Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please show all workings thank you Question 3 You are the portfolio manager at Financial Trust Ltd, an investment firm that is restructuring a variable

please show all workings thank you

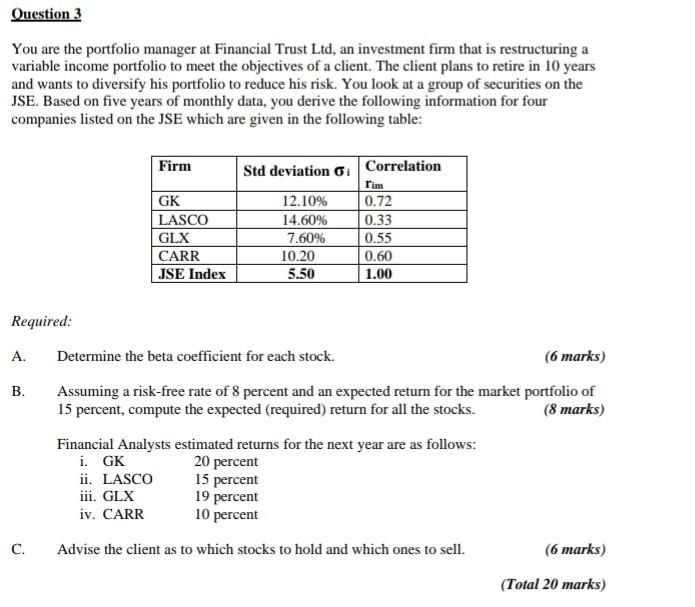

Question 3 You are the portfolio manager at Financial Trust Ltd, an investment firm that is restructuring a variable income portfolio to meet the objectives of a client. The client plans to retire in 10 years and wants to diversify his portfolio to reduce his risk. You look at a group of securities on the JSE. Based on five years of monthly data, you derive the following information for four companies listed on the JSE which are given in the following table: Firm Std deviation 6 Correlation Tim GK 12.10% 0.72 LASCO 14.60% 0.33 GLX 7.60% 0.55 CARR 10.20 0.60 JSE Index 5.50 1.00 Required: A. Determine the beta coefficient for each stock. (6 marks) B. Assuming a risk-free rate of 8 percent and an expected return for the market portfolio of 15 percent, compute the expected (required) return for all the stocks. (8 marks) Financial Analysts estimated returns for the next year are as follows: i. GK 20 percent 15 percent ii. LASCO iii. GLX 19 percent iv. CARR 10 percent Advise the client as to which stocks to hold and which ones to sell. (6 marks) (Total 20 marks) CStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657