Please show all accurate calculations.

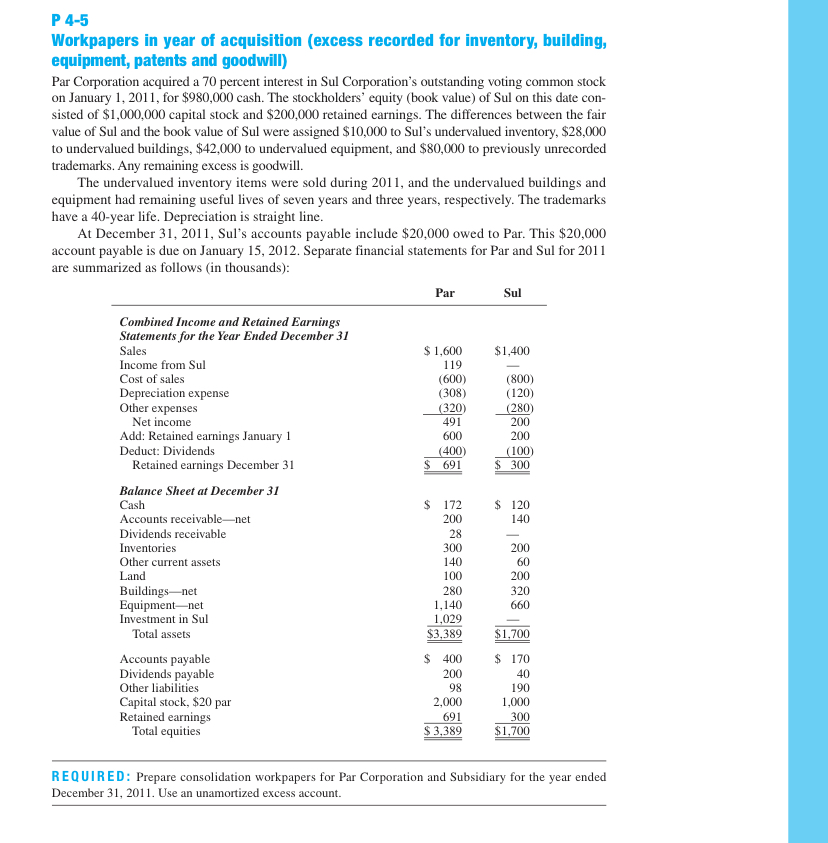

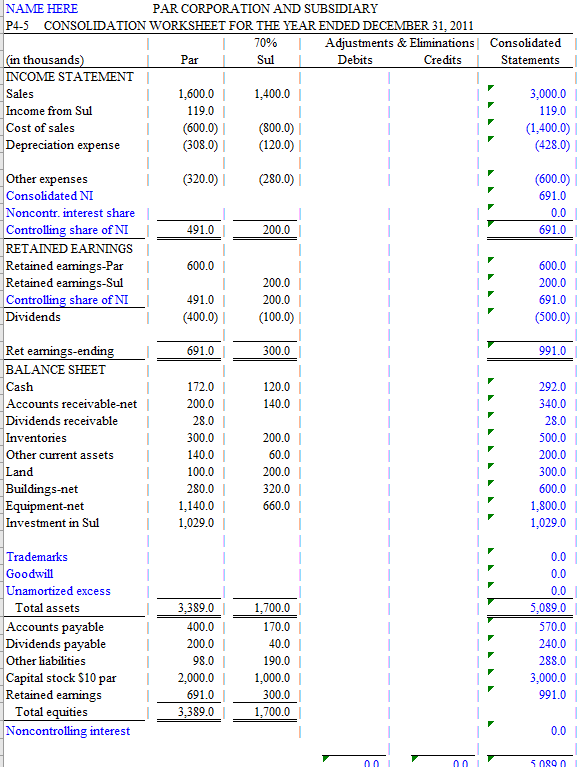

P 4-5 Workpapers in year of acquisition (excess recorded for inventory, building, equipment, patents and goodwill) Par Corporation acquired a 70 percent interest in Sul Corporation's outstanding voting common stock on January 1, 2011, for $980,000 cash. The stockholders' equity (book value) of Sul on this date con- sisted of $1,000,000 capital stock and $200,000 retained earnings. The differences between the fair value of Sul and the book value of Sul were assigned $10,000 to Sul's undervalued inventory, $28,000 to undervalued buildings, $42,000 to undervalued equipment, and $80,000 to previously unrecorded trademarks. Any remaining excess is goodwill. The undervalued inventory items were sold during 2011, and the undervalued buildings and equipment had remaining useful lives of seven years and three years, respectively. The trademarks have a 40-year life. Depreciation is straight line. At December 31, 2011, Sul's accounts payable include $20,000 owed to Par. This $20,000 account payable is due on January 15, 2012. Separate financial statements for Par and Sul for 2011 are summarized as follows (in thousands): Par Sul Combined Income and Retained Earnings Statements for the Year Ended December 31 Sales $ 1,600 $1,400 Income from Sul Cost of sales (800) Depreciation expense (308) (120) Other expenses (320) (280) Net income 491 200 Add: Retained earnings January 1 Deduct: Dividends (400) (100) Retained earnings December 31 $ 300 Balance Sheet at December 31 Cash $ 172 $ 120 Accounts receivable-net Dividends receivable Inventories 300 Other current assets 140 Land 100 200 Buildings-net 280 Equipment-net 1,140 Investment in Sul 1,029 Total assets $1,700 Accounts payable $ 400 $ 170 Dividends payable 200 Other liabilities 98 Capital stock, $20 par 2,000 1,000 Retained earnings Total equities $3,389 $1,700 119 (600) 600 200 $ 691 140 200 28 200 60 320 660 $3,389 40 190 691 300 REQUIRED: Prepare consolidation workpapers for Par Corporation and Subsidiary for the year ended December 31, 2011. Use an unamortized excess account. Consolidated Statements NAME HERE PAR CORPORATION AND SUBSIDIARY P4-5 CONSOLIDATION WORKSHEET FOR THE YEAR ENDED DECEMBER 31, 2011 70% Adjustments & Eliminations (in thousands) Par Sul Debits Credits INCOME STATEMENT Sales 1,600.0 | 1,400.0 Income from Sul 119.0 Cost of sales (600.0) (800.0) Depreciation expense (308.0) (120.0) 3,000.0 119.0 (1,400.0) (428.0) I (320.0) (280.0) (600.0) 691.0 0.0 691.0 491.0 200.0 Other expenses Consolidated NI Noncontr. interest share Controlling share of NI RETAINED EARNINGS Retained earnings-Par Retained eamings-Sul Controlling share of NI Dividends 600.0 491.01 (400.0) 200.0 200.0 (100.0) 600.0 200.0 691.0 (500.0) 691.0 300.0 991.0 120.01 140.0 Ret eamings-ending BALANCE SHEET Cash Accounts receivable-net Dividends receivable Inventories Other current assets Land Buildings-net Equipment-net Investment in Sul 172.0 200.0 28.01 300.0 140.0 100.0 280.0 1,140.0 1,029.0 | 200.0 60.0 292.0 340.0 28.0 500.0 200.0 300.0 600.0 1.800.0 1,029.0 200.0 320.0 660.0 0.01 Trademarks Goodwill Unamortized excess Total assets Accounts payable Dividends payable Other liabilities Capital stock $10 par Retained earnings Total equities Noncontrolling interest 3,389.0 400.0 200.0 98.0 2,000.0 691.0 3,389.0 1,700.0 170.0 40.0 190.0 1,000.0 300.0 1,700.0 0.0 0.0 5,089.0 570.0 240.0 288.0 3,000.0 991.0 0.0 5089 P 4-5 Workpapers in year of acquisition (excess recorded for inventory, building, equipment, patents and goodwill) Par Corporation acquired a 70 percent interest in Sul Corporation's outstanding voting common stock on January 1, 2011, for $980,000 cash. The stockholders' equity (book value) of Sul on this date con- sisted of $1,000,000 capital stock and $200,000 retained earnings. The differences between the fair value of Sul and the book value of Sul were assigned $10,000 to Sul's undervalued inventory, $28,000 to undervalued buildings, $42,000 to undervalued equipment, and $80,000 to previously unrecorded trademarks. Any remaining excess is goodwill. The undervalued inventory items were sold during 2011, and the undervalued buildings and equipment had remaining useful lives of seven years and three years, respectively. The trademarks have a 40-year life. Depreciation is straight line. At December 31, 2011, Sul's accounts payable include $20,000 owed to Par. This $20,000 account payable is due on January 15, 2012. Separate financial statements for Par and Sul for 2011 are summarized as follows (in thousands): Par Sul Combined Income and Retained Earnings Statements for the Year Ended December 31 Sales $ 1,600 $1,400 Income from Sul Cost of sales (800) Depreciation expense (308) (120) Other expenses (320) (280) Net income 491 200 Add: Retained earnings January 1 Deduct: Dividends (400) (100) Retained earnings December 31 $ 300 Balance Sheet at December 31 Cash $ 172 $ 120 Accounts receivable-net Dividends receivable Inventories 300 Other current assets 140 Land 100 200 Buildings-net 280 Equipment-net 1,140 Investment in Sul 1,029 Total assets $1,700 Accounts payable $ 400 $ 170 Dividends payable 200 Other liabilities 98 Capital stock, $20 par 2,000 1,000 Retained earnings Total equities $3,389 $1,700 119 (600) 600 200 $ 691 140 200 28 200 60 320 660 $3,389 40 190 691 300 REQUIRED: Prepare consolidation workpapers for Par Corporation and Subsidiary for the year ended December 31, 2011. Use an unamortized excess account. Consolidated Statements NAME HERE PAR CORPORATION AND SUBSIDIARY P4-5 CONSOLIDATION WORKSHEET FOR THE YEAR ENDED DECEMBER 31, 2011 70% Adjustments & Eliminations (in thousands) Par Sul Debits Credits INCOME STATEMENT Sales 1,600.0 | 1,400.0 Income from Sul 119.0 Cost of sales (600.0) (800.0) Depreciation expense (308.0) (120.0) 3,000.0 119.0 (1,400.0) (428.0) I (320.0) (280.0) (600.0) 691.0 0.0 691.0 491.0 200.0 Other expenses Consolidated NI Noncontr. interest share Controlling share of NI RETAINED EARNINGS Retained earnings-Par Retained eamings-Sul Controlling share of NI Dividends 600.0 491.01 (400.0) 200.0 200.0 (100.0) 600.0 200.0 691.0 (500.0) 691.0 300.0 991.0 120.01 140.0 Ret eamings-ending BALANCE SHEET Cash Accounts receivable-net Dividends receivable Inventories Other current assets Land Buildings-net Equipment-net Investment in Sul 172.0 200.0 28.01 300.0 140.0 100.0 280.0 1,140.0 1,029.0 | 200.0 60.0 292.0 340.0 28.0 500.0 200.0 300.0 600.0 1.800.0 1,029.0 200.0 320.0 660.0 0.01 Trademarks Goodwill Unamortized excess Total assets Accounts payable Dividends payable Other liabilities Capital stock $10 par Retained earnings Total equities Noncontrolling interest 3,389.0 400.0 200.0 98.0 2,000.0 691.0 3,389.0 1,700.0 170.0 40.0 190.0 1,000.0 300.0 1,700.0 0.0 0.0 5,089.0 570.0 240.0 288.0 3,000.0 991.0 0.0 5089