Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE SHOW HOW TO CALC MEAN AND VAR FOR YAHOO STOCK USING R. Choose a stock online (e.g., at Yahoo Finance) and assuming that it

PLEASE SHOW HOW TO CALC MEAN AND VAR FOR YAHOO STOCK USING R.

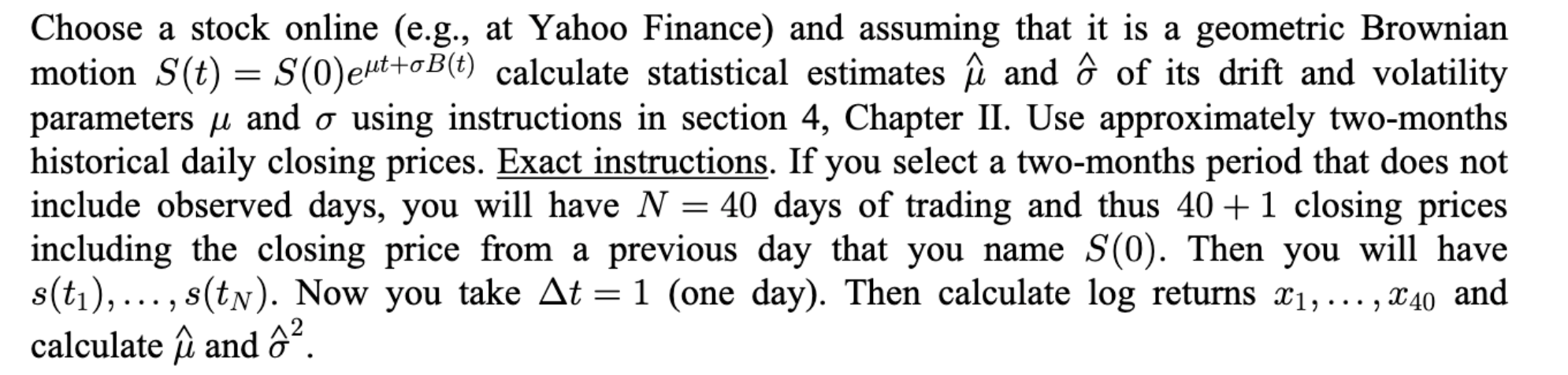

Choose a stock online (e.g., at Yahoo Finance) and assuming that it is a geometric Brownian motion S(t)=S(0)et+B(t) calculate statistical estimates ^ and ^ of its drift and volatility parameters and using instructions in section 4, Chapter II. Use approximately two-months historical daily closing prices. Exact instructions. If you select a two-months period that does not include observed days, you will have N=40 days of trading and thus 40+1 closing prices including the closing price from a previous day that you name S(0). Then you will have s(t1),,s(tN). Now you take t=1 (one day). Then calculate log returns x1,,x40 and calculate ^ and ^2Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started