Answered step by step

Verified Expert Solution

Question

1 Approved Answer

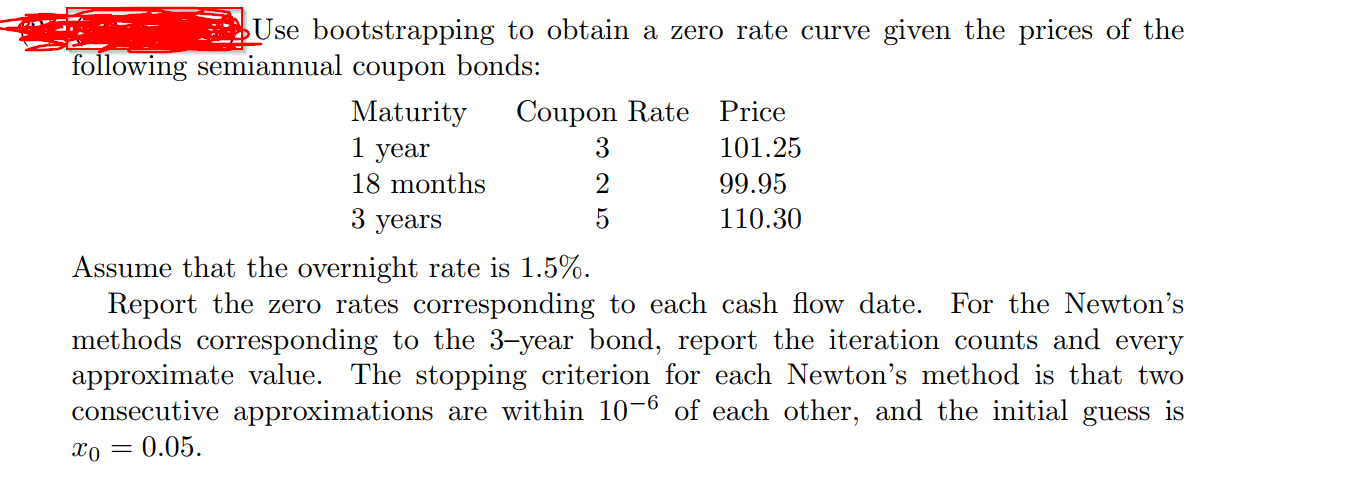

Please provide python code. Use bootstrapping to obtain a zero rate curve given the prices of the following semiannual coupon bonds: Assume that the overnight

Please provide python code.

Use bootstrapping to obtain a zero rate curve given the prices of the

following semiannual coupon bonds:

Assume that the overnight rate is

Report the zero rates corresponding to each cash flow date. For the Newton's

methods corresponding to the year bond, report the iteration counts and every

approximate value. The stopping criterion for each Newton's method is that two

consecutive approximations are within of each other, and the initial guess is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Spatio Temporal Database Management International Workshop Stdbm 99 Edinburgh Scotland September 10 11 1999 Proceedings Lncs 1678

Authors: Michael H. Bohlen ,Christian S. Jensen ,Michel O. Scholl

1999th Edition

3540664017, 978-3540664017