Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show step-by-step answers On June 21, 2016, ZAAG acquired iFrogz for $96.2 million. The excess of the acquisition price over the fair value of

Please show step-by-step answers

- On June 21, 2016, ZAAG acquired iFrogz for $96.2 million. The excess of the acquisition price over the fair value of iFrogz's net assets (ie, tangible assets and identifiable intangible assets, net of assumed liabilities) was $6.925 million, which was recorded as "Goodwill" at the time of the acquisition.

- For book purposes, goodwill is tested annually for impairment. In Note 7, ZAGG discloses that it conducted a goodwill impairment analysis during the fourth quarter of 2017. What was the amount of the impairment in goodwill that resulted from this analysis in 2017?

- For tax purposes, goodwill is amortized annually and is, therefore, a deductible expense on a company's tax return. ZAGG amortized goodwill over a period of 15 years. Note 8 reports a deferred income tax asset of $1,801,000 related to goodwill at December 31, 2017. Explain how goodwill created a deferred income tax asset for ZAGG. Show how ZAGG arrived at this number. You may assume a 35% federal statutory tax rate and a 3% blended state statutory tax rate and that ZAGG began amortizing goodwill for tax purposes starting in July, 2016. [Hint: determine the net (ie, after amortization) value of goodwill for tax purposes to compare to the net book value of goodwill.]

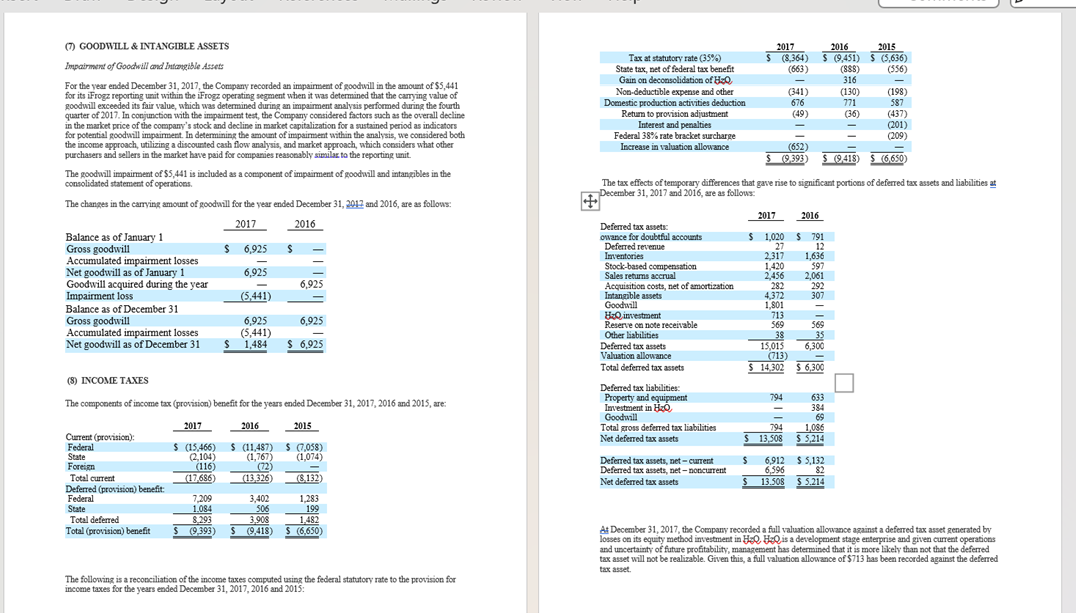

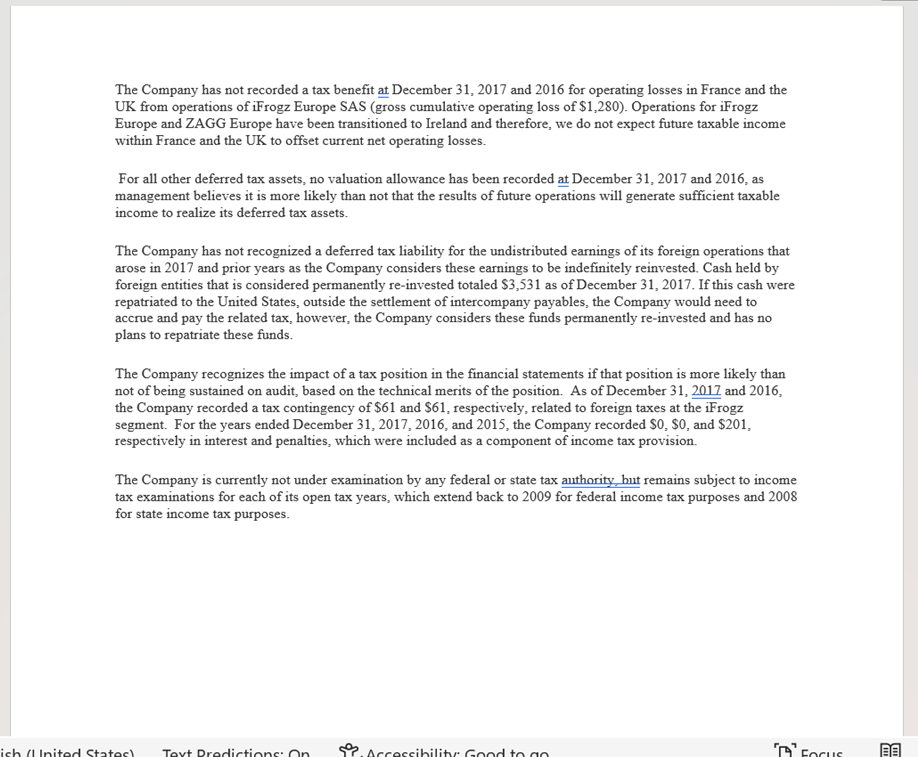

(7) GOODWILL \& INTANGIBLE ASSETS Impairmert of Goodwill and Intosgible Assets For the year ended December 31, 2017, the Company recorded an impaiment of aoodvill in the amount of $5,441 for its IFrogz reporting unit within the IFrogz operating segment when it was determined that the carrying value of goodwill exceeded its fair value, which was determined during an impaiment analysis performed during the fourth quarter of 2017. In conjunction with the impairment test, the Company considered factors such as the overall decline in the maxket price of the company's stock and doclise in market capitalization for a sustained period as indicators for potential gooduall impaiment In determining the amoumt of impaiment within the analysis, we considered both the income approach, utilizing a discourted cash flow analysis, and market approach, which considers what other purchasers and sellers in the market have paid for companies reasonably similas to the reporting unit. The goodvill impaiment of $5,441 is included as a compobent of impaiment of goodvill and intanqubles in the consolidnted statement of operations. The changes in the carrying amount of goodwill for the vear ended December 31,2012 and 2016, are as follows: The tax effects of temaporary differences that gave rise to significant portions of deferred tax assets and liabilities at December 31, 2017 and 2016, are as follows: (8) INCOME TAXES The components of income tax (provision) benefit for the years ended December 31, 2017, 2016 and 2015, are: The following is a reconciliation of the income taxes computed using the federal statutory rate to the provision for At December 31,2017, the Company recorded a full valuation allowance aquinst a deferred tax asset renerated by losses on its equity metbod investment in HFQ HzQ is a development stage enterprise and given current operations and uncertainty of future profitabality, management has determined that it is more likely than not that the deferred tax asset will not be realizable. Given this, a full valuation allowance of $713 has been recorded against the deferred tax asset. income taxes for the years ended December 31, 2017, 2016 and 2015: The Company has not recorded a tax benefit at December 31, 2017 and 2016 for operating losses in France and the UK from operations of iFrogz Europe SAS (gross cumulative operating loss of \$1,280). Operations for iFrogz Europe and ZAGG Europe have been transitioned to Ireland and therefore, we do not expect future taxable income within France and the UK to offset current net operating losses. For all other deferred tax assets, no valuation allowance has been recorded at December 31, 2017 and 2016, as management believes it is more likely than not that the results of future operations will generate sufficient taxable income to realize its deferred tax assets. The Company has not recognized a deferred tax liability for the undistributed earnings of its foreign operations that arose in 2017 and prior years as the Company considers these earnings to be indefinitely reinvested. Cash held by foreign entities that is considered permanently re-invested totaled $3,531 as of December 31,2017 . If this cash were repatriated to the United States, outside the settlement of intercompany payables, the Company would need to accrue and pay the related tax, however, the Company considers these funds permanently re-invested and has no plans to repatriate these funds. The Company recognizes the impact of a tax position in the financial statements if that position is more likely than not of being sustained on audit, based on the technical merits of the position. As of December 31, 2017 and 2016, the Company recorded a tax contingency of $61 and $61, respectively, related to foreign taxes at the iFrogz segment. For the years ended December 31,2017,2016, and 2015, the Company recorded \$0, \$0, and \$201, respectively in interest and penalties, which were included as a component of income tax provision. The Company is currently not under examination by any federal or state tax authority hut remains subject to income tax examinations for each of its open tax years, which extend back to 2009 for federal income tax purposes and 2008 for state income tax purposes

(7) GOODWILL \& INTANGIBLE ASSETS Impairmert of Goodwill and Intosgible Assets For the year ended December 31, 2017, the Company recorded an impaiment of aoodvill in the amount of $5,441 for its IFrogz reporting unit within the IFrogz operating segment when it was determined that the carrying value of goodwill exceeded its fair value, which was determined during an impaiment analysis performed during the fourth quarter of 2017. In conjunction with the impairment test, the Company considered factors such as the overall decline in the maxket price of the company's stock and doclise in market capitalization for a sustained period as indicators for potential gooduall impaiment In determining the amoumt of impaiment within the analysis, we considered both the income approach, utilizing a discourted cash flow analysis, and market approach, which considers what other purchasers and sellers in the market have paid for companies reasonably similas to the reporting unit. The goodvill impaiment of $5,441 is included as a compobent of impaiment of goodvill and intanqubles in the consolidnted statement of operations. The changes in the carrying amount of goodwill for the vear ended December 31,2012 and 2016, are as follows: The tax effects of temaporary differences that gave rise to significant portions of deferred tax assets and liabilities at December 31, 2017 and 2016, are as follows: (8) INCOME TAXES The components of income tax (provision) benefit for the years ended December 31, 2017, 2016 and 2015, are: The following is a reconciliation of the income taxes computed using the federal statutory rate to the provision for At December 31,2017, the Company recorded a full valuation allowance aquinst a deferred tax asset renerated by losses on its equity metbod investment in HFQ HzQ is a development stage enterprise and given current operations and uncertainty of future profitabality, management has determined that it is more likely than not that the deferred tax asset will not be realizable. Given this, a full valuation allowance of $713 has been recorded against the deferred tax asset. income taxes for the years ended December 31, 2017, 2016 and 2015: The Company has not recorded a tax benefit at December 31, 2017 and 2016 for operating losses in France and the UK from operations of iFrogz Europe SAS (gross cumulative operating loss of \$1,280). Operations for iFrogz Europe and ZAGG Europe have been transitioned to Ireland and therefore, we do not expect future taxable income within France and the UK to offset current net operating losses. For all other deferred tax assets, no valuation allowance has been recorded at December 31, 2017 and 2016, as management believes it is more likely than not that the results of future operations will generate sufficient taxable income to realize its deferred tax assets. The Company has not recognized a deferred tax liability for the undistributed earnings of its foreign operations that arose in 2017 and prior years as the Company considers these earnings to be indefinitely reinvested. Cash held by foreign entities that is considered permanently re-invested totaled $3,531 as of December 31,2017 . If this cash were repatriated to the United States, outside the settlement of intercompany payables, the Company would need to accrue and pay the related tax, however, the Company considers these funds permanently re-invested and has no plans to repatriate these funds. The Company recognizes the impact of a tax position in the financial statements if that position is more likely than not of being sustained on audit, based on the technical merits of the position. As of December 31, 2017 and 2016, the Company recorded a tax contingency of $61 and $61, respectively, related to foreign taxes at the iFrogz segment. For the years ended December 31,2017,2016, and 2015, the Company recorded \$0, \$0, and \$201, respectively in interest and penalties, which were included as a component of income tax provision. The Company is currently not under examination by any federal or state tax authority hut remains subject to income tax examinations for each of its open tax years, which extend back to 2009 for federal income tax purposes and 2008 for state income tax purposes Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Ba 213 At Central Oregon Community College

Authors: Albrecht

1st Edition

1111523622, 978-1111523626