PLEASE REFER BELOW BEFORE SUBMITTING A QUESTION ISSUE

Relevant additional information in (10.) is used only when needed. Most of it is unnecessary

I cannot simplify this question it comes as per my attachment. All components are used.

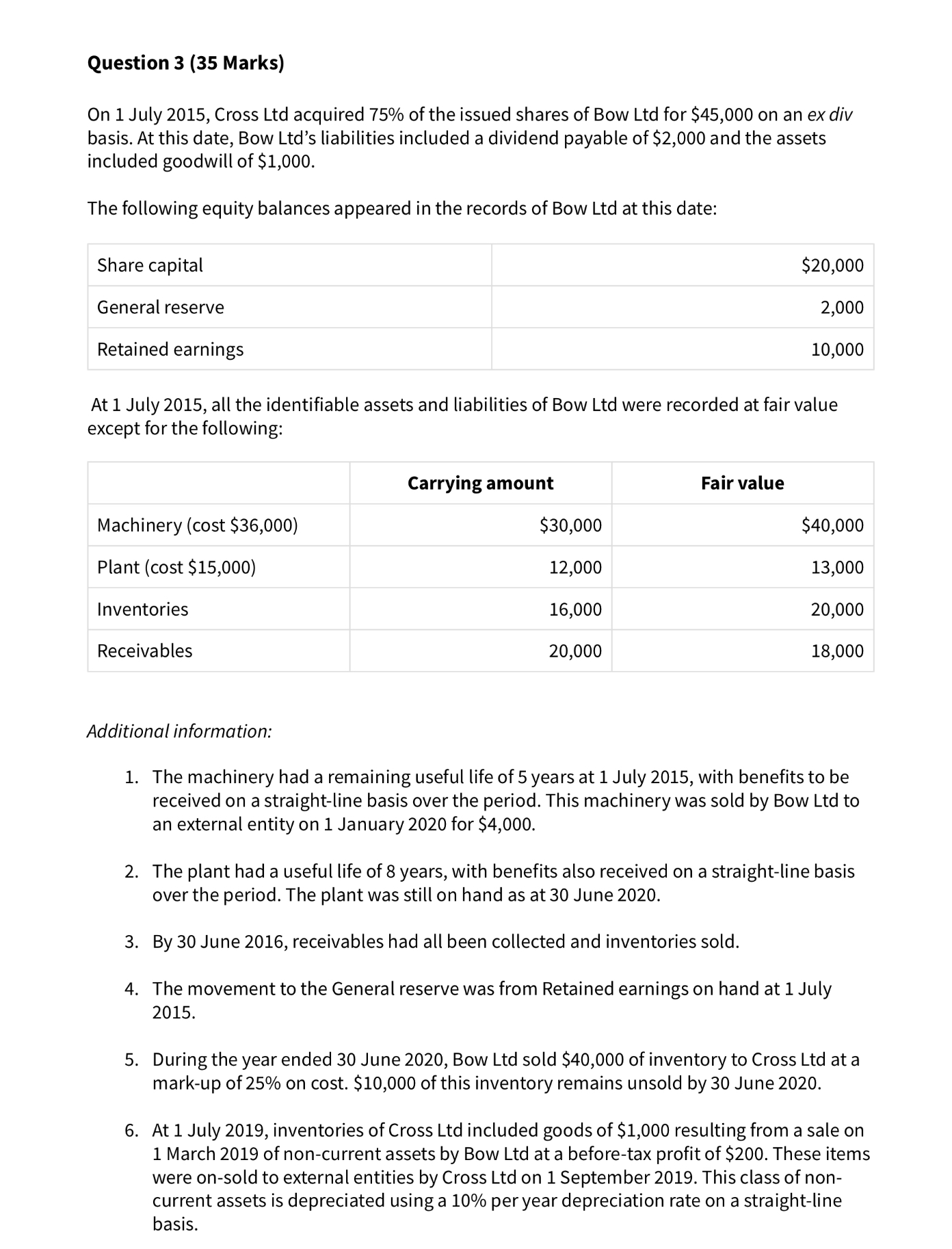

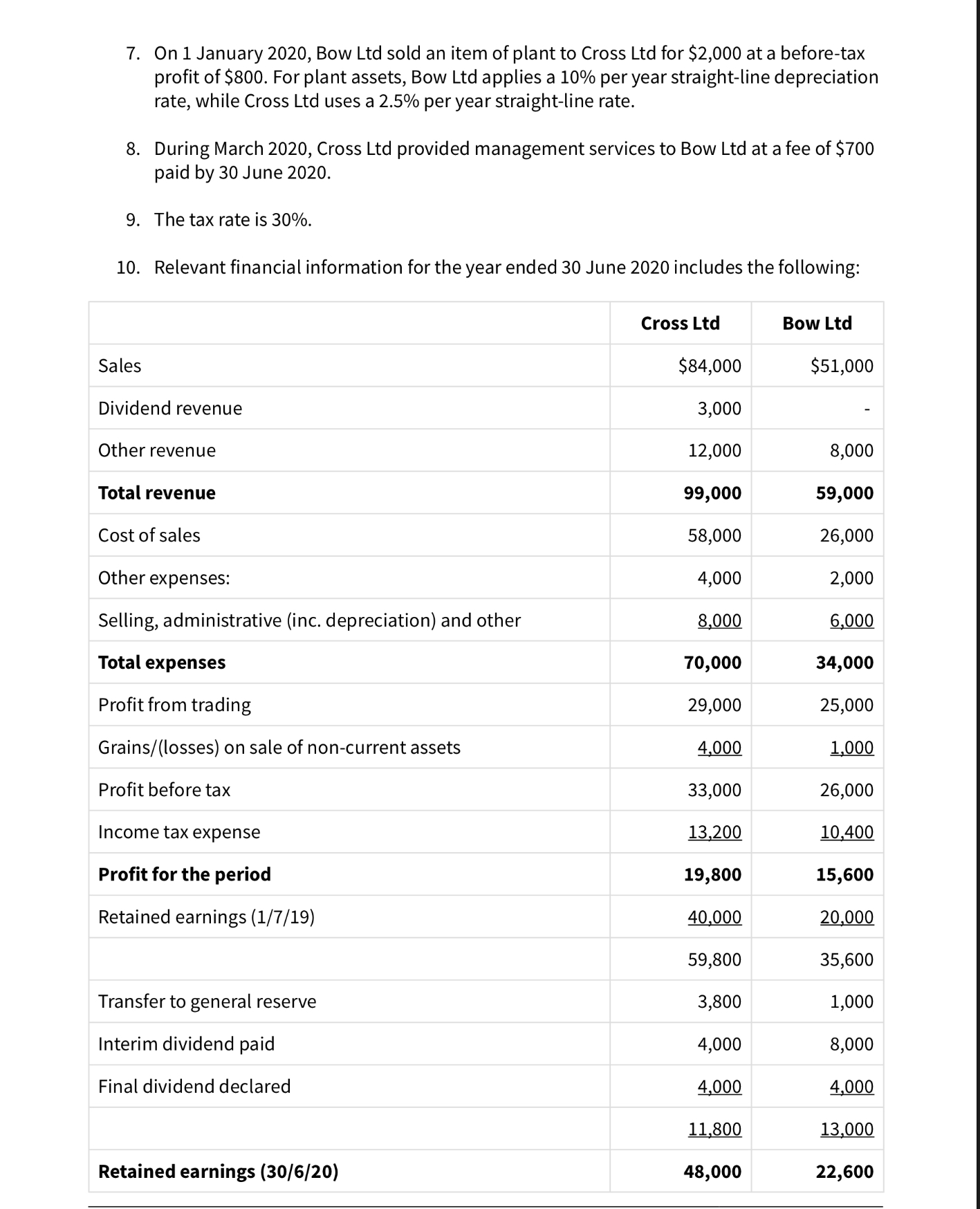

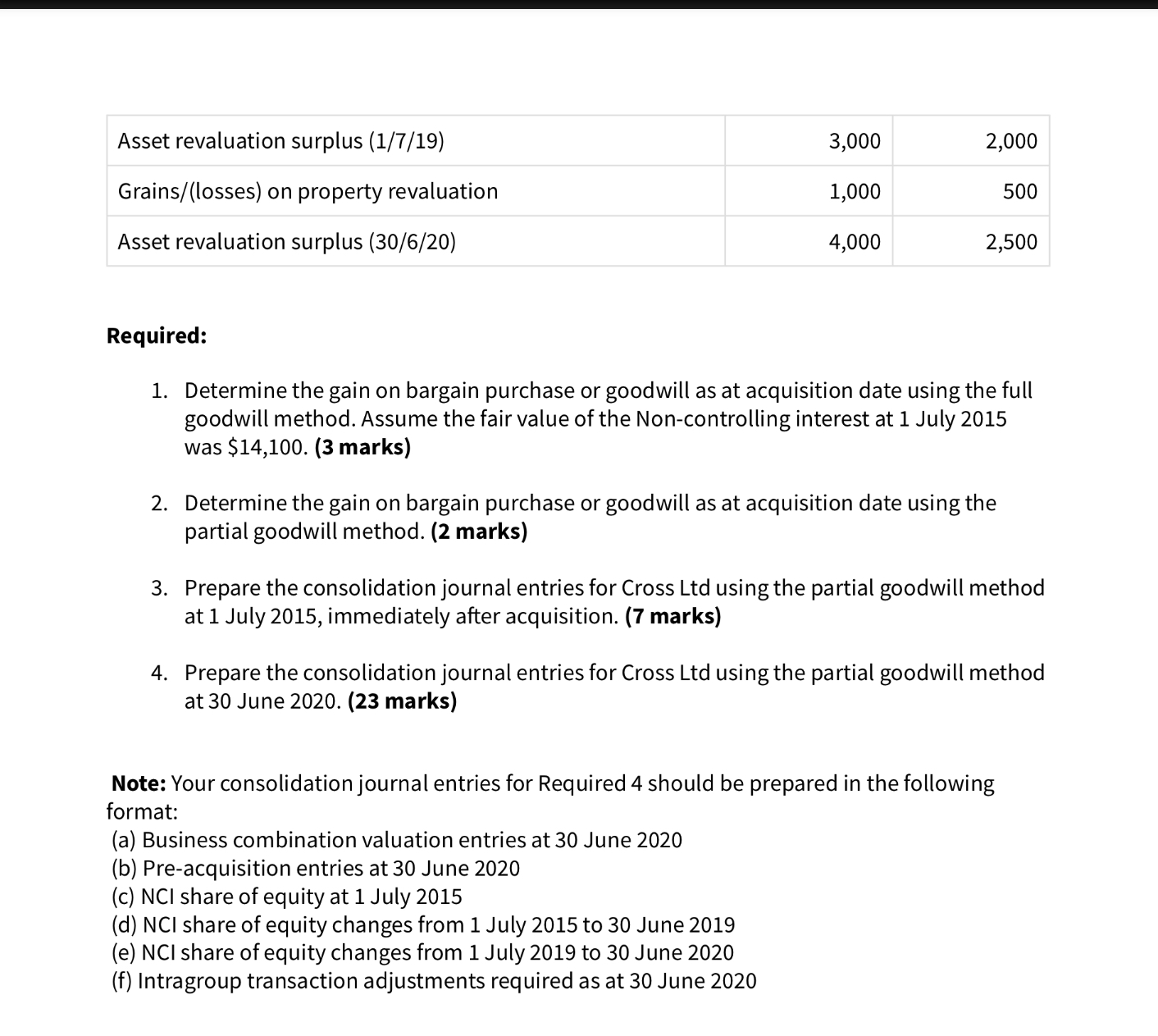

Question 3 (35 Marks) On 1 July 2015, Cross Ltd acquired 75% of the issued shares of Bow Ltd for $45,000 on an ex div basis. At this date, Bow Ltd's liabilities included a dividend payable of $2,000 and the assets included goodwill of $1,000. The following equity balances appeared in the records of Bow Ltd at this date: Share capital $20,000 General reserve 2,000 Retained earnings 10,000 At 1 July 2015, all the identifiable assets and liabilities of Bow Ltd were recorded at fair value except for the following: Carrying amount Fair value Machinery (cost $36,000) $30,000 $40,000 Plant (cost $15,000) 12,000 13,000 Inventories 16,000 20,000 Receivables 20,000 18,000 Additional information: 1. The machinery had a remaining useful life of 5 years at 1 July 2015, with benefits to be received on a straight-line basis over the period. This machinery was sold by Bow Ltd to an external entity on 1 January 2020 for $4,000. 2. The plant had a useful life of8 years, with benefits also received on a straight-line basis over the period. The plant was still on hand as at 30 June 2020. 3. By 30 June 2016, receivables had all been collected and inventories sold. 4. The movement to the General reserve was from Retained earnings on hand at 1 July 2015. 5. During the year ended 30 June 2020, Bow Ltd sold $40,000 of inventory to Cross Ltd at a mark-up of 25% on cost. $10,000 ofthis inventory remains unsold by 30 June 2020. 6. At 1 July 2019, inventories ofCross Ltd included goods of $1,000 resultingfrom a sale on 1 March 2019 of non-current assets by Bow Ltd at a before-tax profit of $200. These items were on-sold to external entities by Cross Ltd on 1 September 2019. This class of non- current assets is depreciated using a 10% per year depreciation rate on a straight-line basis. 7. 0n 1 January 2020, Bow Ltd sold an item of plant to Cross Ltd for $2,000 at a beforetax profit of $800. For plant assets, Bow Ltd applies a 10% per year straight-line depreciation rate, while Cross Ltd uses a 2.5% per year straight-line rate. 8. During March 2020, Cross Ltd provided management services to Bow Ltd at a fee of $700 paid by 30 June 2020. 9. The tax rate is 30%. 10. Relevant financial information for the year ended 30 June 2020 includes the following: Cross Ltd Bow Ltd Sales $84,000 $51,000 Dividend revenue 3,000 - Other revenue 12,000 8,000 Total revenue 99,000 59,000 Cost of sales 58,000 26,000 Other expenses: 4,000 2,000 Selling, administrative (inc. depreciation) and other 8,000 @000 Total expenses 70,000 34,000 Profit from trading 29,000 25,000 Grains/(losses) on sale of non-current assets m m Profit before tax 33,000 26,000 Incometax expense m M Profit for the period 19,800 15,600 Retained earnings (1/7/19) M M 59,800 35,600 Transfer to general reserve 3,800 1,000 Interim dividend paid 4,000 8,000 Final dividend declared 5,000 4 00 M M Retained earnings (30/6/20) 48,000 22,600 Asset revaluation surplus (1/7/19) 3,000 2,000 Grains/(losses) on property revaluation 1,000 500 Asset revaluation surplus (30/6/20) 4,000 2,500 Required: 1. Determine the gain on bargain purchase or goodwill as at acquisition date using the full goodwill method. Assume the fair value ofthe Non-controlling interest at 1 July 2015 was $14,100. (3 marks) 2. Determine the gain on bargain purchase or goodwill as at acquisition date using the partial goodwill method. (2 marks} 3. Prepare the consolidation journal entries for Cross Ltd using the partial goodwill method at 1 July 2015, immediately after acquisition. (7 marks) 4. Prepare the consolidation journal entries for Cross Ltd using the partial goodwill method at 30 June 2020. (23 marks) Note: Your consolidationjournal entries for Required 4 should be prepared in the following format: (a) Business combination valuation entries at 30 June 2020 (b) Pre-acquisition entries at 30 June 2020 (c) NCI share of equity at 1 July 2015 (d) NCI share of equity changes from 1 July 2015 to 30 June 2019 (e) NCI share of equity changes from 1 July 2019 to 30 June 2020 (f) Intragroup transaction adjustments required as at 30 June 2020