Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show all calculations step by step so I can fully understand how to solve. thank you (answer is provided but I don't know how

Please show all calculations step by step so I can fully understand how to solve. thank you (answer is provided but I don't know how to get there)

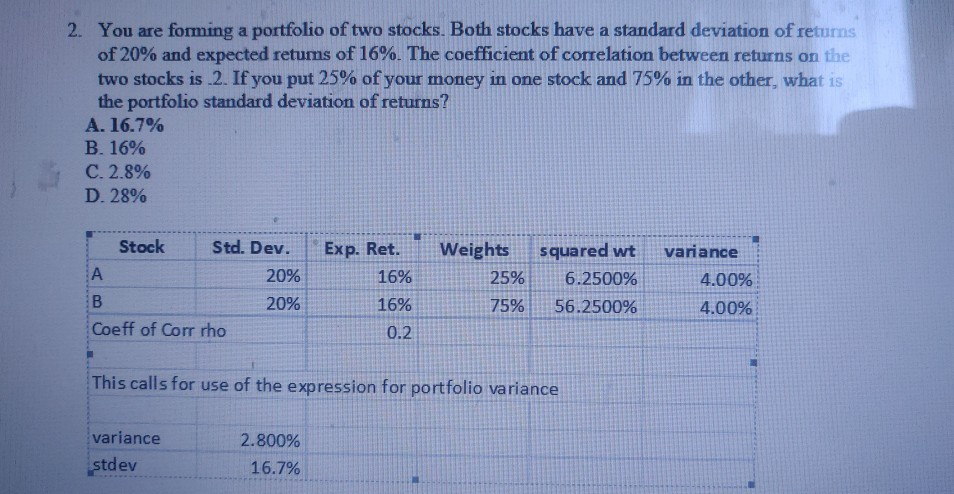

2. You are forming a portfolio of two stocks. Both stocks have a standard deviation of returns of 20% and expected retums of 16%. The coefficient of correlation between returns on the two stocks is 2. If you put 25% of your money in one stock and 75% in the other, what is the portfolio standard deviation of returns? A. 16.7% B. 16% C.2.8% D. 28% Exp. Ret. 16% Weights 25% Stock Std. Dev. 20% B 20% Coeff of Corr rho squared wt 6.2500% 56.2500% variance 4.00% 4.00% 16% 75% 0.2 This calls for use of the expression for portfolio variance variance stdev 2.800% 16.7%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Recent Advances In Commodity And Financial Modeling

Authors: Giorgio Consigli, Silvana Stefani, Giovanni Zambruno

1st Edition

3319613189, 978-3319613185