Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please show the detail steps for a) b) c) d) , thanks ! Assume log returns are normally and independently distributed with mean 0 and

please show the detail steps for a) b) c) d) , thanks !

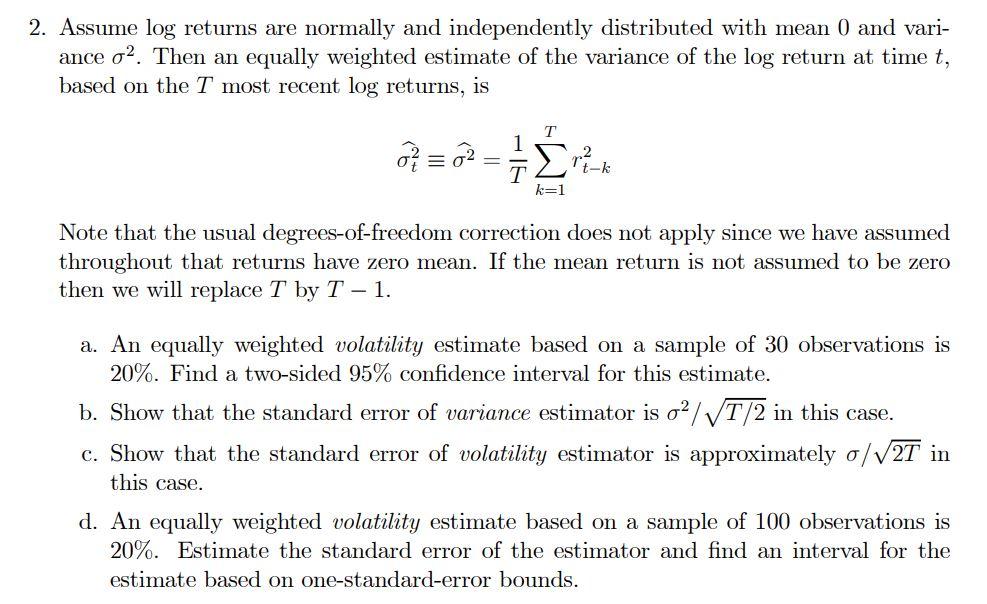

Assume log returns are normally and independently distributed with mean 0 and variance 2. Then an equally weighted estimate of the variance of the log return at time t, based on the T most recent log returns, is t22=T1k=1Trtk2 Note that the usual degrees-of-freedom correction does not apply since we have assumed throughout that returns have zero mean. If the mean return is not assumed to be zero then we will replace T by T1. a. An equally weighted volatility estimate based on a sample of 30 observations is 20%. Find a two-sided 95% confidence interval for this estimate. b. Show that the standard error of variance estimator is 2/T/2 in this case. c. Show that the standard error of volatility estimator is approximately /2T in this case. d. An equally weighted volatility estimate based on a sample of 100 observations is 20%. Estimate the standard error of the estimator and find an interval for the estimate based on one-standard-error bounds. Assume log returns are normally and independently distributed with mean 0 and variance 2. Then an equally weighted estimate of the variance of the log return at time t, based on the T most recent log returns, is t22=T1k=1Trtk2 Note that the usual degrees-of-freedom correction does not apply since we have assumed throughout that returns have zero mean. If the mean return is not assumed to be zero then we will replace T by T1. a. An equally weighted volatility estimate based on a sample of 30 observations is 20%. Find a two-sided 95% confidence interval for this estimate. b. Show that the standard error of variance estimator is 2/T/2 in this case. c. Show that the standard error of volatility estimator is approximately /2T in this case. d. An equally weighted volatility estimate based on a sample of 100 observations is 20%. Estimate the standard error of the estimator and find an interval for the estimate based on one-standard-error boundsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Routledge Handbook Of Responsible Investment

Authors: Tessa Hebb, James Hawley, Andreas Hoepner, Agnes Neher, David Wood

1st Edition

0415624517, 978-0415624510