Answered step by step

Verified Expert Solution

Question

1 Approved Answer

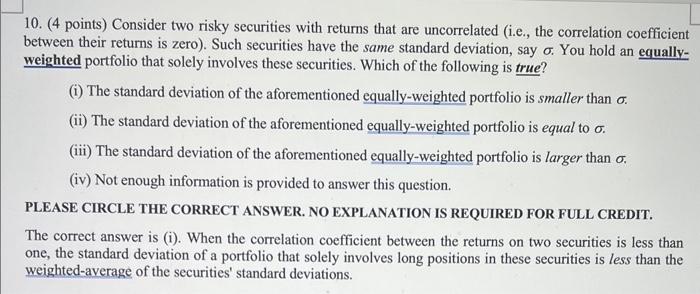

Please provide me with a concise explanation of why (i) is correct. 10. (4 points) Consider two risky securities with returns that are uncorrelated (i.e.,

Please provide me with a concise explanation of why (i) is correct.

10. (4 points) Consider two risky securities with returns that are uncorrelated (i.e., the correlation coefficient between their returns is zero). Such securities have the same standard deviation, say . You hold an equallyweighted portfolio that solely involves these securities. Which of the following is true? (i) The standard deviation of the aforementioned equally-weighted portfolio is smaller than . (ii) The standard deviation of the aforementioned equally-weighted portfolio is equal to . (iii) The standard deviation of the aforementioned equally-weighted portfolio is larger than . (iv) Not enough information is provided to answer this question. PLEASE CIRCLE THE CORRECT ANSWER. NO EXPLANATION IS REQUIRED FOR FULL CREDIT. The correct answer is (i). When the correlation coefficient between the returns on two securities is less than one, the standard deviation of a portfolio that solely involves long positions in these securities is less than the weighted-average of the securities' standard deviations Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis For Financial Management

Authors: Robert Higgins, Jennifer Koski, Todd Mitton

13th Edition

1260772365, 978-1260772364