Answered step by step

Verified Expert Solution

Question

1 Approved Answer

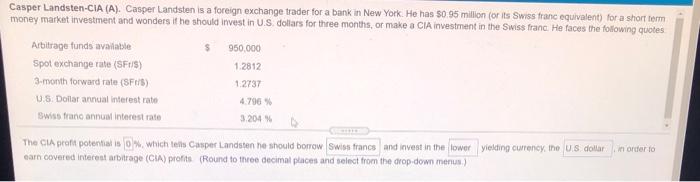

please show all work! Thanks Casper Landsten-CIA (A). Casper Landsten is a foreign exchange trader for a bank in New York. He has $0.95 million

please show all work! Thanks

Casper Landsten-CIA (A). Casper Landsten is a foreign exchange trader for a bank in New York. He has $0.95 million (or its Swiss franc equivalent) for a short form money market investment and wonders it he should invest in US dollars for three months, or make a CIA investment in the Swiss franc He faces the following quotes Arbitrage funds available 950.000 Spot exchange rate (SFt/s) 1.2812 3-month forward rate (SF68) 1.2737 US Dollar annual interest rate Swiss franc annual interest rato 3.204 The CIA proto potential in which tes Casper Landsten he should borrow Swan francs and invest in the lower yielding currency, the US dollar earn covered interest arbitrage (CIA) profits (Round to the decimal places and select from the drop-down menus 4.796 in order to Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Equity Analysis and Portfolio Management Tools to Analyze and Manage Your Stock Portfolio

Authors: Robert A.Weigand

1st edition

978-111863091, 1118630912, 978-1118630914