Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show step by step thank you. Suppose there are two risky assets in the economy. Asset 1 has expected return of 10% and a

Please show step by step thank you.

Please show step by step thank you.

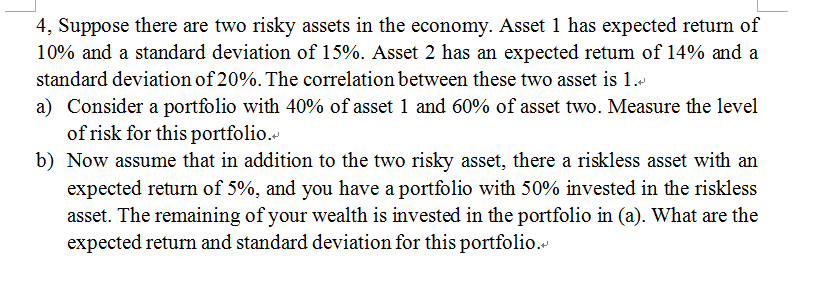

Suppose there are two risky assets in the economy. Asset 1 has expected return of 10% and a standard deviation of 15%. Asset 2 has an expected return of 14% and a standard deviation of 20%. The correlation between these two asset is 1. Consider a portfolio with 40% of asset 1 and 60% of asset two. Measure the level of risk for this portfolio. Now assume that in addition to the two risky asset, there a riskless asset with an expected return of 5% and you have a portfolio with 50% invested in the riskless asset. The remaining of your wealth is invested in the portfolio in What are the expected return and standard deviation for this portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Sustainability In Public Administration Exploring The Concept Of Financial Health

Authors: Manuel Pedro Rodríguez Bolívar

1st Edition

3319579614, 3319579622, 9783319579610, 9783319579627