Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please show all work and correct answer only! 14. a. Discuss how each of the following theories for the term structure of interest rates could

please show all work and correct answer only!

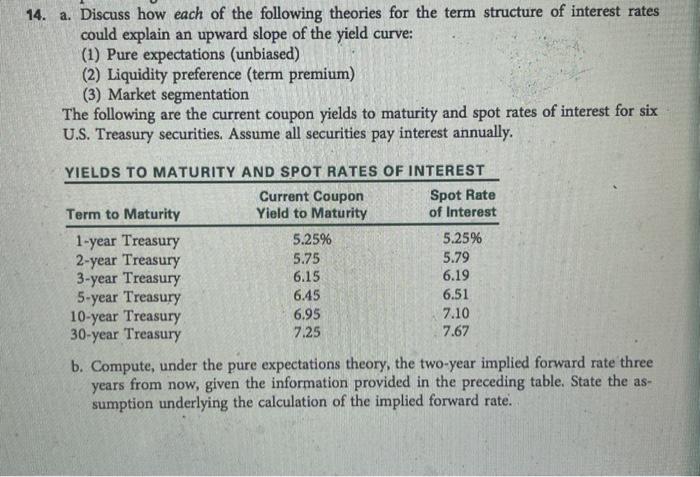

14. a. Discuss how each of the following theories for the term structure of interest rates could explain an upward slope of the yield curve: (1) Pure expectations (unbiased) (2) Liquidity preference (term premium) (3) Market segmentation The following are the current coupon yields to maturity and spot rates of interest for six U.S. Treasury securities. Assume all securities pay interest annually. YIELDS TO MATURITY AND SPOT RATES OF INTEREST Current Coupon Spot Rate Term to Maturity Yield to Maturity of Interest 1-year Treasury 5.25% 5.25% 2-year Treasury 5.75 5.79 3-year Treasury 6.15 6.19 5-year Treasury 6.45 6.51 10-year Treasury 6.95 7.10 30-year Treasury 7.25 7.67 b. Compute, under the pure expectations theory, the two-year implied forward rate three years from now, given the information provided in the preceding table. State the as- sumption underlying the calculation of the implied forward rate Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin Mining The New Gold Rush Bitcoin Mining Is The Future

Authors: Sam Sutton

1st Edition

1985654717, 978-1985654716