Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please show the calculation step by step. answer only 4b) and 4c). appreciate (a) The following represents the information for two stocks, A1 and B2:

please show the calculation step by step. answer only 4b) and 4c). appreciate

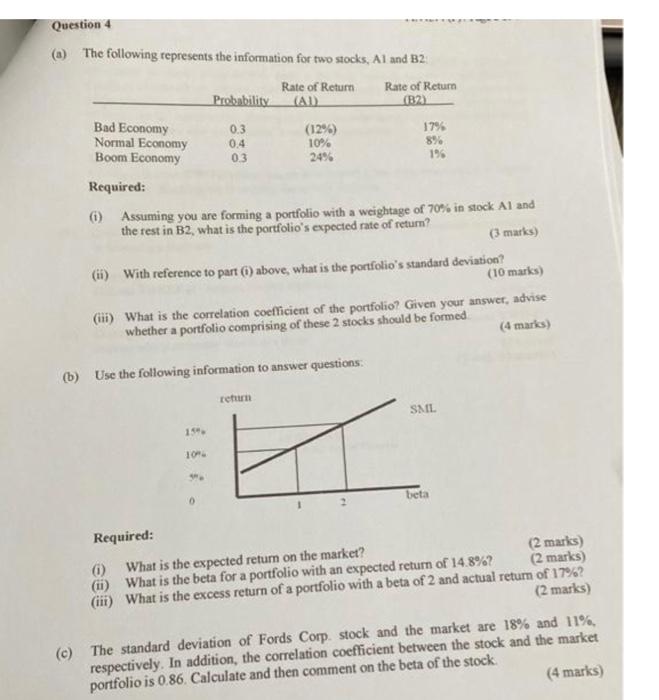

(a) The following represents the information for two stocks, A1 and B2: Required: (i) Assuming you are forming a portfolio with a weightage of 70% in stock A1 and the rest in B2, what is the portfolio's expected rate of return? (3 marks) (ii) With reference to part (i) above, what is the portfolio's standard deviation? (10 marks) (iii) What is the correlation coefficient of the portfolio? Griven your answer, advise whether a portfolio comprising of these 2 stocks should be formed (4 marks) (b) Use the following information to answer questions: Required: (i) What is the expected retum on the market? (2 marks) (ii) What is the beta for a portfolio with an expected return of 14.8% ( 2 marks) (iii) What is the excess return of a portfolio with a beta of 2 and actual return of 17% ? (2 marks) (c) The standard deviation of Fords Corp. stock and the market are 18% and 11%, respectively. In addition, the correlation coefficient between the stock and the market portfolio is 0.86. Calculate and then comment on the beta of the stock. (4 marks) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Non Financial Managers

Authors: Gene Siciliano

1st Edition

0071413774, 978-0071413770