Answered step by step

Verified Expert Solution

Question

1 Approved Answer

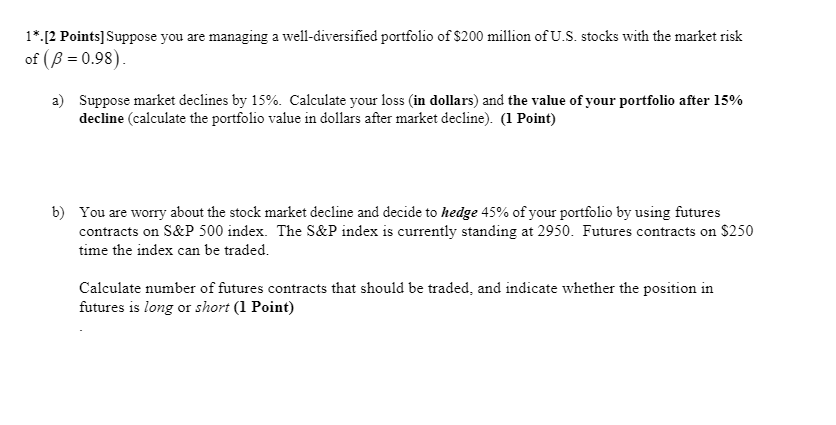

Please show all work, calculations, etc 1*.[2 Points]Suppose you are managing a well-diversified portfolio of $200 million of U.S. stocks with the market risk of

Please show all work, calculations, etc

1*.[2 Points]Suppose you are managing a well-diversified portfolio of $200 million of U.S. stocks with the market risk of B = 0.98). a) Suppose market declines by 15%. Calculate your loss (in dollars) and the value of your portfolio after 15% decline (calculate the portfolio value in dollars after market decline). (1 Point) b) You are worry about the stock market decline and decide to hedge 45% of your portfolio by using futures contracts on S&P 500 index. The S&P index is currently standing at 2950. Futures contracts on $250 time the index can be traded. Calculate number of futures contracts that should be traded, and indicate whether the position in futures is long or short (1 Point)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: Philip J. Adelman, Alan M. Marks

4th Edition

0132434792, 9780132434799