Answered step by step

Verified Expert Solution

Question

1 Approved Answer

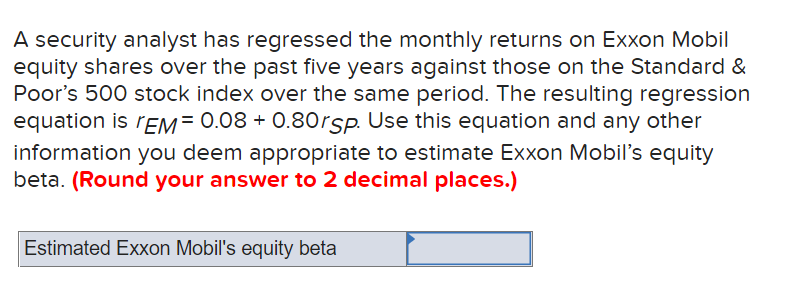

please show work :) A security analyst has regressed the monthly returns on Exxon Mobil equity shares over the past five years against those on

please show work :)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Laymans Guide To Managing Your Investments

Authors: Thomas Dunleavy

1st Edition

979-8763592214