Answered step by step

Verified Expert Solution

Question

1 Approved Answer

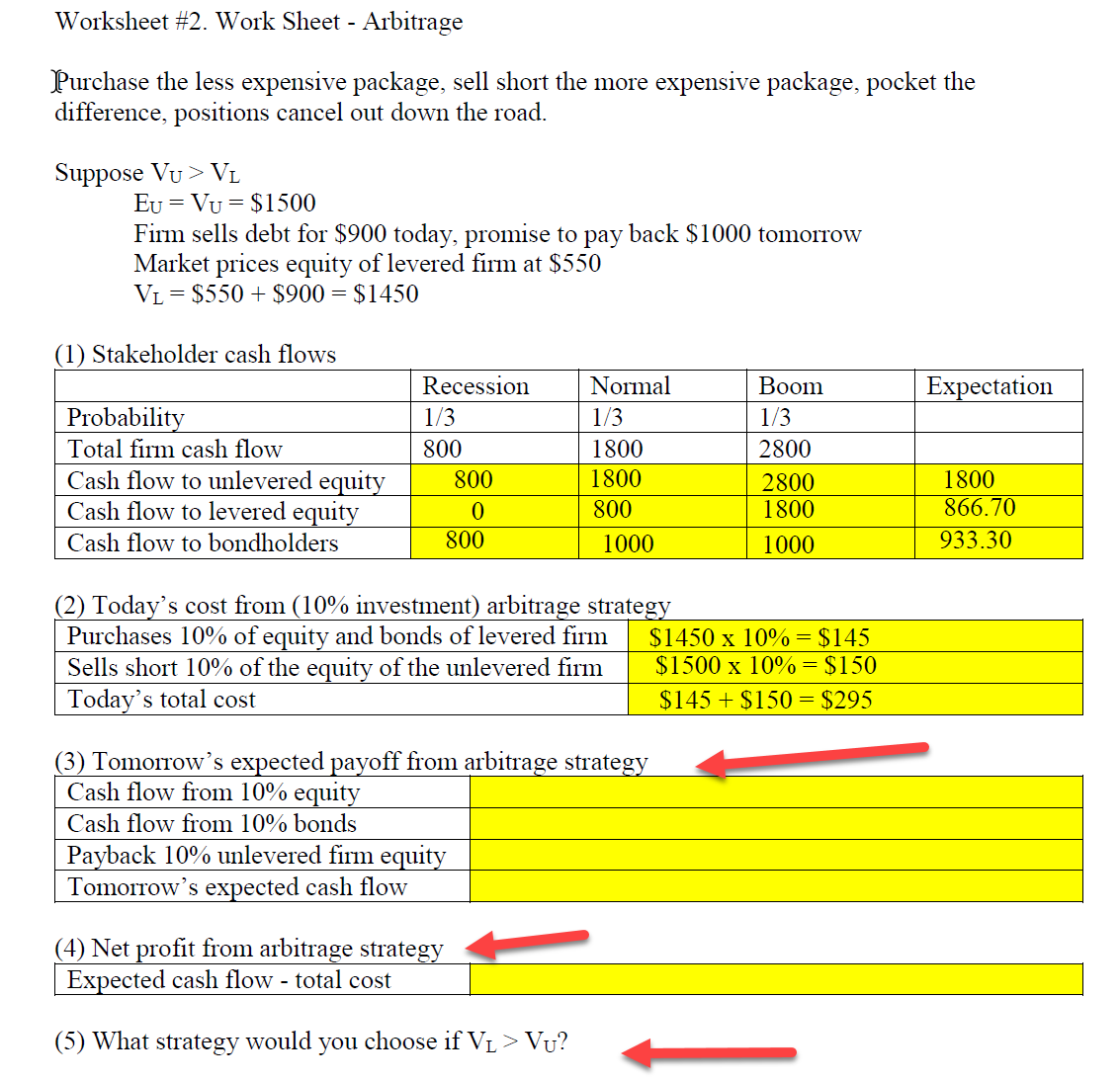

Please review my answers to Questions #1 & #2. Provide solutions for Questions 3-5 (Red Arrows are pointing to) Worksheet #2. Work Sheet - Arbitrage

Please review my answers to Questions #1 & #2. Provide solutions for Questions 3-5 (Red Arrows are pointing to)

Worksheet \#2. Work Sheet - Arbitrage Purchase the less expensive package, sell short the more expensive package, pocket the difference, positions cancel out down the road. Suppose VU>VL EU=VU=$1500 Firm sells debt for $900 today, promise to pay back $1000 tomorrow Market prices equity of levered firm at $550 VL=$550+$900=$1450 (1) Stakahnlder nach flntxre (3) Tomorrow's expected pavoff from arbitrage strategv (5) What strategy would you choose if VL>VUStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Cash What You Need To Know About Bch

Authors: Alexander O. M.

1st Edition

1976721229, 978-1976721229