Answered step by step

Verified Expert Solution

Question

1 Approved Answer

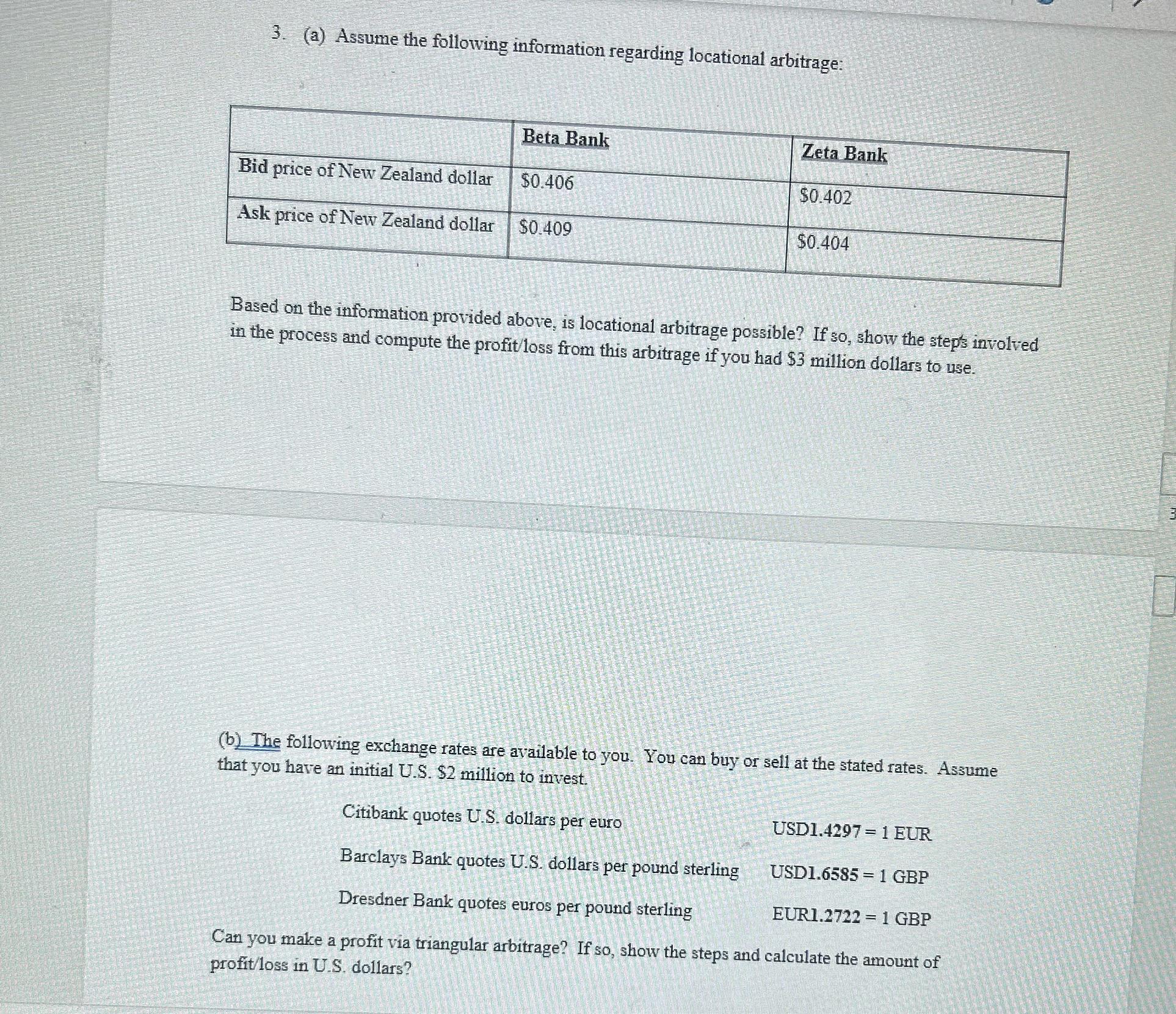

Please show all workings. Thank you. 3. (a) Assume the following information regarding locational arbitrage: Beta Bank Bid price of New Zealand dollar $0.406 Ask

Please show all workings. Thank you.

3. (a) Assume the following information regarding locational arbitrage: Beta Bank Bid price of New Zealand dollar $0.406 Ask price of New Zealand dollar $0.409 Zeta Bank $0.402 $0.404 Based on the information provided above, is locational arbitrage possible? If so, show the steps involved in the process and compute the profit/loss from this arbitrage if you had $3 million dollars to use. (b) The following exchange rates are available to you. You can buy or sell at the stated rates. Assume that you have an initial U.S. $2 million to invest. Citibank quotes U.S. dollars per euro USD1.4297 1 EUR Barclays Bank quotes U.S. dollars per pound sterling USD1.6585 = 1 GBP == Dresdner Bank quotes euros per pound sterling EUR1.2722 = 1 GBP Can you make a profit via triangular arbitrage? If so, show the steps and calculate the amount of profit/loss in U.S. dollars?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

a To determine if locational arbitrage is possible we need to compare the implied cross exchange rate with the actual cross exchange rate The implied ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International financial management

Authors: Jeff Madura

9th Edition

978-0324593495, 324568207, 324568193, 032459349X, 9780324568202, 9780324568196, 978-0324593471