Answered step by step

Verified Expert Solution

Question

1 Approved Answer

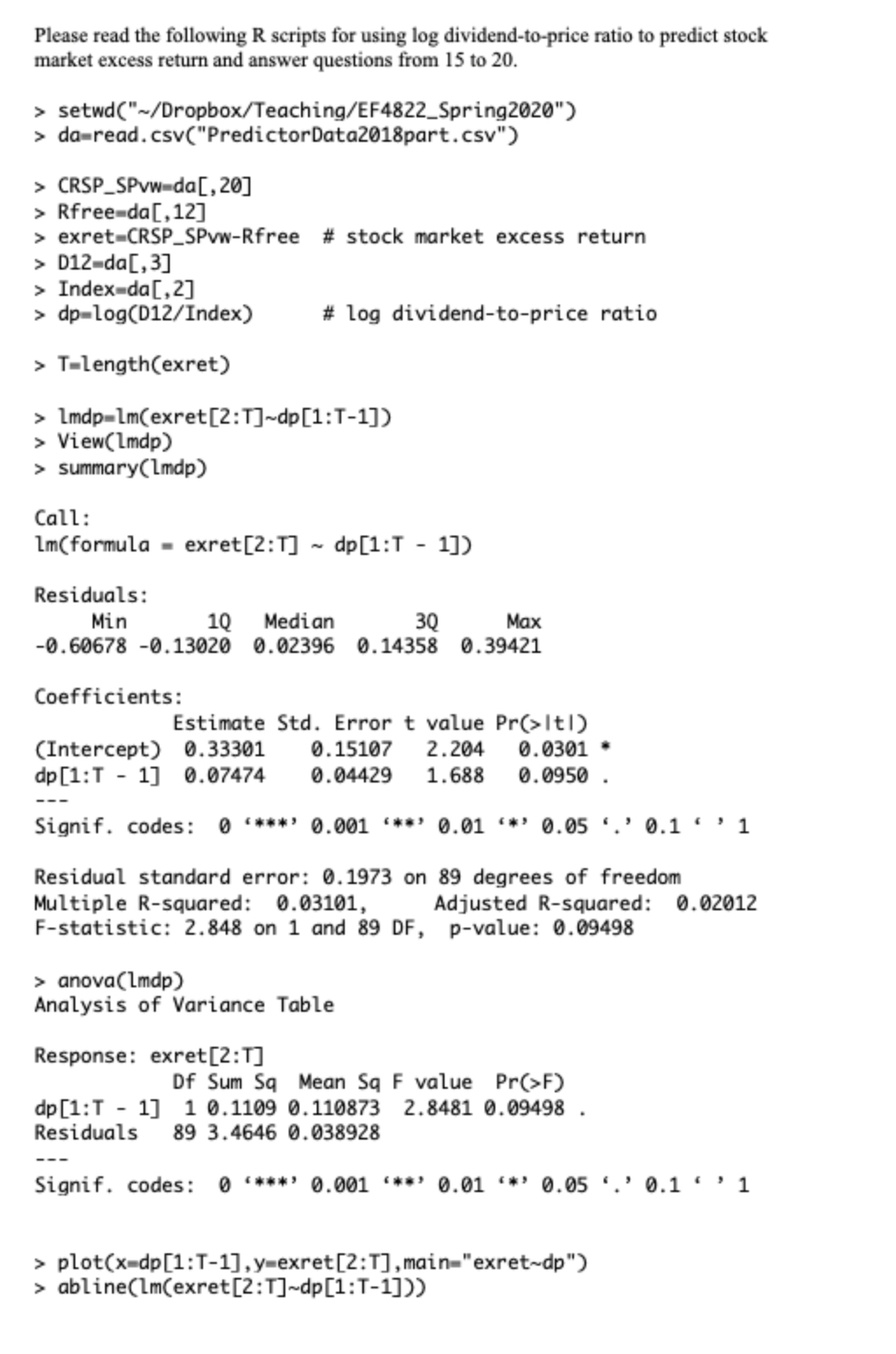

Please read the following R scripts for using log dividend-to-price ratio to predict stock market excess return and answer questions from 15 to 20.

Please read the following R scripts for using log dividend-to-price ratio to predict stock market excess return and answer questions from 15 to 20. > setwd("~/Dropbox/Teaching/EF4822_Spring2020") > da read.csv("PredictorData2018part.csv") > CRSP_SPvw-da[, 20] > Rfree-da[12] > exret CRSP SPvw-Rfree # stock market excess return > D12-da[,3] > Index-da[,2] > dp log(D12/Index) > T-length(exret) # log dividend-to-price ratio > Lmdp=1m(exret[2:T]~dp[1:T-1]) > View(Lmdp) > summary(Lmdp) Call: lm(formula - exret[2:T] ~ dp[1:T - 1]) Residuals: Min 10 Median 30 Max -0.60678 -0.13020 0.02396 0.14358 0.39421 Coefficients: Estimate Std. Error t value Pr(>It!) (Intercept) 0.33301 0.15107 2.204 dp[1:1] 0.07474 0.04429 0.0301 - 1.688 0.0950. --- Signif. codes: 0***** 0.001 **** 0.01 *** 0.05 0.1'1 Residual standard error: 0.1973 on 89 degrees of freedom Multiple R-squared: 0.03101, Adjusted R-squared: 0.02012 F-statistic: 2.848 on 1 and 89 DF, p-value: 0.09498 > anova (Lmdp) Analysis of Variance Table Response: exret[2:T] dp [1:1] Residuals Df Sum Sq Mean Sq F value Pr(>F) 10.1109 0.110873 2.8481 0.09498. 89 3.4646 0.038928 Signif. codes: 0 ***** 0.001 *** 0.01 *** 0.05 0.1' ' 1 > plot(x=dp[1:T-1], y=exret [2:T], main="exret-dp") > abline(lm(exret [2:T]~dp[1:T-1]))

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: Thomas Garman, Raymond Forgue

12th edition

9781305176409, 1133595839, 1305176405, 978-1133595830