Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please see picture Problem 5 (9) Consider two rms A and B. The weekly returns of Firm A have a normal distribution with p :

Please see picture

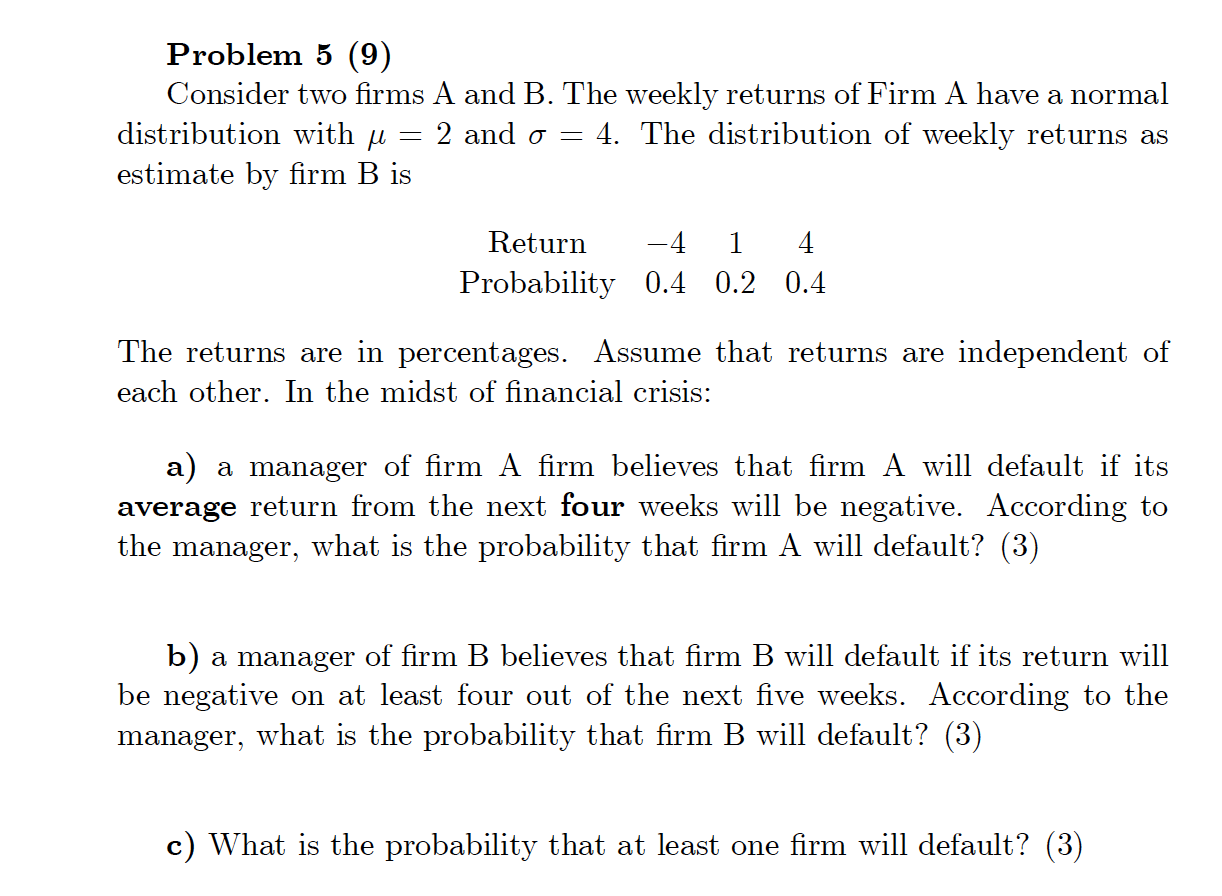

Problem 5 (9) Consider two rms A and B. The weekly returns of Firm A have a normal distribution with p : 2 and a : 4. The distribution of weekly returns as estimate by rm B is Return *4 1 4 Probability 0.4 0.2 0.4 The returns are in percentages. Assume that returns are independent of each other. In the midst of nancial crisis: a) a manager of rm A rm believes that rm A will default if its average return from the next four weeks will be negative. According to the manager, what is the probability that rm A will default? (3) b) a manager of rm B believes that rm B will default if its return will be negative on at least four out of the next ve weeks. According to the manager, what is the probability that rm B will default? (3) c) What is the probability that at least one rm will default? (3)

Problem 5 (9) Consider two rms A and B. The weekly returns of Firm A have a normal distribution with p : 2 and a : 4. The distribution of weekly returns as estimate by rm B is Return *4 1 4 Probability 0.4 0.2 0.4 The returns are in percentages. Assume that returns are independent of each other. In the midst of nancial crisis: a) a manager of rm A rm believes that rm A will default if its average return from the next four weeks will be negative. According to the manager, what is the probability that rm A will default? (3) b) a manager of rm B believes that rm B will default if its return will be negative on at least four out of the next ve weeks. According to the manager, what is the probability that rm B will default? (3) c) What is the probability that at least one rm will default? (3) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Saxon Algebra 1/2 An Incremental Development, Test Forms

Authors: Saxon Publishers

3rd Edition

9781591411734, 1591411734