity of tram and trolleybus enterprises are operations for the prepa The information base for the study were official reports ration and implementation of city passenger transport in ing data, factual information and results of the questionnaire accordance with schedules and routes. However, enterprises of managers of CET enterprises of Ukraine. ot clectric transport incur costs not only in the course Method of staying the specified problem are based of organization and implementation of transport. Much of on dialectic and system approaches to studying the current the costs arise during store maintenance and repair of the state of activity accounting of CET enterprises, manage rolling stock. Also, enterprises carry out AC transformation ment quality and efficiency models. Methods of analysis and and uninterrupted power supply, maintenance and repair of wynthesis were to determine the indstry secifics of the contact network and tramwav cient information about quality and efficiency, Capital Capital The information behavior of managers should combine control, adaptation, forecasting and Conversion of creativity based on the diversity of information capital into resources (17). In this regard, the main objects resources of management are profit, costs and financial results. At present, information on these objects Resources Conversion of is formed within the integrated accounting sys provided tem at the enterprises of city electric transport, transport However, such information is not enough to services Conversion of ensure the high-quality implementation of man- resources into the agement functions. The process of effective ac- passenger counting of activity should be organized so that transport process on its basis, it would be possible to take timely and scientifically sound management decisions Process stages Passenger transport Transport services "One of the major principles when choosing an option of the organization of activity accounting and management is obvious the compliance of the accounting system with the objectives of management" [18). In each case, the management decision must Fig. 1. Processes of the operating activity of city electric transport be, above all, targeted. That is, the management enterprises influence should be directed to the definition of financial result and efficiency of activity not The operating activity consists of a number of successive only of the enterprise as a whole, but of each structural unit stages: supply, preparation for transport, provision and im- separately. This situation leads to the growth of the infor plementation of transport services. At the enterprises of city mation role of responsibility accounting, which will allow electric transport, the processes of production, sale and con- determining general and individual results. Possibilities of sumption of products are combined, while in the production effective management depend on the extent of perception sphere the specified processes are separated from each other and interpretation of information formed in the accounting in space and time. Transport does not generate wealth that system by the management staff" (19) can be accumulated or reserved. CET companies provide Responsibility accounting provides direct and feedback passenger transport services Services cannot be separated communication at different levels of management. The from the transport process, resulting in an inextricable link purpose of such accounting, above all, is the formation of a between the provision and consumption of transport ser new vision of production responsibilities of employees and vices. This puts transport companies in direct dependence the organization of conscious self-control. Employees will on fluctuations in demand for transport and leads to uneven feel responsible for the quality of the work performed and production have confidence that the final achievements will not remain In addition, CET companies have significant peculiari- unnoticed by the management. After all, the skillful se of ties in relations with customers. In accordance with the law, psychological and economic leverage will motivate employ tram and trolleybus enterprises are obliged to provide trans- ces to achieve the best result port services to certain categories of passengers at a reduced Therefore, responsibility accounting is a key element of cost [14]. According to the report of the CET Corporation Organization of management accounting, which combines the number of passengers entitled to reduced transport fares control, analytical and motivational functions. Such ac in 2017 reached 65.84% [15]. The procedure of forming counting system is not new, it is described in detail in the transport fares is also legally established, focusing primar works of both foreign and domestic scholars. Thus, "respon ily on the criterion of real solvency of the population (16) sibility accounting is a system that allows you to evaluate Therefore, part of the costs of the main activity are covered plans and action of sich responsibility center [4). The at the expense of badgetary financing. The amount of such organizational structure of the enterprise resembles a pyra financing should correspond to the amount of profit lost mid, in which each manager is assigned to the responsibility due to the transport of those categories of passengers who center 118]. This principle of accounting allows determining enjoy reduced public transport fares. In addition, the funds levels of profit and costs by the primary places of origin in of CET enterprises should be recognized as a form of profit structural units. There are different approaches regarding the amount of which depends on the quantity and quality of the structure and classification methods of responsibility transport services provided to those categories of the popu centers Cost, profit and investment centers are commonly lation paying reduced fares distinguished (20) Based on the above peculiarities of management of city However, it is necessary to distinguish between the con electric transport enterprises, the following definition of the cepts of pufit or cost ceuter and responsibility center i operating activity can be proceed it is a set of operations in well-known that the profit or cost center is a type of te related to the preparation and direct implementation of sponibility centers. Often, scientists detine both the profit passenger transport by the rolling stock in accordance with or cost center, and the responsibility center is a set of established routes and schedules the enterprise activity that responsability centens must ha To ensure the proper management of the operating personal responsibility of the head for activity indicators tivity of CET enteri Winerary to an which can influeel and control Enter turopean Journal of Enterprise Technoge is RP- At the same time, there are differences regarding the However, the problem is the inconsistency of service, specificity of distribution of profit and costs among responsi with respect to the priorities of service of technical facilities bility centers. Thus, there is a statement that cost centers and of different routes and the quality of their work with the responsibility centers should be considered as two indepen-quality of service of transport passengers. dent objects of accounting and control of production costs, At present, the role of city electric transport begins to which are determined by the place in the enterprise structure, grow. This trend is most noticeable in large cities, where economic characteristics and social content (21). That is the efficiency of using personal transport is constantly de responsibility centers, first of all, are associated with cost creasing due to the growing shortage of parking places and management, while cost centers - only with the calculation frequent congestion of production costs Today, the main criterion for deciding on the type of There is also a definition of the cost center as cost vehicle is reliability and compliance with the declared sched- grouping, which allows combining cost centers with the ule. In such a situation, a transport enterprise serving a pas. responsibility of managers who head certain departments senger traffic of more than 2 thousand pass/his guaranteed in one accounting process. In this case, cost center meats a to become profitable [22]. separate object of analytical accounting for the purpose of As a result, the technology for improving the efficiency monitoring control and management of city public transport should be based on the method that Along with cost centers, most researchers distinguish allows combining the interests of both service staff and profit (revenue) centers that have certain characteristics passengers This is a mandatory responsibility of the managemeat of a The proposed method relies on the use of the basic separate structural unit of the enterprise for the formation of structure of the estimate [23, 24), which was tested for the profit (revenue) and the lack of control over costs. possibility to be applied as a criterion of efficiency 125-27 The starting point for constructing the responsibility accounting system is the organizational structure of the (P-R) enterprise. First of all, it is proposed to take into account the technological structure of the enterprise and then allocate its horizontal and vertical sections where is the expert estimate of the input product of the So, in different industries, profit and cost center ac operation: Pis the expert estimate of the output product of counting should be carried out in different ways, because it the operation is the time of the operation depends on the technology and organizational structure of The proposed method is based on the fact that the indi: the enterprise. The main focus should be on the distribution cator of resource efficiency is transformed into a standard of of profit and costs precisely among responsibility centers passenger service quality whose managers can directly influence the process of forma For this, as the expert estimate of the input product of tion of indicators and bear personal responsibility the operation, we take the volume of served passengersion The main operating activity is performed by the depot the segment of the studied routeR-N traffic service, which provides transport services to passen Let us determine the coefficient of the added value gers. This service organizes passenger transport on routes of transport service as the ratio of the average number of and monitors compliance with the traffic regularity on the passengers transported daily to the number of lines and the live according to the schedule. The services of the main unit average number of passengers served by transport lines). can be characterized as follow Then the expert estimate of the output product of the the cost of services is directly included in transport fares transport operation can be determined from the expression direct consumers of services are passenger PEN However, enterprises of city clectric transport incur Let us introduce the concept of a frame as an interval of costs not only in the process of organization and implemen time from the transport arrival to a stop until the arrival at tation of transport according to the schedule. Auxilury the next stop. units do not directly serve passengers. The activity of such Then out of frame at a fixed time interval will change the units is aimed at achieving the main objective. They should coefficient W of the penalty function F contribute to the functions of the main unit. To perform such technological functions, the following production and F-(-1) operating units are organized - rolling stock department of the depot (repair shops), When out of one frame, the numerical value of the coef which is intended for storage, maintenance and repair of ficient of the penalty function takes it valor. This value the flees, that is responsible for putting technically sound is increased by one at the next out of fun within the route. vehicles on the line Them for the service quality indicator, we will get - energy management department (traction power station and emergency dispatch service), which provides uninterrupe (NA-(4-1) W-N) (2) ed power supply to the line through AC transformation - railroad management department, which perform the functions of maintenance and current repair of tramways The value of the eliciency index with tero penalty fune and railways tion index is a standard for the transporter and the service The peculiarities of services provided by auxiliary units staff of the line include On the other hand, the value of the state in - the cost of services is indirectly included in transport idicates the most profitable route for the transport enterprise fames For a route with a maximum reference Q. It is advisable - terms and cons of tanut the most exteriene driver and the most in-to-date Control processes 0.014 0.012 0.01 0 2 16 IR rolling stock. And so on, as the reference values of the esti- This, in turn, will increase the efficiency of the transport mate decrease enterprise with the use of accounting and management tools. In this case, the update rate of the entire fleet will be Of course, these new opportunities can be implemented maximum, and the quality of service and the possibility of only if the collection, storage and processing of new data will increasing salaries of the enterprise staff will increase be organized. These are data on arrival and departure times Consider an example of using the method to assess the of transport to the locations of passengers. quality of passenger transport. The collection of such data is already carried out in a Let us assume that the total number of passengers trans- number of cities of the world and Ukraine. At the same time, ported daily by the entire fleet of rolling stock is 10,000 peo it is technically not difficult to implement such collection in ple. The total number of passengers transported daily on the the automatic mode. This requires additional information studied route - 2,000 people. Route time - 1 h 30 min. The related to causes of deviation from the reference frame: number of stops - 20 units - low quality of road services in bad weather conditions: Then, N-20, 1-2,000/10000-0.2.7-1.5. - quality of repair and maintenance of the vehicle: By substituting the values in the expression (2), we get - low skills of the driver, etc. (Fig. 2). The problem of practical provision of transport service quality in order to increase efficiency requires many steps and further scientific research. However, the development of the proposed quality formula and the method for determin ing the indicator, depending on the frame deviation from the standard, allows taking a step in the near future. It should also be noted that at the governmental and 0.000 departmental levels, provision of transport services will be 0.006 subject to legal regulation solely in terms of detailing the 0.004 procedural actions or administrative regulation of structural units and officials of some department to improve the orga nization of their service and public activity 10 12 The process of standardizing the provision of transport services by public administration bodies should be based, Fig. 2. The values of the passenger service quality index certainly, on assessment of their quality. The quality of depending on the number of outs of the route frames transport services will be determined by the appropriate criteria. The criterion is the basis for assessing the quality Calculations show that a complete deviation from the of transport services. The criteria should be suitable for schedule or non-departure of the rolling stock on the line the development of standards for the provision of transport lead to a zero value of the quality index services on their basis. Quality assessment of transport services should be carried out both by the state and by con sumers of services through their comparism. The standard 6. Discussion of the results of the study of the level will be determined as the appropriate quality level of organization of the system of responsibility accounting of transport services. Minimum requirements are a minimum CET enterprises' activity quality limit. Failure to comply with the minimum standard is a reason for the negative quality assessment of provision One of the biggest problems with transport service is the of transport services and should provide for certain legal need to ensure maximum efficiency of each passenger. More over, as a result of such service, it is necessary to ensure the consequences competitiveness of the transport enterprise. This specificity necessitates the coordination of manage 7. Conclusions ment efforts, which should be aimed at such a specific result as the accuracy of vehicle positioning in time. The developed quality index allows linking various man 1. To ensure the effective organization of management accounting of CET enterprises activity, it is necessary to agement aspects There is an opportunity to estimate the efficiency of various take into account sectoral features. These include state regulation of the industry, peculiarities in relations with routes, and using this estimation to set pelities both for units that provide traffic of vehicles and for the staff directly respon customers, the specific nature of the services provided and able for the quality and efficiency of passenger transport technological features of structural units 2. The mathematical model and the method for deter The connection between quality and efficiency in one indicator akes it possible to interest all structures of the mining the management quality, which connects the quality of service with the efficiency of city transport routes, are de- transport enterprise in the high-quality service for passen veloped. On the one hand, this allows rating of rooted by the gers. At the same time, such high-quality service will satisfy customer needs as much as possible and significantly increase quality of service of the transport enterprises customers te criterion of efficiency, on the other hand determining the the passenger traffic Barling the accuracy of fulfillment of the transport chechule