Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show all work Problem # 1 Monthly return data are presented below for each of the two stocks and the S&P index for a

Please show all work

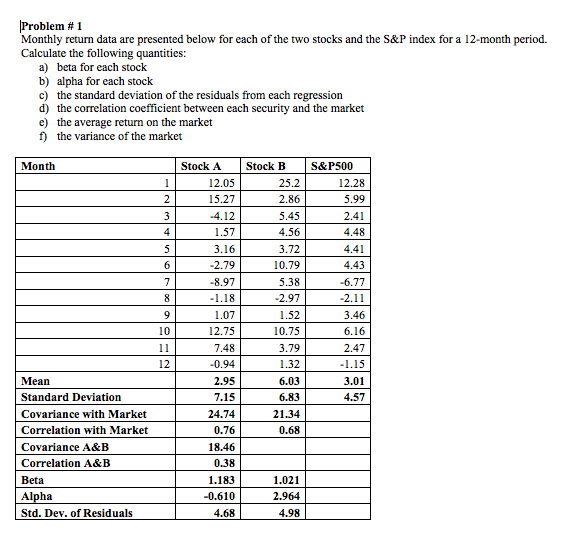

Problem # 1 Monthly return data are presented below for each of the two stocks and the S&P index for a 12-month period. Calculate the following quantities: a) beta for each stock b) alpha for each stock c) the standard deviation of the residuals from each regression d) the correlation coefficient between each security and the market e) th f) the variance of the market e average return on the market Month Stock A Stock B S&P500 12.05 15.27 4.12 1.57 3.16 2.79 -8.97 1.18 1.07 12.75 7.48 0.94 2.95 7.15 24.74 0.76 18.46 0.38 1.183 0.610 4.68 25.2 2.86 5.45 4.56 3.72 10.79 5.38 2.97 1.52 10.75 3.79 1.32 6.03 6.83 21.34 0.68 12.28 5.99 2.41 4.48 4.41 4.43 6.77 2.11 3.46 6.16 2.47 1.15 3.01 4.57 10 12 Mean Standard Deviation Covariance with Market Correlation with Market Covariance A&B Correlation A&B Beta Alpha Std. Dev. of Residuals 1.021 2.964 4.98

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financing California Real Estate Spanish Missions To Subprime Mortgages

Authors: Lynne P. Doti

1st Edition

184893601X, 978-1848936010