Please Provide step by step work

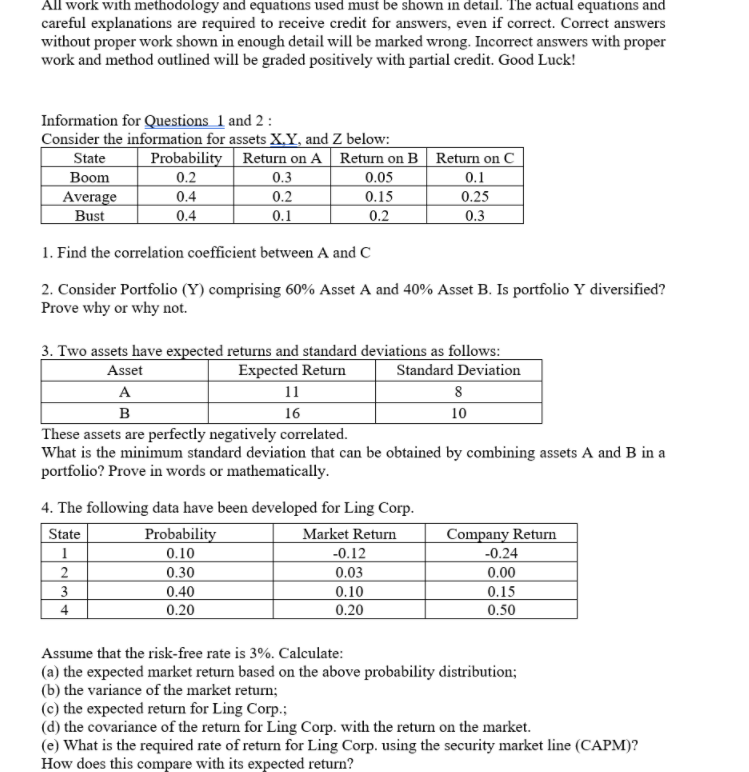

All work with methodology and equations used must be shown in detail. The actual equations and careful explanations are required to receive credit for answers, even if correct. Correct answers without proper work shown in enough detail will be marked wrong. Incorrect answers with proper work and method outlined will be graded positively with partial credit. Good Luck! Information for Questions 1 and 2: Consider the information for assets X,Y, and Z below: State Probability Return on A Return on B Return on C Boom 0.2 0.3 0.05 0.1 Average 0.4 0.2 0.15 0.25 Bust 0.4 0.1 0.2 0.3 1. Find the correlation coefficient between A and C 2. Consider Portfolio (Y) comprising 60% Asset A and 40% Asset B. Is portfolio Y diversified? Prove why or why not. 3. Two assets have expected returns and standard deviations as follows: Asset Expected Return Standard Deviation A 11 8 B 16 10 These assets are perfectly negatively correlated. What is the minimum standard deviation that can be obtained by combining assets A and B in a portfolio? Prove in words or mathematically. 4. The following data have been developed for Ling Corp. State Probability Market Return Company Return 1 0.10 -0.24 2 0.30 0.03 0.00 3 0.40 0.10 0.15 0.20 0.20 0.50 -0.12 4 Assume that the risk-free rate is 3%. Calculate: (a) the expected market return based on the above probability distribution; (b) the variance of the market return; (c) the expected return for Ling Corp.; (d) the covariance of the return for Ling Corp. with the return on the market. (e) What is the required rate of return for Ling Corp. using the security market line (CAPM)? How does this compare with its expected return? All work with methodology and equations used must be shown in detail. The actual equations and careful explanations are required to receive credit for answers, even if correct. Correct answers without proper work shown in enough detail will be marked wrong. Incorrect answers with proper work and method outlined will be graded positively with partial credit. Good Luck! Information for Questions 1 and 2: Consider the information for assets X,Y, and Z below: State Probability Return on A Return on B Return on C Boom 0.2 0.3 0.05 0.1 Average 0.4 0.2 0.15 0.25 Bust 0.4 0.1 0.2 0.3 1. Find the correlation coefficient between A and C 2. Consider Portfolio (Y) comprising 60% Asset A and 40% Asset B. Is portfolio Y diversified? Prove why or why not. 3. Two assets have expected returns and standard deviations as follows: Asset Expected Return Standard Deviation A 11 8 B 16 10 These assets are perfectly negatively correlated. What is the minimum standard deviation that can be obtained by combining assets A and B in a portfolio? Prove in words or mathematically. 4. The following data have been developed for Ling Corp. State Probability Market Return Company Return 1 0.10 -0.24 2 0.30 0.03 0.00 3 0.40 0.10 0.15 0.20 0.20 0.50 -0.12 4 Assume that the risk-free rate is 3%. Calculate: (a) the expected market return based on the above probability distribution; (b) the variance of the market return; (c) the expected return for Ling Corp.; (d) the covariance of the return for Ling Corp. with the return on the market. (e) What is the required rate of return for Ling Corp. using the security market line (CAPM)? How does this compare with its expected return