Answered step by step

Verified Expert Solution

Question

1 Approved Answer

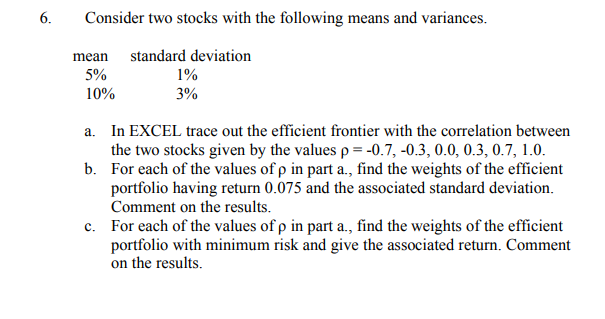

Please show all work and explanations 6 Consider two stocks with the following means and variances. mean standard deviation 5% 190 3% 10% a. In

Please show all work and explanations

6 Consider two stocks with the following means and variances. mean standard deviation 5% 190 3% 10% a. In EXCEL trace out the efficient frontier with the correlation between b. er cac h of the: valucs offpiput a., ficl the: wcighis of ihe nt the two stocks given by the values p--0.7, -0.3,0.0, 0.3, 0.7, 1.0 portfolio having return 0.075 and the associated standard deviation. Comment on the results. c. For each of the values of p in part a., find the weights of the efficient portfolio with minimum risk and give the associated return. Comment on the resultsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Capital Markets Institutions And Instruments

Authors: Frank J. Fabozzi, Franco Modigliani

4th Edition

0136026028, 9780136026020