Please show work and explain how you got each number from.

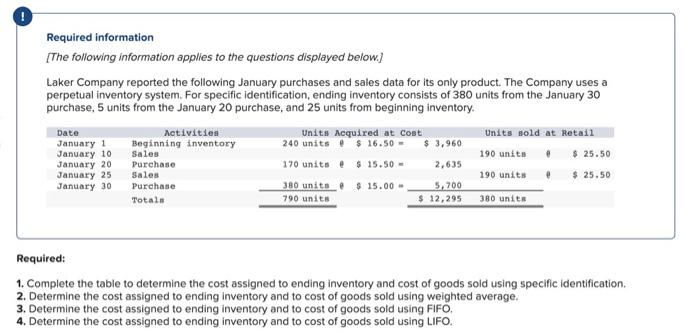

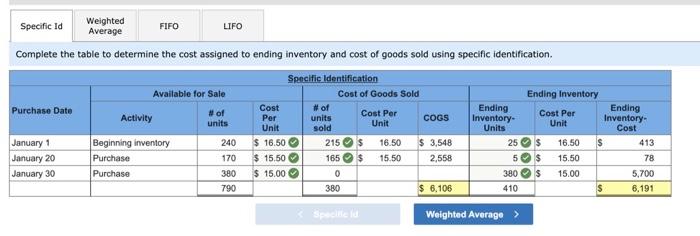

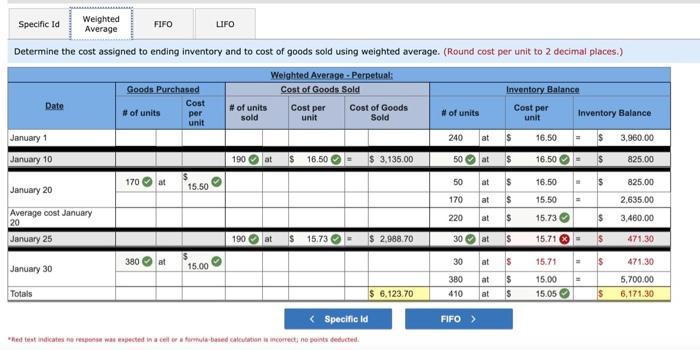

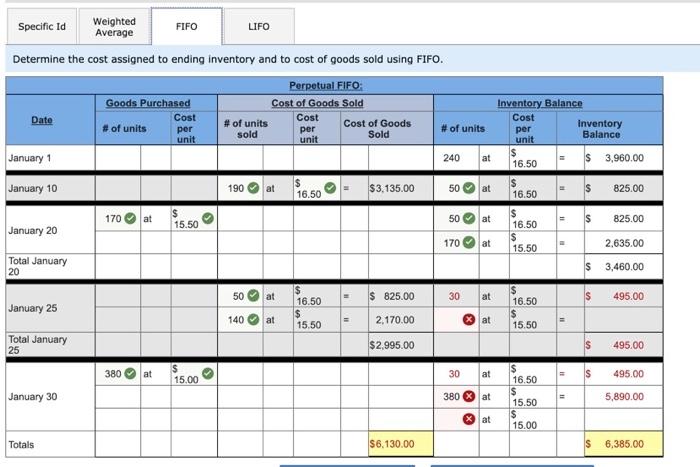

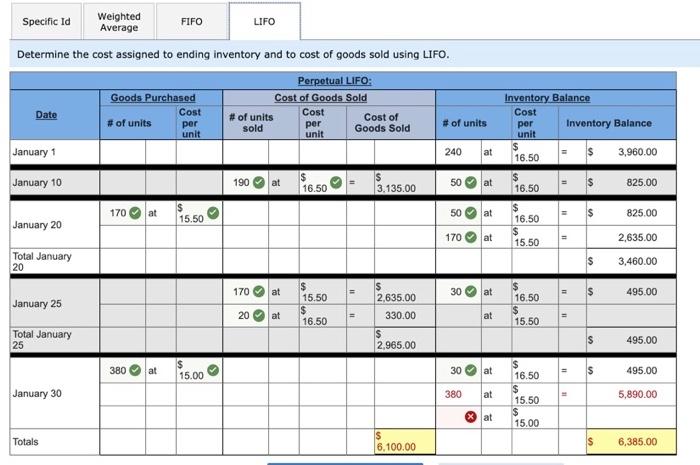

Required information [The following information applies to the questions displayed below.) Laker Company reported the following January purchases and sales data for its only product. The Company uses a perpetual inventory system. For specific identification, ending inventory consists of 380 units from the January 30 purchase, 5 units from the January 20 purchase, and 25 units from beginning inventory. Date Activities Units Acquired at Cost Units sold at Retail January 1 Beginning inventory 240 units $ 16.50 $ 3,960 January 10 Sales 190 units $ 25.50 January 20 Purchase 170 units $15.50 - 2,635 January 25 Sales 190 units e $ 25.50 January 30 Purchase 380 units $15.00 - 5,700 Total. 790 units $ 12,295 380 units Required: 1. Complete the table to determine the cost assigned to ending inventory and cost of goods sold using specific identification 2. Determine the cost assigned to ending inventory and to cost of goods sold using weighted average. 3. Determine the cost assigned to ending inventory and to cost of goods sold using FIFO. 4. Determine the cost assigned to ending inventory and to cost of goods sold using LIFO. Weighted Specific Id FIFO LIFO Average Complete the table to determine the cost assigned to ending inventory and cost of goods sold using specific identification Specific Identification Available for Sale Cost of Goods Sold Ending Inventory Purchase Date # of Cost # of Ending Cost Per Activity Per Ending units Cost Per COGS Unit units Inventory Unit Inventory Unit sold Units Cost January 1 Beginning inventory 240 $ 16.50 215$ 16.50 $ 3,548 25$ 16.50 $ 413 January 20 Purchase 170 $ 15.50 165$ 15.50 2,558 5$ 15.50 78 January 30 Purchase 380 $ 15.00 0 380$ 15.00 5,700 790 380 $ 6,106 410 $ 6.191 Speeltels Weighted Average > Specific la Weighted Average FIFO LIFO Determine the cost assigned to ending inventory and to cost of goods sold using weighted average. (Round cost per unit to 2 decimal places.) Weighted Average - Perpetual Goods Purchased Cost of Goods Sold Inventory Balance Date Cost # of units Cost per # of units Cost of Goods per Cost per sold unit # of units unit Sold Inventory Balance unit January 1 240 16.50 - $ 3,960.00 January 10 190 at S 10.50 S 3.135.00 50 at $ 16.50 825.00 170 50 ats 15.50 January 20 16.50 825.00 170 15.50 2,635.00 Average cost January 20 220 ats 15.73 $ 3,480.00 January 25 190 15.73 $ 2,988.70 30 at $ 15.713 380 at 15.00 15.71 471.30 January 30 380 at 5 15.00 5,700.00 Totals $ 6,123.70 410 ats 15.05 $ 6,171.30 Het les indicate newed in a celor mai calculation is incorrectne points deducted = at 471.30 = LIFO Specific Id Weighted FIFO Average Determine the cost assigned to ending inventory and to cost of goods sold using FIFO. Perpetual FIFO: Goods Purchased Cost of Goods Sold Date Cost Cost # of units # of units per per Cost of Goods # of units sold Sold unit January 1 Inventory Balance Cost per Inventory Balance 16.50 = $ 3,960.00 unit unit 240 at January 10 190 at $ 16.50 $3,135.00 50 at $ 825.00 170 at 50 at $ 16.50 $ 16.50 $ 15.50 15.50 = 825.00 January 20 170 at 2.635.00 Total January 20 $ 3,460.00 $ 825.00 $ 495.00 January 25 50 at 140 is 16.50 $ 15.50 30 at at 16.50 $ 15.50 > at 2,170.00 Total January 25 $ 2,995.00 S 495.00 380 at $ 15.00 11 495.00 30 at 380 at January 30 $ 16.50 $ 15.50 $ 15.00 = 5,890.00 %% at Totals $6.130.00 $ 6,385.00 Inventory Balance Cost per Inventory Balance unit $ 16.50 3,960.00 $ 825.00 16.50 Specific Id Weighted FIFO LIFO Average Determine the cost assigned to ending inventory and to cost of goods sold using LIFO. Perpetual LIFO: Goods Purchased Cost of Goods Sold Date Cost Cost # of units # of units Cost of per per #of units sold unit unit Goods Sold January 1 240 at 190 $ January 10 at 16.50 50 at 3.135.00 170 at 50 at 15.50 January 20 170 Total January 20 170 at 30 at 15.50 2,635.00 January 25 20 $ at 330.00 at 16.50 Total January $ 25 2,965.00 380 at 30 15.00 at January 30 380 at > $ $ 825.00 at 16.50 $ 15.50 2,635.00 $ 3.460.00 11 495.00 16.50 $ 15.50 = = $ 495.00 . s 495.00 $ 16.50 $ 15.50 $ 15.00 5,890.00 * at Totals IS 6,100.00 6,385.00